Introduction: Framing the Long-Term Consequences of Impatience

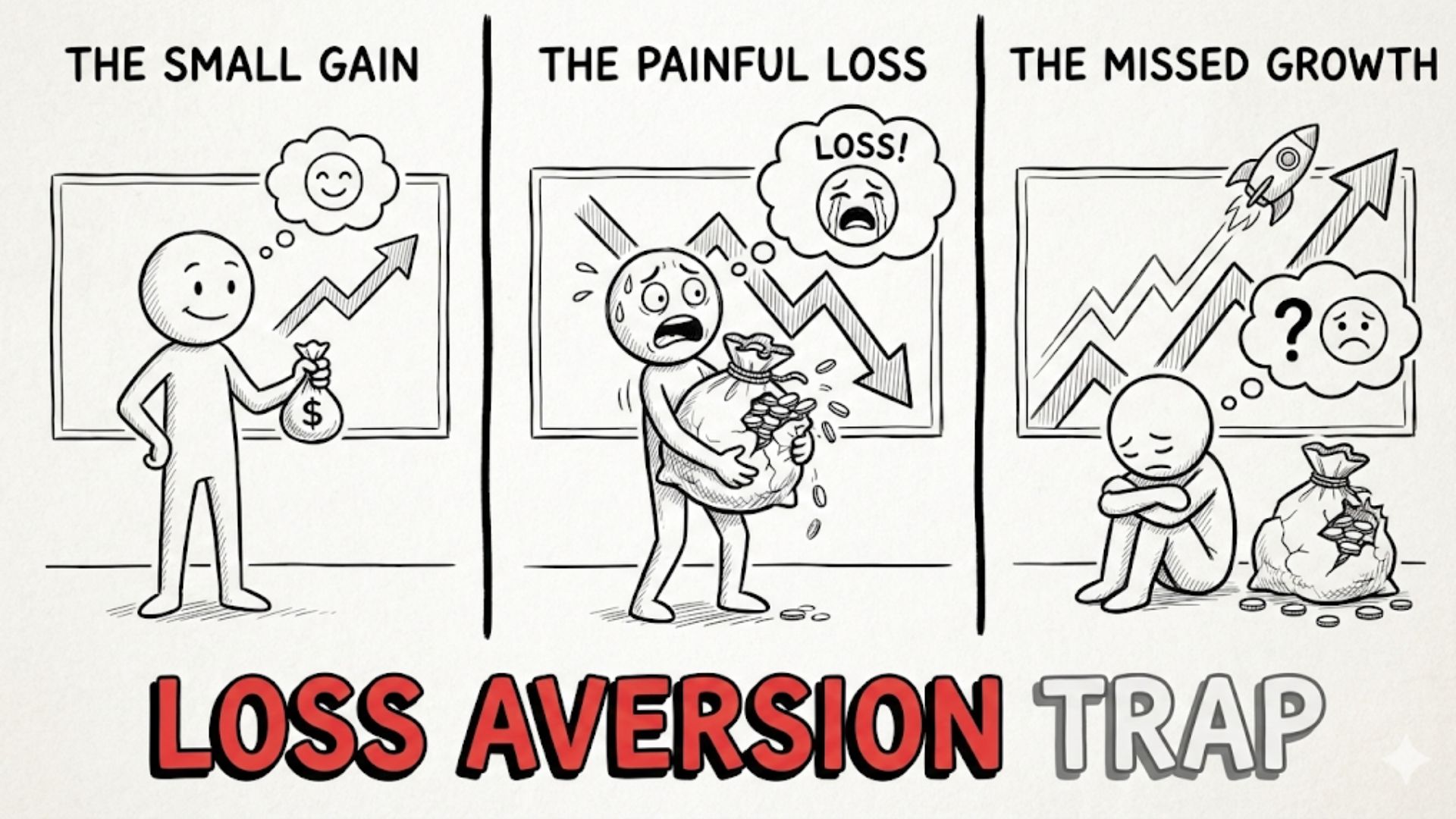

Loss aversion is among the most robust findings in behavioral economics. Individuals tend to experience the psychological pain of losses more intensely than the pleasure of equivalent gains. In isolation, this asymmetry appears adaptive: organisms that respond strongly to threats often survive longer. Yet in modern financial systems—where volatility is routine and temporary losses are structurally embedded in long-term growth—this bias can systematically distort portfolio decisions.

The deeper issue is not merely emotional discomfort in the face of declining asset values. It is the interaction between loss aversion and impatience. When short-term fluctuations are interpreted as urgent threats rather than expected features of compounding systems, investors compress their time horizons. Decisions are then evaluated against immediate outcomes rather than multi-decade trajectories. This time horizon misalignment transforms ordinary volatility into perceived failure.

Financial success, particularly in diversified capital markets, is a delayed payoff phenomenon. Returns accumulate gradually, often irregularly, and are heavily influenced by compounding. Impatience—amplified by loss aversion—disrupts participation in these systems. The long-term consequences are not the result of a single mistake but of repeated, structurally predictable reactions to short-term discomfort.

Understanding how loss aversion interacts with impatience requires moving beyond surface-level advice about “staying calm.” The relevant question is not why individuals feel discomfort in downturns, but why this discomfort persists across generations despite evidence that short-term volatility is normal and why institutions and cultural norms reinforce time horizon compression rather than counteract it.

The Core Problem: Time Horizon Misalignment

At the center of loss-driven portfolio errors lies a structural decision-making mismatch: evaluating long-duration assets using short-duration metrics.

Most financial assets—equities in particular—are claims on future streams of cash flows. Their expected value unfolds over years or decades. However, they are priced continuously and publicly. This creates a cognitive conflict. Investors can observe price changes in real time, but the underlying economic process that justifies holding the asset operates slowly.

Loss aversion intensifies this conflict. When prices decline, even temporarily, the brain encodes the event as a loss relative to a recent reference point. If the investor’s evaluation window is daily or quarterly, a drawdown becomes a salient negative outcome. If the evaluation window is multi-decade, the same drawdown may be statistically unremarkable.

The problem, therefore, is not volatility itself but the misalignment between the time horizon of the asset and the time horizon of evaluation. Short-term price movement becomes the dominant signal, crowding out long-term value creation. This misalignment leads to behaviors such as premature selling, excessive portfolio turnover, and avoidance of assets with higher long-term expected returns due to short-term variance.

Time horizon mismatch also influences risk perception. Risk is often defined as the probability of permanent capital impairment. However, when evaluation windows shrink, temporary volatility is treated as equivalent to permanent loss. Loss aversion converts variability into perceived danger, and impatience prevents the system from reverting to its long-term mean.

In this sense, the structural error is not emotional weakness but analytical compression. The decision-maker is applying a short-term feedback system to a long-term compounding mechanism.

Read also: Why “Positive Thinking” Is Making You Miserable

Why the Problem Persists Despite Experience

One might assume that repeated exposure to market cycles would attenuate loss aversion’s influence. Historical evidence demonstrates that downturns are recurrent and recoveries common. Yet impatience persists across generations of investors. The persistence of this bias reflects structural reinforcement mechanisms rather than mere ignorance.

Delayed and Noisy Feedback

Financial markets provide rapid price feedback but delayed fundamental feedback. Daily price movements are highly visible; the slow accumulation of earnings growth, innovation, and productivity is less perceptible. This asymmetry distorts learning.

Behavioral adaptation depends on clear cause-and-effect relationships. In investing, the link between disciplined long-term holding and eventual wealth accumulation is probabilistic and delayed. Meanwhile, the emotional feedback from losses is immediate and vivid. The human cognitive system is more responsive to rapid, emotionally salient signals than to abstract, long-term statistical advantages.

As a result, investors may incorrectly attribute short-term losses to flawed strategy rather than normal variance. This misattribution reinforces reactive behavior.

Incentive Structures

Institutional design frequently rewards short-term performance. Portfolio managers are often evaluated quarterly. Corporate executives may face compensation structures tied to annual earnings metrics. Financial media emphasizes daily market movements.

When incentives are aligned with short-term results, agents rationally respond by reducing short-term volatility, even if doing so lowers long-term expected returns. This dynamic filters into individual behavior. Retail investors observe and internalize a culture of constant performance measurement.

Incentive structures thus institutionalize impatience. Loss aversion becomes more potent when professional survival appears contingent on avoiding short-term drawdowns.

Cultural Conditioning and Immediacy Norms

Modern economic environments reward immediacy in many domains: rapid consumption, instant communication, real-time metrics. Digital platforms compress feedback loops and elevate short-term indicators. Financial markets are embedded in this broader cultural context.

When individuals are habituated to immediate responsiveness, the psychological tolerance for delayed payoff systems diminishes. Long-term investing, by contrast, demands extended periods without visible reinforcement. Loss aversion interacts with cultural impatience to produce exaggerated responses to temporary declines.

Present Bias and Cognitive Shortcuts

Present bias—the tendency to overweight immediate outcomes relative to future ones—compounds loss aversion. A loss today is weighted more heavily than a gain in ten years. Even when intellectually aware of compounding, individuals discount distant outcomes.

Moreover, cognitive shortcuts such as availability bias amplify recent negative events. A recent market decline becomes more salient than decades of growth data. This selective attention reinforces reactive behavior.

The persistence of loss-driven impatience, therefore, is not paradoxical. It is structurally supported by feedback asymmetry, incentive misalignment, cultural norms, and cognitive architecture.

Read also: Howard Marks & The Art of Second-Level Thinking

Real-World Consequences Across Domains

Although loss aversion is often discussed in the context of investing, its interaction with impatience extends across financial and professional domains.

Investing and Portfolio Turnover

In portfolios, loss aversion frequently manifests as premature selling of declining assets to “stop the pain,” even when long-term fundamentals remain intact. This behavior crystallizes temporary volatility into permanent loss. Conversely, investors may hold declining assets excessively to avoid realizing losses, distorting allocation decisions.

Frequent trading in response to short-term price changes introduces transaction costs, tax inefficiencies, and behavioral timing errors. Compounding, which depends on sustained participation, is interrupted.

Career Development

In career contexts, time horizon misalignment appears when individuals abandon skill development paths prematurely because early feedback is ambiguous or negative. Complex skill acquisition follows delayed payoff curves. Initial progress is slow, and competence compounds over years.

Loss aversion may cause individuals to interpret early setbacks as signals of permanent inadequacy. Impatience then leads to frequent directional changes, preventing cumulative expertise.

Entrepreneurship and Business Strategy

Entrepreneurial ventures often require extended periods of investment before profitability. Short-term revenue fluctuations may obscure long-term strategic positioning. When decision-makers overweight immediate losses relative to future optionality, they may underinvest in innovation or abandon promising projects prematurely.

Corporate strategy also suffers from quarterly earnings pressure. Long-term research and development expenditures may be reduced to stabilize short-term results, sacrificing future growth.

Savings Behavior and Consumption

Loss aversion can influence savings decisions when individuals perceive reduced current consumption as an immediate loss. The long-term gain of financial security is abstract and distant. Present bias magnifies the discomfort of deferred gratification.

Thus, impatience, reinforced by loss aversion, reduces participation in long-term capital accumulation systems across multiple domains.

Skill Accumulation and Intellectual Capital

Learning, reputation building, and network effects all exhibit compounding characteristics. Early effort often yields limited visible reward. Individuals sensitive to short-term setbacks may disengage before compounding effects materialize.

The structural theme across these domains is consistent: when evaluation windows are shorter than payoff horizons, temporary discomfort drives suboptimal exit decisions.

Read also: The Blueprint for Permissionless Wealth and Perpetual Peace

A Core Mental Model: Compounding and Delayed Feedback Systems

A central mental model for understanding loss aversion in portfolio decisions is the compounding and delayed feedback system.

Compounding systems exhibit three characteristics:

- Small incremental gains accumulate nonlinearly over time.

- Early stages appear slow and unimpressive.

- Interruptions disproportionately reduce long-term outcomes.

Equity markets historically demonstrate these properties. Returns are uneven, with periods of decline interspersed with growth. However, over extended horizons, the cumulative effect of retained earnings, reinvestment, and productivity growth produces exponential trajectories.

Delayed feedback systems obscure this trajectory. In early periods, progress may appear negligible relative to volatility. Only over extended durations does the curve become visibly upward-sloping.

Loss aversion disrupts compounding by truncating participation. Exiting during downturns interrupts the nonlinear accumulation process. Because exponential systems are sensitive to time in the system, not merely rate of return, shortened participation significantly reduces eventual outcomes.

This model clarifies why impatience is structurally costly. The cost is not merely missed gains in a particular year but forfeited exposure to the convexity of long-term growth.

Applying Better Thinking in Practice (Principles, Not Tactics)

Improving long-term reasoning requires structural alignment rather than emotional suppression. Several analytical principles are relevant.

First, evaluation windows should correspond to the underlying duration of the asset or project. Long-duration assets require long-duration assessment frameworks. This reduces the salience of short-term variance.

Second, incentives should reflect long-term performance where feasible. When decision-makers are rewarded for sustained outcomes rather than quarterly fluctuations, behavior shifts accordingly.

Third, probabilistic thinking should replace deterministic interpretations of short-term outcomes. Variance is not synonymous with error. Recognizing the statistical properties of complex systems reduces overreaction.

Fourth, separating signal from noise requires distinguishing between fundamental deterioration and temporary price movement. This analytical separation is conceptual rather than tactical; it reframes interpretation rather than prescribing specific trades.

These principles do not eliminate loss aversion. They reposition it within a broader analytical structure that reduces its dominance over decision-making.

Read also: Why Most Investors Underperform the Market

Common Misunderstandings About Patience

Patience is often misconstrued as passive endurance. In financial contexts, this misunderstanding obscures the distinction between disciplined long-term participation and indiscriminate inaction.

Long-term thinking does not imply ignoring information or tolerating deteriorating fundamentals. It implies aligning evaluation with relevant time scales. Reactivity to every fluctuation is distinct from responsiveness to substantive change.

Another misconception is that long-term orientation guarantees positive outcomes. Extended time horizons increase the probability of benefiting from compounding in diversified systems, but they do not eliminate uncertainty. Structural advantages improve odds; they do not create certainty.

A further misunderstanding is that emotional detachment is sufficient. Structural alignment of incentives, evaluation metrics, and feedback systems is more influential than individual temperament alone.

Clarifying these misconceptions prevents oversimplification of patience as a personality trait rather than a systemic alignment.

Connections to Broader Thinking Frameworks

The interaction between loss aversion and impatience intersects with several broader conceptual frameworks.

Second-Order Effects

Short-term loss avoidance may produce long-term opportunity costs. Selling during downturns reduces future exposure to recovery phases. The second-order effect of short-term relief is diminished long-term growth.

Incentive Design

Behavior responds to incentives. When institutions reward short-term stability, participants rationally avoid volatility. Designing evaluation systems around longer horizons shifts aggregate behavior.

Opportunity Cost Over Time

Time spent out of compounding systems carries opportunity cost. The forgone exponential growth from missed participation can exceed the magnitude of avoided short-term losses.

Path Dependency

Financial trajectories are path dependent. Early decisions influence subsequent options. Interruptions to compounding alter the entire future path of wealth accumulation.

These frameworks situate loss aversion within a larger architecture of decision theory and system dynamics.

Conclusion: Reframing Financial Success as a Time-Based System

Loss aversion is not merely an emotional bias; it is a structural force that interacts with impatience and institutional design to shape portfolio outcomes. When short-term evaluation dominates long-term objectives, compounding systems are disrupted. The resulting cost is cumulative rather than immediate.

The persistence of this problem across generations reflects feedback distortions, incentive structures, cultural norms, and cognitive architecture that collectively compress time horizons. Financial success, by contrast, operates as a time-based system. It depends less on momentary precision and more on sustained participation in delayed payoff mechanisms.

Reframing investing through the lens of time horizon alignment clarifies why impatience systematically undermines long-term wealth accumulation. The core issue is not volatility itself, but the decision-making framework applied to it. Aligning evaluation with duration transforms temporary losses from existential threats into statistically ordinary features of complex systems.

In this sense, the cost of loss aversion is not simply the discomfort of decline. It is the forfeiture of time within compounding structures—an invisible yet consequential erosion of long-term financial capacity.