Financial markets are theoretically designed to facilitate the efficient allocation of capital toward productive enterprises, rewarding participants who provide liquidity and assume risk. However, empirical data consistently demonstrates a significant “behavioral gap” between market returns and the actual returns realized by the average participant. This discrepancy is not primarily the result of intellectual deficiency or lack of information; rather, it is a structural failure of decision-making rooted in impatience and the misalignment of time horizons.

This article examines why the human cognitive apparatus is poorly calibrated for the non-linear nature of compounding. It explores the causal mechanisms that drive participants toward short-termism, the institutional and cultural forces that reinforce these biases, and the systemic consequences of prioritizing immediate utility over long-term strategic positioning.

1. Introduction: Framing the Long-Term Consequences of Impatience

The fundamental tension in capital accumulation is the conflict between the immediate gratification of consumption (or the relief of exiting a volatile position) and the delayed, exponential rewards of compounding. In a survival context, the human brain was evolutionarily optimized to prioritize the “now”—securing resources in a scarce environment where the future was highly uncertain. In the modern financial landscape, this biological inheritance manifests as a catastrophic inability to wait.

The stakes are not merely a few percentage points of annual return. Because wealth creation is a geometric process, small differences in the duration of an investment lead to vast disparities in terminal outcomes. An individual who interrupts compounding prematurely does not just lose interest; they lose the vertical portion of the growth curve. This systematic impatience leads to a transfer of wealth from those with short-term orientations to those with the structural capacity for long-term endurance.

Read also: How to Cure Excusitis and Unlock Your True Potential

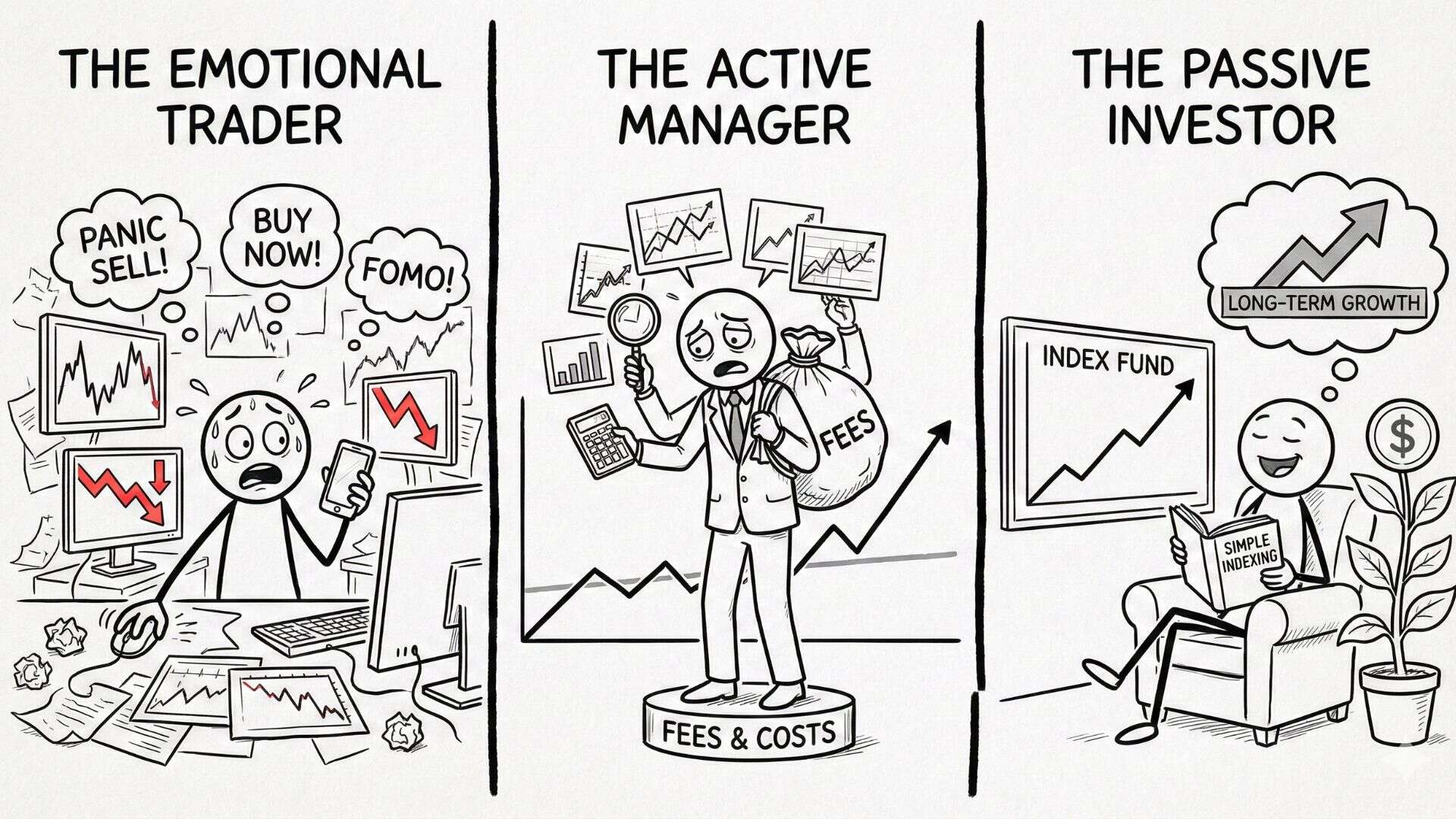

2. The Core Problem: Time Horizon Misalignment

The core of investor underperformance lies in a structural mismatch between the duration of the asset and the frequency of its evaluation. Most productive assets—be they equities, businesses, or specialized skills—require years or decades to realize their full economic potential. However, the modern decision-maker often evaluates these assets on a daily, monthly, or quarterly basis.

The Variance-Duration Disconnect

On short time horizons, asset prices are dominated by variance (noise). The probability of an asset price being higher or lower on a daily basis is nearly 50/50, regardless of its underlying quality. As the time horizon extends, however, the fundamental growth rate (signal) begins to dominate the variance.

The misalignment occurs when a decision-maker applies a high-frequency evaluation window to a low-frequency growth process. By observing an asset too frequently, the participant is exposed to an overwhelming amount of noise, which triggers emotional responses and reactive decision-making. This leads to “forced” exits during periods of temporary volatility, effectively liquidating long-term potential for short-term psychological relief.

The Agency Problem of the Future Self

In intertemporal choice theory, the “future self” is often treated by the brain as a stranger. Prioritizing capital for a version of oneself thirty years in the future feels like an act of altruism rather than self-interest. Consequently, when the present self experiences the pain of a market drawdown, the urge to terminate the investment is powerful. This failure to maintain a cohesive identity across time prevents the commitment required to see a compounding cycle through to its conclusion.

3. Why the Problem Persists Despite Experience

Despite the well-documented mathematical advantages of patience, the behavioral gap persists. This persistence is maintained by a complex web of feedback loops and institutional incentives.

Feedback Loop Distortion and Signal-to-Noise Problems

One reason experience fails to correct impatience is that the financial environment provides “noisy” feedback. In many domains, such as athletics or basic engineering, the feedback between action and result is clear and rapid. In the markets, however, a bad decision (e.g., speculative gambling) can be rewarded by luck in the short term, while a good decision (e.g., patient allocation) may be punished by temporary market downturns.

This distortion prevents the development of accurate mental models. Participants mistake luck for skill and volatility for permanent capital impairment. Because the “knee” of the compounding curve—the point where growth accelerates vertically—is often separated from the initial investment by decades, the positive reinforcement for patience is too delayed to effectively condition behavior.

Incentive Structures and the “Institutional Imperative”

Institutional structures are often the primary drivers of short-termism. Professional money managers are incentivized by quarterly performance metrics and annual bonuses. A manager whose strategy requires a five-year horizon to mature may be terminated after three quarters of underperformance.

This creates a “Principal-Agent” problem: the investor (the principal) may have a twenty-year horizon, but the manager (the agent) has a one-year horizon. The resulting behavior—excessive trading, “window dressing,” and herd behavior—is a rational response to the manager’s personal incentive structure, even if it is detrimental to the investor’s long-term returns.

Cultural and Technological Reinforcement

The current information environment is designed to maximize engagement through the amplification of urgency. Real-time notifications, 24-hour news cycles, and social media status-signaling create a “culture of the immediate.” In this environment, “doing nothing” is perceived as a failure of agency. Cultural conditioning suggests that intelligence is demonstrated through frequent action and reaction, when in the context of compounding, intelligence is often demonstrated through the refusal to act on noise.

Read also: Why Structural Consistency Outperforms Tactical Timing

4. Real-World Consequences Across Domains

While most visible in financial markets, the structural failure of impatience propagates through all areas of high-stakes decision-making.

- Investing: The average retail investor consistently underperforms index-level returns due to “market timing” errors and high turnover. Frequent transactions incur costs—taxes, commissions, and bid-ask spreads—that act as a drag on compounding. More critically, the participant exits the market during drawdowns, missing the few high-impact days of recovery that generate the majority of historical returns.+1

- Career Development: Human capital is subject to compounding similar to financial capital. Mastery of a complex field requires a prolonged “apprenticeship” phase. Impatience leads professionals to “job-hop” for marginal salary increases, frequently resetting their social capital and domain-specific expertise. They fail to reach the “seniority” phase where their expertise would yield non-linear rewards.

- Business Strategy: Organizations driven by impatient capital often suffer from “pivot-itis.” They abandon long-term R&D or brand-building efforts at the first sign of friction, seeking the immediate hit of a short-term revenue boost. This creates a state of perpetual fragility, where the organization never builds a structural “moat” or a sustainable competitive advantage.

- Skill Acquisition: The “plateau of latent potential” is the period where effort does not yet yield visible results. Impatient individuals abandon the pursuit during this plateau, failing to realize that the work they did was not “wasted” but rather “stored” for the future breakthrough.

5. A Core Mental Model: Compounding and Delayed Feedback Systems

The primary mental model for understanding this phenomenon is the Non-Linear Nature of Compounding.

Compounding is a geometric progression where the current output is a function of previous inputs and time. The mathematical formula for compounding—$FV = PV(1+r)^t$—reveals that the exponent ($t$, or time) is the most powerful variable in the equation.

The “Valley of Disappointment”

In a linear system, if you put in 10% more effort, you get 10% more result. In a compounding system, the relationship between time and output is asymmetric. During the early stages, the growth is almost imperceptible. This creates a “Valley of Disappointment,” where the actor feels that their effort or capital is yielding no return.

Impatience is essentially the failure to navigate this valley. Because the brain is optimized for linear feedback, it interprets the slow initial growth of a compounding system as a signal that the strategy is failing. By exiting the system before reaching the “knee of the curve,” the decision-maker ensures they never experience the phase where growth becomes effortless and vertical.

6. Applying Better Thinking in Practice (Principles, Not Tactics)

Reframing success as a time-based system requires a shift in decision-making principles. These are not “hacks,” but structural changes to how one processes information and evaluates outcomes.

Aligning the Evaluation Frequency with Asset Duration

To improve long-term reasoning, one must match the “sampling rate” of information to the “duration” of the goal. If an investment has a 10-year horizon, it should ideally be evaluated once a year, not once a day. This reduces the “availability heuristic” of recent price movements and allows the fundamental signal to emerge from the noise.

Designing for “Strategic Inertia”

Since willpower is a finite resource, a superior strategy involves building systems that make “doing nothing” the path of least resistance. This includes automation, pre-commitment contracts, and reducing the accessibility of real-time data. By creating friction for reactive decisions, the decision-maker protects the compounding process from their own biological impulses.

Focusing on Process Quality Over Outcome Variance

Because short-term outcomes are noisy, they are poor indicators of decision quality. Better thinkers focus on the integrity of the process. If a decision was made based on sound causal reasoning and a long time horizon, a temporary negative outcome is merely a statistical expectation, not a signal to pivot.

Read also: Why “Saving 10%” is a Financial Death Sentence

7. Common Misunderstandings About Patience

The concept of patience is frequently oversimplified in ways that lead to sub-optimal strategies. It is necessary to distinguish between strategic patience and intellectual lethargy.

Patience is Not Passivity

A common misunderstanding is that patience means “doing nothing” in the face of changing fundamentals. Strategic patience is an active state. it requires the continuous monitoring of the environment to ensure that the original thesis—the “why” behind the allocation—remains valid. It is the refusal to act on price while remaining vigilant about value.

The Fallacy of the “Forever” Horizon

Assuming that “longer is always better” is a misunderstanding of risk. A long time horizon allows for the recovery from volatility, but it does not protect against structural obsolescence. Being “patient” with a business model that is being fundamentally disrupted by technology is not a strategic advantage; it is a failure to recognize a sunk cost.

Patience is a Luxury of Liquidity

One cannot be patient if they do not have the financial or operational “buffer” to withstand short-term shocks. Impatience is often a forced condition caused by a lack of liquidity. True long-term thinking requires an “emergency fund” or a “margin of safety” that ensures the decision-maker is never forced to liquidate a compounding asset to meet immediate needs.

8. Connections to Broader Thinking Frameworks

The problem of investor underperformance is deeply intertwined with several other domains of decision theory:

- Second-Order Thinking: Impatience is typically a first-order response to pain (a market drop) or pleasure (a quick gain). Second-order thinking asks: “If I act now to stop the pain, what is the cost to my capital thirty years from now?”

- Incentive Design: Understanding how your environment (your boss, your social circle, your apps) is incentivizing you to be impatient is the first step toward building a “contrarian” time horizon.

- Opportunity Cost Reasoning: Every tactical “pivot” has an opportunity cost—not just in terms of transaction fees, but in terms of the “resetting” of the compounding clock.

- Signal vs. Noise: This framework, originating in information theory, is the ultimate diagnostic for time horizon misalignment. Short horizons are 90% noise; long horizons are 90% signal.

9. Conclusion: Reframing Financial Success as a Time-Based System

Most investors do not underperform because they are “wrong” about their assets; they underperform because they are impatient with the process. They treat wealth building as a task to be optimized through activity, rather than a system to be managed through duration.

Success in long-term capital allocation—whether in markets, careers, or business—is less about “beating” others and more about “not beating yourself.” It requires the intellectual humility to admit that your biology is wired for the short term and the structural foresight to build systems that protect you from that biology.

By reframing financial success as a function of time-weighted exposure to productive systems, the decision-maker gains an “arbitrage” advantage over the rest of the market. While the majority of participants compete in the crowded, high-noise environment of the short term, the vertical portion of the growth curve remains relatively uncrowded for those who can simply wait. The ultimate strategic advantage is not a faster reaction time, but a longer time horizon.