Introduction: Framing the Long-Term Consequences of Impatience

Personal finance is often presented as a technical domain governed by spreadsheets, tax rules, and asset selection. Yet beneath these surface details lies a more fundamental determinant of outcomes: time. Wealth accumulation, financial stability, and professional capital formation are not primarily the result of isolated decisions, but of sustained participation in systems that reward delayed payoff.

The central tension in personal finance is therefore temporal. Individuals make decisions in the short term, while most financial outcomes unfold over decades. This mismatch between immediate action and delayed consequence creates structural vulnerabilities. Impatience—defined not as emotional volatility but as compressed evaluation horizons—systematically distorts judgment.

Simplicity, in this context, is not aesthetic minimalism. It is structural alignment. Simple financial systems tend to win not because they are intellectually superior in isolation, but because they reduce friction, minimize error exposure, and support long-term participation in compounding environments. Complexity, by contrast, often amplifies feedback noise, increases behavioral error rates, and incentivizes short-term adjustments.

Understanding why simplicity tends to outperform complexity in personal finance requires examining the mechanisms that undermine long-term success. These mechanisms include time horizon misalignment, incentive distortions, delayed feedback structures, and cognitive biases such as present bias and short-termism. The issue is not that individuals lack information; it is that they operate within systems that reward immediacy and penalize patience.

The Core Problem: Time Horizon Misalignment

At the heart of financial underperformance lies a structural decision-making error: evaluating long-duration systems with short-duration metrics.

Most wealth-building processes are inherently long term. Investment returns compound gradually. Career capital accumulates through sustained skill development. Savings habits generate resilience over decades. Yet these systems are observed through short-term feedback loops: daily market prices, monthly income fluctuations, quarterly performance reviews.

When evaluation windows are shorter than payoff horizons, volatility becomes disproportionately salient. Temporary fluctuations are interpreted as signals requiring intervention. Complexity often emerges as a response to this perceived need for control. Investors diversify excessively across strategies, frequently adjust allocations, or adopt tactical overlays in an attempt to reduce short-term discomfort.

However, each adjustment introduces friction—transaction costs, tax consequences, cognitive load, and error risk. Over time, these frictions accumulate. The intended benefit of reducing short-term variability often results in diminished long-term returns.

Simplicity, in contrast, aligns the structure of decision-making with the duration of the underlying system. A straightforward allocation strategy or automated savings process reduces the frequency of intervention. By lowering the number of decision points, simplicity decreases the probability of behaviorally driven mistakes.

Time horizon misalignment thus explains why complex systems underperform in practice even when theoretically sound. The issue is not computational insufficiency but behavioral exposure.

Read also: How Loss Aversion Impacts Portfolio Decisions

Why the Problem Persists Despite Experience

If long-term simplicity is advantageous, why do individuals repeatedly gravitate toward complexity and short-term responsiveness? The persistence of impatience across generations reflects structural and institutional reinforcement mechanisms.

Delayed Feedback and Attribution Errors

Compounding systems provide delayed and probabilistic feedback. The relationship between disciplined behavior and eventual outcome is statistically reliable but temporally distant. In the interim, randomness dominates observable results.

Human cognition evolved to learn from rapid feedback loops. Immediate cause-and-effect relationships support adaptation. In finance, however, the most consequential benefits—such as decades of compounded returns—are invisible in early stages. Early gains appear modest; short-term fluctuations dominate perception.

Complex strategies often provide the illusion of control. Adjustments create a sense of responsiveness to new information, even when such information is largely noise. Because long-term outcomes are delayed, individuals may misattribute short-term underperformance to insufficient complexity rather than to normal variance.

Incentive Structures and Professional Influence

Institutional incentives frequently reward activity over restraint. Financial intermediaries often generate revenue through transactions, product innovation, and active management. Media environments prioritize novelty and short-term developments.

Professionals operating under quarterly evaluation systems rationally emphasize short-term metrics. This orientation influences public discourse. Individual investors internalize norms that equate engagement with competence and complexity with sophistication.

Simplicity, by contrast, is less visible. A strategy that requires minimal adjustment generates little narrative. As a result, cultural reinforcement favors action and optimization over endurance.

Cultural Norms of Immediacy

Contemporary economic systems amplify immediacy. Digital platforms provide instant metrics, real-time analytics, and continuous performance tracking. Consumption and communication occur at accelerating speeds. In such environments, delayed gratification is culturally atypical.

Financial decisions occur within this broader cultural framework. When individuals are accustomed to rapid responsiveness in most domains, long-duration financial systems feel counterintuitive. Complexity offers a way to simulate immediacy within inherently slow processes.

Present Bias and Short-Termism

Present bias—the tendency to overweight immediate costs and benefits—reinforces complexity. A simplified strategy may produce short-term discomfort during volatility. The perceived immediate loss outweighs the abstract long-term advantage of staying the course.

Short-termism also manifests in consumption decisions. The immediate pleasure of spending competes with the distant security of saving. Simple savings systems reduce discretionary friction, whereas complex budgeting structures increase cognitive load and decision fatigue.

The persistence of impatience, therefore, is not accidental. It is structurally supported by feedback asymmetry, institutional incentives, and cognitive architecture.

Read also: The Cost of Overconfidence in Investing

Real-World Consequences Across Domains

Time horizon misalignment and complexity-induced impatience extend beyond portfolio allocation. Their influence appears across financial and professional domains.

Investing

In investing, complexity often manifests as frequent portfolio adjustments, tactical timing strategies, and the pursuit of short-term alpha. Each modification introduces transaction costs and behavioral timing risk.

Simple strategies—characterized by broad diversification and infrequent adjustment—reduce decision frequency. Fewer decisions reduce exposure to behavioral biases. Because compounding rewards sustained participation, minimizing interruption becomes a structural advantage.

Career Development

Career capital accumulates through long-term skill acquisition and reputation formation. However, individuals often respond to short-term dissatisfaction by switching paths prematurely. Frequent transitions disrupt compounding expertise.

Simplicity in career planning does not imply rigidity. Rather, it reflects sustained commitment to foundational skills that yield increasing returns over time. Excessive optimization for immediate compensation or status can undermine long-term trajectory.

Entrepreneurship and Business Strategy

Businesses that prioritize quarterly metrics may underinvest in long-term research and development. Strategic simplicity—clear value propositions, focused execution, and consistent reinvestment—often outperforms frequent strategic pivots driven by short-term performance fluctuations.

Complex strategic overlays may obscure core economic drivers. Simplicity enhances clarity, enabling better alignment between incentives and long-term objectives.

Savings and Consumption

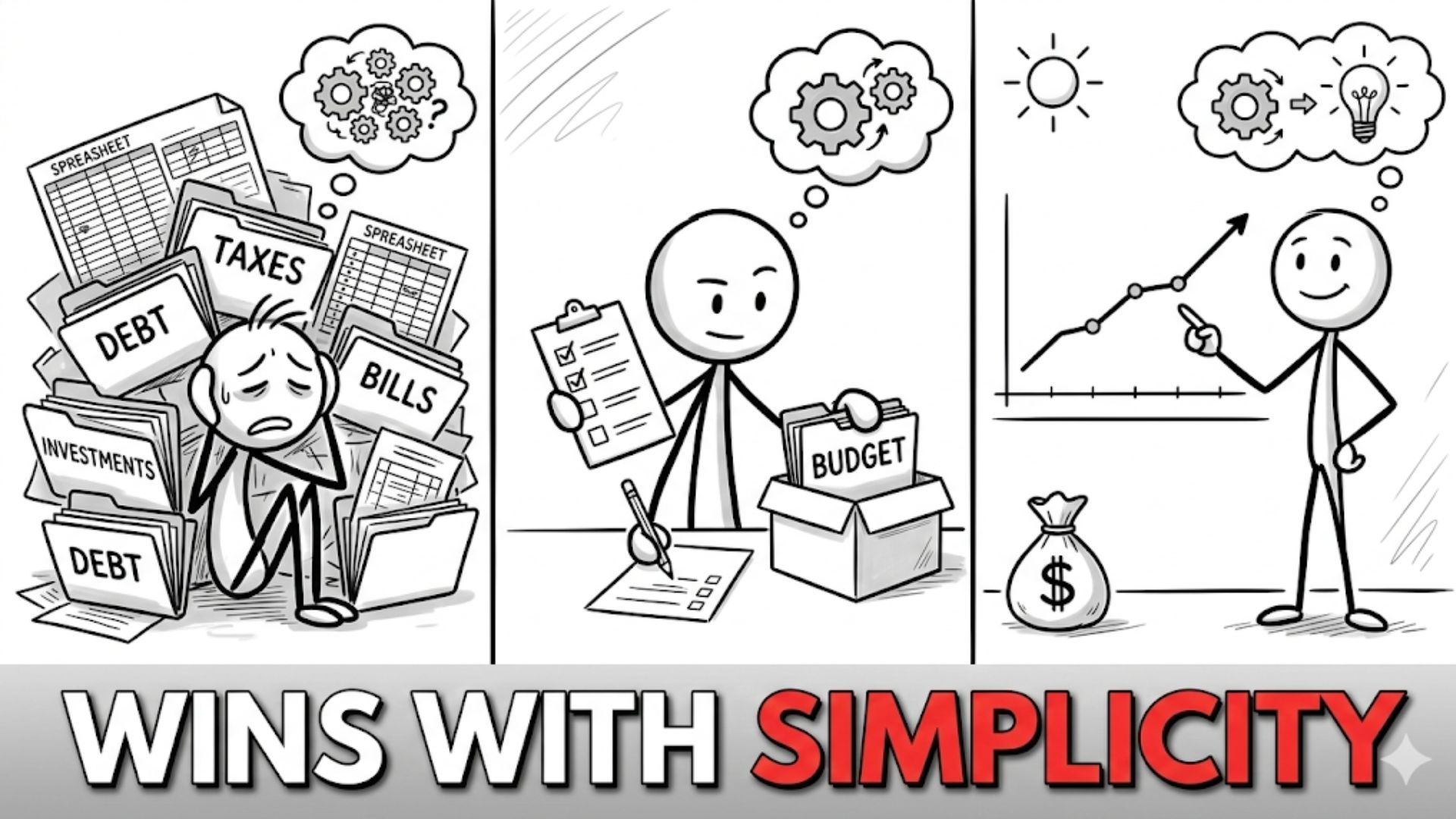

Household financial stability often depends less on intricate optimization and more on consistent surplus generation and disciplined reinvestment. Automated systems that reduce discretionary intervention tend to outperform elaborate budgeting schemes that require constant monitoring.

In each domain, simplicity reduces cognitive overhead and behavioral risk. Impatience, by contrast, multiplies decision points and amplifies error probability.

Read also: Why Long-Term Thinking Is a Financial Advantage

A Core Mental Model: Compounding and Delayed Feedback Systems

The conceptual foundation underlying simplicity’s advantage is the compounding and delayed feedback system.

Compounding systems possess nonlinear growth properties. Incremental gains accumulate multiplicatively rather than additively. However, early phases appear disproportionately modest. Only over extended periods does the exponential nature of growth become visible.

Delayed feedback systems obscure this progression. Because returns are uneven and volatility is persistent, short-term observation windows underrepresent long-term trajectory.

Simplicity supports compounding by minimizing interruption. Each deviation from a long-term process resets momentum. Transaction costs, tax liabilities, and behavioral timing errors truncate the exponential curve.

The mathematical sensitivity of exponential growth to time is critical. Small differences in duration produce large differences in outcome. Therefore, the primary advantage of simplicity lies in preserving time within the system.

Complexity increases the probability of exit—either partial or complete—during periods of discomfort. By contrast, simple systems reduce opportunities for reactive intervention.

This mental model clarifies why patience is structurally advantageous. It is not a moral virtue but a mechanical property of exponential processes.

Applying Better Thinking in Practice (Principles, Not Tactics)

Improved long-term reasoning arises from structural alignment rather than tactical optimization.

First, evaluation intervals should match the duration of the underlying system. Long-term investments should be assessed over correspondingly long horizons. Short-term metrics should be contextualized within broader trajectories.

Second, decision frequency should be minimized where possible. Each decision introduces potential error. Systems that automate or standardize core processes reduce behavioral exposure.

Third, complexity should be justified by durable informational advantage rather than by perceived need for control. If additional layers do not materially improve expected long-term outcomes, they likely increase friction.

Fourth, incentives should be examined critically. When performance measurement emphasizes short-term variance, structural pressure toward complexity and reactivity increases.

These principles focus on alignment rather than prescription. They recognize that long-term success depends less on precision and more on sustained participation.

Read also: Mastering The 5 AM Club for Elite Performance and Cognitive Sovereignty

Common Misunderstandings About Patience

Patience is frequently misunderstood as passivity or complacency. In reality, long-term alignment can coexist with active monitoring of fundamental change. The distinction lies between reacting to noise and responding to structural shifts.

Another misconception is that simplicity implies intellectual laziness. On the contrary, designing robust simple systems often requires deep understanding of underlying mechanics. Simplicity at the operational level can reflect complexity at the conceptual level.

It is also inaccurate to assume that long-term orientation guarantees success. Structural alignment improves probabilities but does not eliminate uncertainty. Compounding systems remain subject to systemic shocks and regime changes.

Finally, some interpret simplicity as universal uniformity. In practice, simplicity must be context-specific. The principle is not minimalism for its own sake, but coherence between system design and time horizon.

Connections to Broader Thinking Frameworks

The advantage of simplicity intersects with several broader analytical concepts.

Second-Order Effects

Complex interventions may produce unintended downstream consequences. Frequent trading intended to reduce risk can increase tax burden and behavioral error, reducing net return.

Incentive Design

When systems reward activity, participants act. Aligning incentives with long-term outcomes reduces pressure toward unnecessary complexity.

Opportunity Cost

Time spent managing intricate financial structures carries opportunity cost. Cognitive resources allocated to marginal optimization could be deployed toward higher-return activities such as skill development or business creation.

Path Dependency

Early decisions influence subsequent options. A pattern of frequent adjustments establishes habits of reactivity. Conversely, early commitment to simple systems reinforces long-term stability.

These frameworks situate simplicity within a larger architecture of decision theory and institutional analysis.

Read also: How Anchoring Bias Affects Financial Choices

Conclusion: Reframing Financial Success as a Time-Based System

Personal finance is not primarily a problem of information scarcity or computational deficiency. It is a problem of temporal alignment. Wealth accumulation, career capital, and strategic advantage are outcomes of prolonged engagement with compounding systems.

Impatience disrupts these systems by compressing evaluation windows and amplifying sensitivity to short-term variance. Complexity often emerges as a response to discomfort, yet increases friction and error exposure.

Simplicity wins not because it is inherently superior in all contexts, but because it preserves time within compounding processes. By reducing decision frequency, aligning incentives with duration, and minimizing behavioral interference, simple systems enhance the probability of long-term participation.

Financial success, viewed through this lens, is less about continuous optimization and more about structural coherence. When time horizons, incentives, and evaluation frameworks align, the mechanics of compounding operate with minimal disruption.

Reframing personal finance as a time-based system clarifies why impatience systematically undermines outcomes. The critical resource is not sophistication but sustained duration. Simplicity functions as a mechanism for protecting that duration against the structural pressures of immediacy.