[!IMPORTANT] THE SNAPSHOT

- Star Rating: 4.5/5

- One-Sentence Verdict: A visual guide that proves the biggest risk to your portfolio isn’t a market crash—it’s your reaction to it.

- Best For: Emotional investors, index fund fans, and people who watch financial news daily.

- Difficulty: Very Easy.

[Get “The Behavior Gap” on Amazon]

Closing your personal behavior gap begins with a single realization: you cannot control the market, but you can control the person staring back at you in the mirror.

INTRODUCTION: The Painful Truth About Performance

Traditional financial literacy operates on a flawed premise: it assumes that if we give people enough charts, data points, and spreadsheets, they will make rational decisions. It treats the human brain like a high-powered calculator when, in reality, our “biological hardware” is still running on ancestral software designed for survival on the savannah, not portfolio management in the 21st century. This software is powered by two primary engines: fear and greed.

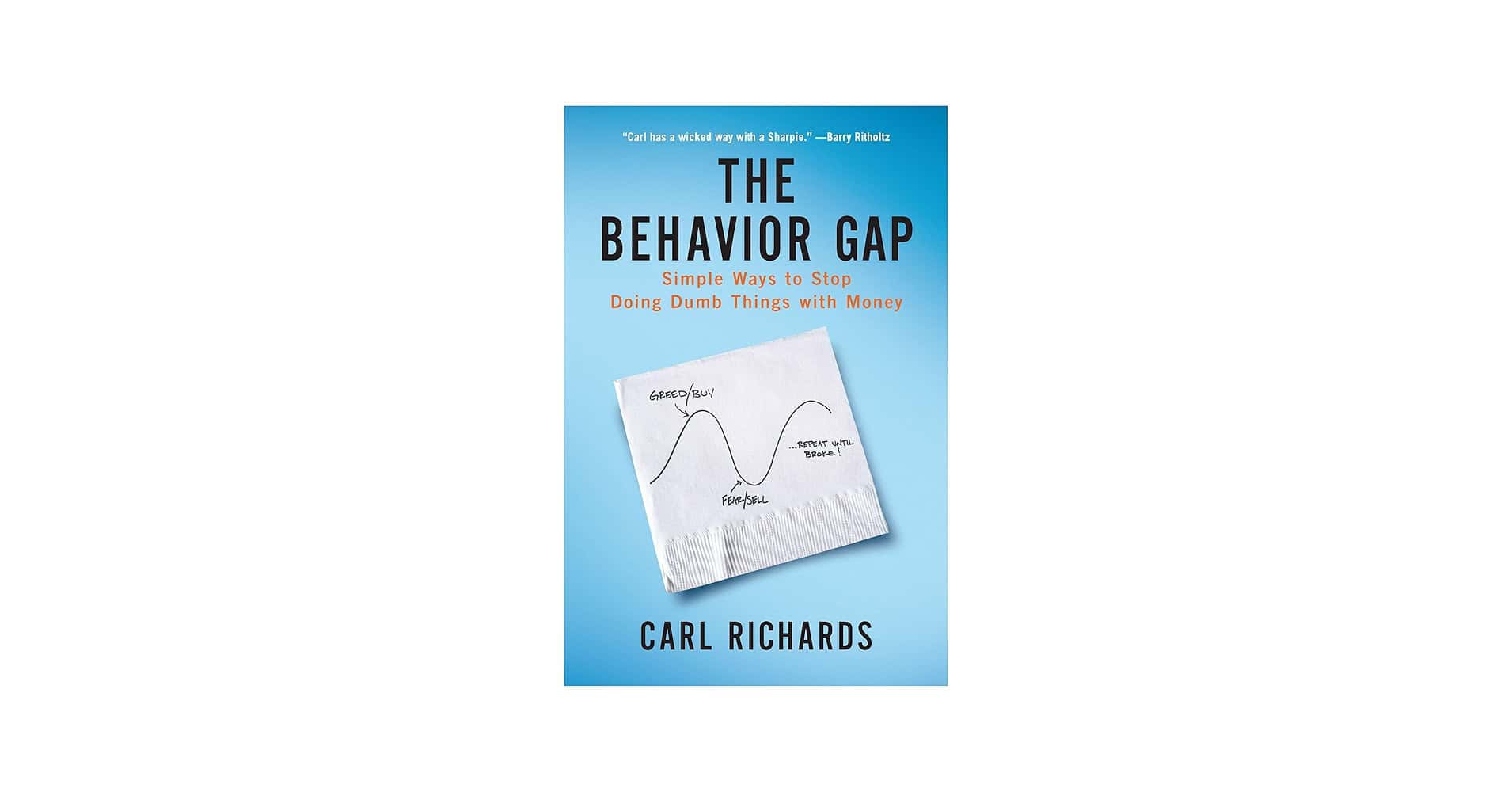

To visualize this, imagine one of Carl Richards’ most famous napkin sketches. It features a simple wave representing market cycles. At the peak of the wave, there is an arrow pointing to the word “Greed/Buy!” At the very bottom of the trough, there is another arrow pointing to “Fear/Sell!” Underneath the whole mess, Richards has scrawled the caption: “Repeat until broke.” This is the “Cycle of Shame,” and it is the default setting for the human mind.

The “painful truth” of the investment world is that the average investor consistently underperforms the very funds they invest in. This isn’t because the funds are inherently bad; it’s because the investors are human. We are biologically drawn to “Buy High and Sell Low.” We wait until an investment is proven and “safe”—which usually means it has already reached a peak—to buy. Conversely, we wait until the pain of loss is unbearable—usually at the exact moment the market is bottoming out—to sell.

Carl Richards, a Certified Financial Planner known as the “napkin philosopher,” recognized that the noise of Wall Street was drowning out common sense. Using nothing but a Sharpie and a stack of napkins, Richards began sketching simple metaphors to illustrate how we sabotage our own wealth. His mission is to help us stop “doing dumb things with money” by shifting our focus from “market returns”—over which we have zero authority—to “personal behavior,” where we have total responsibility.

WHAT IS THE “BEHAVIOR GAP”?

In the world of strategic finance, the most important metric isn’t the S&P 500’s annual percentage; it is the distance between mathematical potential and actual human results. This distance is what Richards famously defines as the Behavior Gap.

The Behavior Gap: The difference between the returns an investment produces and the actual returns an investor realizes, caused by emotional decision-making, poor timing, and the impulse to chase trends.

To understand why this matters, we must break down the three components derived from data points provided by rigorous studies from firms like Morningstar and Dalbar. These studies consistently show that while mutual funds might return 8% or 10%, the people inside those funds often walk away with significantly less.

- Investment Return: This is what the “Market” or a mutual fund generates. It is the raw mathematical performance of the assets if they were held without interference for the entire duration.

- Investor Return: This is what the individual actually puts in their pocket. It accounts for the friction of the human element: when the investor entered the market (usually too late), when they panicked and left (usually too early), and the unnecessary fees they paid in a desperate attempt to “fix” their portfolio.

- The Gap: This is the value lost to the “human element”—the combined weight of panic, overconfidence, and the hubris of trying to “time” the market.

Read also: The One Page Financial Plan Summary: STOP OVERTHINKING YOUR MONEY (CARL RICHARDS REVIEW)

“The So What?” Layer: The Emotional and Financial Cost

To illustrate the devastating impact of this gap, consider a professional with a $100,000 portfolio. Over a 20-year period, the “Market” (Investment Return) earns an average of 10% annually. Mathematically, that 100,000 should grow to approximately **672,750**.

However, because this investor reacts to news headlines and retreats to cash during market dips, their actual “Investor Return” is only 4%. After 20 years, that same 100,000 has only grown to approximately **219,112**.

The Behavior Gap in this scenario has cost the investor $453,638. But this isn’t just a number on a spreadsheet; it is an emotional and lifestyle catastrophe. A $672,000 nest egg represents a retirement defined by travel, legacy-building, and the freedom to say “yes” to experiences. A $219,000 nest egg represents a retirement of scarcity—one where you are counting pennies for medication, worrying about the heating bill, and perhaps being forced to work long past your physical prime. The Behavior Gap is the difference between a life of dignity and a life of desperation. Understanding the gap is the first step toward wealth; the second is identifying the “noise” that creates it.

KEY LESSON 1: IGNORE THE NOISE

We live in an age of information overload. The 24-hour financial news cycle is not designed to help you retire; it is a product designed to keep you watching so that advertisers can sell you products. This creates a strategic danger by constantly triggering the brain’s “fight or flight” response. Richards is famously blunt about the value of financial media:

“Information is cheap, meaning is expensive.”

The news cycle exploits our natural tendency to avoid pain and seek pleasure. When we see headlines about a global crisis, our instinct is to “do something” to protect ourselves. Richards uses the “Libya Oil” example from the source to illustrate market irrationality. In 2011, market commentators obsessed over how unrest in Libya would destroy the oil market. In reality, Libya’s oil exports were relatively small in the context of global consumption, yet the collective emotion of fear caused a massive market reaction. The market reacted to the headline and the feeling, not the underlying export data.

“The So What?” Layer: The Convenience Trap

Many investors fall victim to the “Economist Smirk”—the false sense of intellectual superiority that comes from reading high-level financial publications. This leads to the “Paradox of Information Overload,” where an investor feels like they have “insider” knowledge that necessitates immediate action.

In reality, the convenience of technology has become our greatest enemy. Because we can check our balances on our phones while waiting for coffee, we feel like we are “working” or “being productive” when we trade. We confuse activity with progress. Checking your portfolio daily is like checking the temperature of your oven every thirty seconds while trying to bake a cake; it doesn’t make the cake bake faster, it just lets the heat out and ruins the result. If you rely on news for investment signals, you are already too late. By the time a “crisis” or a “boom” is on CNBC, the market has already priced it in. Success comes from finding a “good” strategy and having the discipline to ignore the noise that tells you to abandon it.

KEY LESSON 2: PERFECT IS THE ENEMY OF GOOD

A major driver of the Behavior Gap is the obsessive search for the “world’s best investment.” Many investors spend their lives trying to optimize their portfolio to the last decimal point, only to abandon the entire plan the moment volatility hits. Richards argues that the “perfect” investment does not exist; the “right” investment is entirely dependent on your personal goals.

To illustrate the sheer randomness and complexity of the market, Richards shares “The Chocolate Anecdote.” He tells the story of a hedge fund manager who attempted to buy up the world’s entire chocolate supply. When you are sitting in your living room trying to pick the “perfect” stock, you have no idea that there is a billionaire in a skyscraper somewhere making a move that has nothing to do with fundamentals and everything to do with cornering a commodity. The market is “crazy” and unpredictable because the motives of its players are often hidden.

One of the most common mistakes in this quest for perfection is “Investment Collecting.” This occurs when an investor haphazardly buys “hot” funds or stocks they heard about at a party. In reality, they often end up with multiple similar funds, which increases complexity and risk without adding value. Richards contrasts this with a “Portfolio Tapestry”—an intentional, principle-driven strategy where every thread (investment) has a specific purpose and aligns with the others.

“The So What?” Layer: The Blinding Power of Overconfidence

The strategic danger of “picking winners” is that it relies on luck disguised as skill. Richards notes that Overconfidence is a leading cause of risk-taking. We believe we are smarter than the average, which blinds us to the fact that past performance is a terrible predictor of future success.

Research indicates that high fees are a much more reliable predictor of poor performance than past returns are of future success. The more you pay for “sophistication” and “active management,” the more you are often just paying to widen your Behavior Gap. If no perfect product exists, your strategic priority must shift from the “product” to the “process.” Investing based on past growth is the equivalent of guessing the next result of a coin toss based on previous flips; the history of the coin does not change the 50/50 physics of the next toss.

KEY LESSON 3: FINANCIAL PLANNING IS A PROCESS, NOT A PRODUCT

Most people view a financial plan as a thick binder that sits on a shelf—a static document meant to predict the next 30 years. Richards argues that this version of planning is worthless because it is based on unpredictable assumptions about inflation, market performance, and longevity. Surprises are the only constant in life. Instead, he insists that “planning” is a verb, not a noun.

He uses the Airplane Metaphor to clarify this: A pilot flying from New York to Los Angeles is actually off-course about 90% of the time. The plane is constantly buffeted by wind and turbulence. However, the pilot arrives safely because of continuous, tiny course corrections. Financial planning is the same. It is not about being “right” from the start; it is about having a process to get back on track when life inevitably changes.

Read also: The Automatic Millionaire Summary: How to Get Rich Without a Budget (The David Bach Method)

“The So What?” Layer: Personal Finance is Personal

Richards rejects “Generalized Advice”—the rules of thumb that people shout on social media. Whether it’s the universal rejection of annuities or the “4% rule,” Richards argues these are often useless because they ignore your specific reality. He cites Tim Maurer’s mantra:

“Personal finance is more personal than finance.”

The ultimate goal of money isn’t just to have a larger number in a bank account; it is to facilitate a meaningful life. Richards references studies indicating that money’s impact on happiness plateaus after an annual income of approximately $75,000. Beyond this point, the correlation between wealth and joy diminishes.

Strategically, this means that a “One-Page Financial Plan” that focuses on your deep-seated values—like spending time with family or contributing to your community—is far more effective than a 50-page binder of projections. If your money isn’t supporting your life goals, you are working for your money, rather than your money working for you.

CRITICAL ANALYSIS: IS IT TOO BASIC?

A common critique of The Behavior Gap is that its lessons are too simplistic for “advanced” traders. They argue that in a world of algorithmic trading and complex derivatives, telling someone to “just behave” is reductive.

However, Richards provides a powerful counter-argument: sophistication is often a trap. The most complex financial problems usually require the simplest behavioral solutions. The “Greater Fool Theory”—the idea that you can buy an overvalued stock because some “greater fool” will pay more for it later—is just a sophisticated-sounding way to describe gambling. We are biologically drawn to being the “fool” because our brains crave the excitement of the hunt.

“Simple. Not Easy.”

While the concepts are simple to understand, they are incredibly difficult to execute when your life savings are fluctuating. Furthermore, we must add intellectual weight by looking at the “Happiness” debate. While Richards caps the money/happiness correlation at $75k, other scholars like Dunn and Norton (Happy Money) suggest that financial gain can lead to significant happiness if spent correctly (buying experiences or “buying time”). This highlights that while Richards is right about behavior, the strategic use of wealth is as important as its accumulation.

PROS AND CONS

| PROS | CONS |

| Relatable “Napkin Sketches”: Visual metaphors make complex psychological concepts immediately clear. | Repetitive: The core message of “stay the course” is reiterated frequently throughout the book. |

| Focus on Controllables: Empowers the reader by ignoring market noise and focusing on fees and behavior. | Lack of Specific Picks: Investors looking for a “hot tip” or specific fund recommendations will be disappointed. |

| Non-Judgmental Tone: Richards acknowledges that we are all wired for “dumb” behavior, reducing investor shame. | Simplistic for Pros: Advanced traders may feel the book lacks technical depth or academic rigor. |

CONCLUSION: BEHAVING YOUR WAY TO WEALTH

The overarching goal of Richards’ philosophy is to transition the reader from trying to “beat the market” to “behaving for the market.” You are responsible for your behavior, even if you have no control over the results the market delivers.

Imagine a final napkin sketch:

- Draw two large, overlapping circles.

- Circle A is labeled: “Things that matter.”

- Circle B is labeled: “Things you can control.”

- The tiny area where they intersect is where your focus must live.

Most investors spend 90% of their energy on things that matter but they cannot control (interest rates, geopolitical unrest). By shifting your focus to the intersection, you effectively close the Behavior Gap. Wealth isn’t about being the smartest person in the room; it’s about being the most disciplined.

CALL TO ACTION: CLOSE THE GAP

To stop doing “dumb things with money” and start behaving your way to wealth, implement this 3-step action plan:

- Delete the Noise: Stop checking your portfolio daily. In fact, if you find yourself compulsively trading, delete the Robinhood app (or your broker’s app) from your phone. Force yourself to use a desktop computer so that the friction of logging in prevents impulsive “thumb-trading” at the dinner table.

- Acknowledge the Gap: Be brutally honest. Look at your personal returns over the last five years and compare them to a simple S&P 500 index fund. The difference is your personal Behavior Gap. Calculate the dollar amount and write it down.

- The “24-Hour” Checklist: Before making any trade, you must wait 24 hours and answer three questions:

- Is this trade based on a change in my long-term life goals?

- Am I reacting to a news headline or a “hot tip”?

- Have I consulted my “One-Page Financial Plan” to see if this aligns with my values?

Remember: your portfolio is like a bar of soap; the more you touch it, the smaller it gets due to the friction of fees, taxes, and bad timing. Put the soap down. Stay the course.