Introduction: Framing the Long-Term Consequences of Impatience

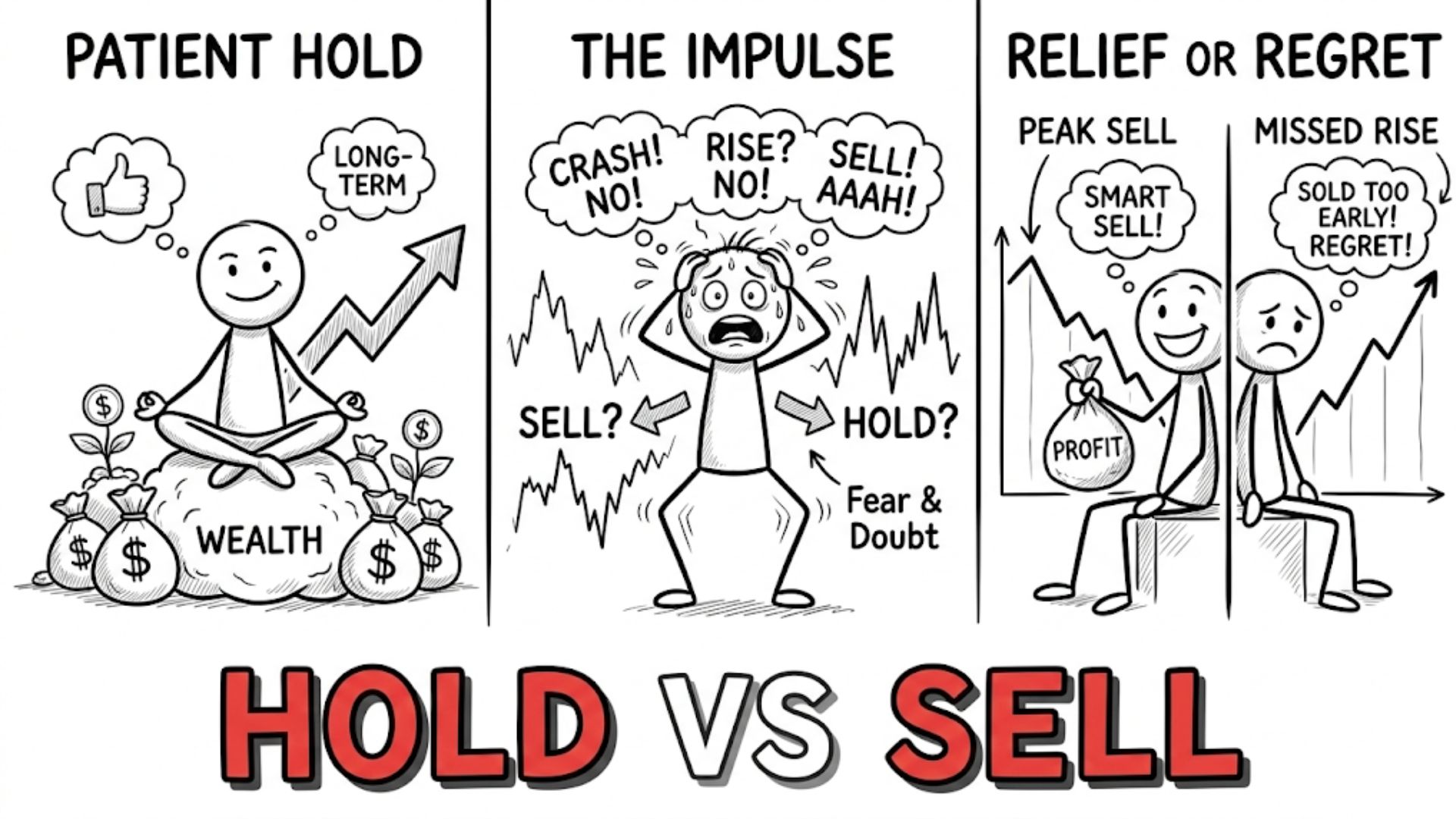

The decision to hold or sell an asset appears, on the surface, to be a technical judgment about valuation, risk, and expected return. In practice, it is also a psychological event. Market prices fluctuate continuously, but human tolerance for uncertainty does not. The tension between these two dynamics creates one of the central behavioral challenges in investing: the difficulty of remaining aligned with long-term objectives in the presence of short-term volatility.

Financial markets are structured as delayed payoff systems. Equity ownership, for example, represents a claim on future cash flows that unfold over extended periods. Yet prices are updated in real time, and these price movements are interpreted emotionally as gains or losses. The decision to hold or sell is therefore rarely neutral. It is filtered through cognitive biases, institutional incentives, and culturally reinforced norms of immediacy.

Impatience plays a central role in this dynamic. When evaluation horizons are compressed, temporary declines become intolerable, and modest short-term gains appear sufficient to justify exit. Over time, repeated short-horizon decisions undermine participation in compounding systems. The cumulative effect is not merely a missed opportunity but a structurally altered wealth trajectory.

Understanding the psychology of holding versus selling requires examining why time horizon misalignment persists, why impatience remains influential despite decades of financial education, and how broader incentive structures reinforce short-termism. The issue is not emotional weakness in isolation; it is the interaction between human cognition and systems that generate noisy, delayed feedback.

Read also: Why Cash Flow Thinking Beats Net Worth Obsession

The Core Problem: Time Horizon Misalignment

At the center of the holding-versus-selling dilemma lies a structural error: evaluating long-duration assets through short-duration feedback.

Most financial assets derive value from long-term productive activity. Corporations generate earnings over years. Real estate appreciates through demographic and economic shifts over decades. Even bonds reflect extended streams of contractual payments. However, these assets are priced daily, sometimes by the second. The result is a cognitive environment in which short-term price fluctuations are far more visible than long-term value creation.

Time horizon misalignment occurs when investors allow short-term price signals to dominate decisions that were initially justified by long-term expectations. If an asset is purchased with a ten-year thesis but evaluated on a weekly basis, variance becomes disproportionately influential.

This misalignment produces two symmetrical errors. First, investors may sell prematurely during downturns, interpreting temporary volatility as evidence of permanent impairment. Second, investors may sell early during moderate gains to secure short-term satisfaction, truncating potential long-term compounding.

The structural issue is not merely emotional discomfort but analytical compression. Short-term price changes contain a mixture of information and noise. Over short windows, noise dominates. When decisions are made within these compressed intervals, randomness exerts outsized influence.

The act of holding requires tolerating ambiguity. The act of selling provides closure. Impatience biases individuals toward closure, even when the long-term expected value favors endurance. Thus, time horizon misalignment converts normal market variability into a sequence of costly interventions.

Read also: The Difference Between Volatility and Risk

Why the Problem Persists Despite Experience

One might expect that repeated exposure to market cycles would attenuate reactive behavior. Historical data consistently show that markets recover from downturns over sufficiently long horizons. Yet impatience and frequent trading remain common. This persistence reflects structural reinforcement mechanisms rather than simple ignorance.

Feedback Loop Distortion

Financial markets generate immediate price feedback but delayed fundamental feedback. Earnings growth, productivity improvements, and competitive positioning evolve gradually. Price changes, by contrast, are instantaneous and highly salient.

This asymmetry distorts learning. Humans are adapted to environments where rapid feedback signals survival-relevant information. In markets, however, short-term price fluctuations are often random. The immediacy of these signals gives them disproportionate psychological weight.

As a result, investors may interpret volatility as actionable information rather than statistical noise. Selling becomes a response to perceived threat, even when underlying fundamentals remain intact.

Incentive Structures

Institutional incentives frequently reward short-term performance measurement. Portfolio managers may face quarterly evaluations. Corporate executives may be judged on annual earnings metrics. Media coverage emphasizes daily market movements.

These incentives rationally encourage shorter evaluation horizons. Professional survival can depend on avoiding short-term underperformance relative to benchmarks. This environment reinforces a culture in which frequent action is equated with diligence.

Individual investors are influenced by these norms. When financial discourse centers on short-term performance, holding for extended periods may appear inattentive or naive. Thus, institutional structures amplify psychological biases.

Present Bias and Short-Termism

Present bias—the tendency to overweight immediate outcomes relative to future ones—plays a central role in selling decisions. A current loss feels concrete and painful. A future recovery is abstract and probabilistic. The immediate relief of selling can outweigh the expected long-term gain of holding.

Similarly, realizing gains provides immediate satisfaction. The pleasure of locking in profit is experienced now; the uncertain prospect of larger future gains is discounted.

This temporal asymmetry explains why both panic selling and premature profit-taking persist. In each case, immediate emotional resolution competes with long-term value.

Cultural Reinforcement of Immediacy

Modern economic culture emphasizes responsiveness and optimization. Digital platforms provide real-time metrics and constant updates. Performance dashboards normalize continuous evaluation.

Within this context, holding an asset for years without frequent adjustment appears countercultural. Immediacy is equated with competence. Selling becomes a demonstration of engagement.

These structural forces ensure that impatience is not an isolated psychological trait but a culturally reinforced behavior pattern.

Read also: The Temporal Architecture of Markets: How Fear and Greed Drive Market Cycles

Real-World Consequences Across Domains

Although holding versus selling is most visible in financial markets, the underlying psychology extends to other domains involving delayed payoff systems.

Investing and Portfolio Stability

Frequent selling increases transaction costs, tax liabilities, and the probability of mistimed reentry. Because compounding depends on uninterrupted participation, repeated exits reduce exposure to exponential growth phases.

Moreover, selling during downturns often converts temporary mark-to-market losses into permanent capital impairment. The difference between volatility and loss becomes blurred when impatience dominates.

Career Development

In professional contexts, individuals may abandon career paths prematurely in response to short-term dissatisfaction or setbacks. Complex skills compound over time, but early progress is slow and uneven.

Switching trajectories frequently interrupts the accumulation of expertise and reputation. The psychological impulse to “sell” a career path mirrors portfolio behavior under volatility.

Entrepreneurship and Business Strategy

Entrepreneurs often face prolonged periods of uncertain revenue before achieving scale. Selling a business or abandoning a strategy prematurely may relieve short-term stress but foreclose long-term growth.

Corporate decision-makers similarly confront pressure to divest underperforming divisions quickly. While strategic exits can be rational, reactive selling driven by quarterly results may sacrifice future optionality.

Savings and Consumption

Selling assets to finance immediate consumption illustrates time horizon compression. The immediate utility of spending competes with the long-term security of retained capital. Present bias shifts weight toward current satisfaction.

Across these domains, the structural theme remains consistent: impatience interrupts compounding systems and alters long-term trajectories.

Read also: A Masterclass on Graham and Dodd’s “Security Analysis”

A Core Mental Model: Compounding and Delayed Feedback Systems

The mechanics underlying holding versus selling decisions can be illuminated through the mental model of compounding within delayed feedback systems.

Compounding systems generate nonlinear growth. Returns build upon prior returns, creating exponential trajectories over extended periods. However, early stages often appear unimpressive, and interim volatility obscures long-term direction.

Delayed feedback systems further complicate interpretation. Positive long-term trends may coexist with short-term declines. Observers operating on compressed timelines may misinterpret these fluctuations as evidence of structural failure.

Holding preserves participation in the exponential curve. Selling truncates it. Because exponential growth is highly sensitive to duration, even brief interruptions can materially alter final outcomes.

The psychological cost of holding—tolerating interim volatility—must be weighed against the mathematical cost of exiting. Compounding rewards endurance not because of moral virtue but because time itself amplifies incremental gains.

Understanding this model clarifies why simplicity often outperforms complex reactive strategies. Fewer interventions mean fewer disruptions to the compounding process.

Applying Better Thinking in Practice (Principles, Not Tactics)

Improved reasoning in holding-versus-selling decisions depends on structural alignment rather than emotional suppression.

First, evaluation horizons should correspond to the intended holding period. Long-term assets require long-term assessment frameworks. Short-term price movements should be contextualized within broader expectations.

Second, decision frequency should be minimized where feasible. Each decision introduces potential error. Reducing the number of discretionary sell points decreases exposure to bias.

Third, differentiation between volatility and fundamental deterioration is essential. Price movement alone does not necessarily imply impaired long-term value.

Fourth, awareness of incentive structures is necessary. If evaluation systems reward short-term outcomes, behavior will adapt accordingly. Recognizing these incentives allows for more deliberate interpretation of performance signals.

These principles aim to reduce structural misalignment rather than prescribe specific financial actions.

Read also: Financial Freedom From $2.26 to $1.25 Million in 5 Years

Common Misunderstandings About Patience

Patience is often conflated with passivity. Holding an asset does not imply ignoring new information or tolerating genuine structural decline. Rational reassessment remains necessary when underlying fundamentals change.

Another misconception is that long-term holding guarantees positive outcomes. Compounding increases probabilities but does not eliminate uncertainty. Structural shifts, technological disruption, and macroeconomic change can invalidate prior assumptions.

It is also incorrect to assume that emotional resilience alone solves the problem. Even disciplined individuals operate within systems that reward immediacy. Structural design—such as aligning evaluation intervals with asset duration—often matters more than temperament.

Clarifying these distinctions prevents oversimplified narratives about patience.

Connections to Broader Thinking Frameworks

The psychology of holding versus selling intersects with several broader conceptual frameworks.

Second-Order Effects

Selling to avoid short-term loss may reduce exposure to subsequent recovery phases. The second-order consequence of immediate relief is diminished long-term growth.

Incentive Design

Performance measurement shapes behavior. When evaluation emphasizes short-term variance, selling becomes more frequent. Aligning incentives with long-term objectives alters decision patterns.

Opportunity Cost

Time spent outside compounding systems carries opportunity cost. Missed periods of growth accumulate invisibly but materially.

Path Dependency

Early selling decisions influence future expectations and habits. A pattern of reactive selling can institutionalize short-termism, shaping long-term financial identity.

These frameworks situate individual psychology within systemic structures.

Read also: How an Insignificant Ape Conquered the World

Conclusion: Reframing Financial Success as a Time-Based System

The decision to hold or sell is not solely a matter of valuation. It is a confrontation between short-term perception and long-term reality. Impatience, reinforced by loss aversion, present bias, and institutional incentives, compresses evaluation horizons and magnifies volatility.

Financial success operates as a time-based system. Compounding rewards sustained participation and penalizes interruption. When short-term discomfort triggers premature selling, the cost is not limited to immediate loss; it includes forfeited time within exponential processes.

The persistence of reactive selling across generations reflects structural reinforcement rather than simple ignorance. Immediate feedback loops, cultural norms of responsiveness, and incentive designs that emphasize short-term metrics collectively sustain impatience.

Reframing holding versus selling decisions through the lens of time horizon alignment clarifies the central challenge. The essential question is not whether volatility will occur—it will—but whether evaluation frameworks are calibrated to the duration of underlying economic processes.

In long-duration systems, simplicity and endurance often prove structurally advantageous. By preserving exposure to compounding and minimizing behavioral interruption, holding becomes less an act of emotional fortitude and more a rational alignment with the mechanics of time.