Introduction: The Limits of Prediction

In the classical tradition of economic theory, the rational actor is often modeled as an engine of prediction. Decisions are framed as optimization problems: an individual gathers information, forecasts the probabilities of various future states, and selects the path that maximizes expected utility. This deterministic approach assumes that the primary barrier to success is a lack of data or computational power. The implicit belief is that if we could only model the world with enough precision, the “correct” decision would reveal itself.

However, as a systems thinker observing the trajectories of complex environments—from the volatility of capital markets to the non-linear path of technological innovation—I have come to view this reliance on prediction as a fundamental structural vulnerability. In reality, many of the most significant systems in our world are not merely “risky”; they are deeply uncertain. In these environments, the variables are too numerous, the feedback loops too intricate, and the “Black Swan” events too impactful for any predictive model to remain robust over time.

An alternative strategy, one far more aligned with the actual mechanics of uncertain systems, is the cultivation of optionality. Optionality is the architectural preservation of future possibilities. It is the strategy of maintaining the right, but not the obligation, to take an action. Instead of betting on a specific forecast, the strategist who prioritizes optionality structures their position to benefit from a wide range of favorable outcomes while strictly limiting their exposure to negative ones. In the economics of uncertainty, the ability to remain flexible and capture asymmetric upside is often more valuable than the illusory precision of a forecast.

Read also: The Deep Psychology of Inspiring Leadership and Brand Loyalty

Uncertainty vs. Risk

To understand the economic logic of optionality, we must first distinguish between “risk” and “uncertainty,” a distinction famously articulated by the economist Frank Knight.

Risk refers to situations where the outcomes are unknown, but the underlying probability distribution is known. A casino operates in a world of risk; while the house doesn’t know the result of the next spin of the roulette wheel, it knows the exact mathematical probability of every possible outcome. In such environments, prediction and optimization are highly effective.

Uncertainty, conversely, refers to situations where the probabilities themselves are unknown or unknowable. The future of a new industry, the long-term impact of a radical technology, or the trajectory of a global geopolitical shift falls into this category. In a state of uncertainty, there is no “roulette wheel” to calculate. The “sample space” is open-ended.

Optionality is the native strategy for uncertainty. While prediction requires a stable environment with a closed set of variables, optionality thrives on randomness. In fact, a position with high optionality is “long volatility”—it benefits when the environment becomes more turbulent, as turbulence increases the likelihood that one of the many potential upside paths will be realized, while the cost of the “option” remains fixed.

The Structure of Asymmetric Payoffs

The core of optionality’s value lies in the structure of asymmetric payoffs. In a linear system, the downside and upside are proportional. In an asymmetric system, they are decoupled.

In economic terms, this is often described as a convex payoff profile. A convex relationship is one where the benefits of an event grow faster than its costs. If we visualize this on a graph, the curve bends upward.

Optionality creates convexity by imposing a “floor” on losses while removing the “ceiling” on gains. This is the logic of a “trial.” If you perform an experiment that costs $100 but has a 1% chance of yielding $100,000, you have created an asymmetric payoff. You can afford to be “wrong” 99 times. The 99 failures do not aggregate into ruin; they are merely the “cost of the option.” The single success, however, changes the state of the entire system.

The strategist who prioritizes optionality is essentially a collector of these convex bets. They recognize that in an uncertain world, “being right” about the future is difficult, but “structuring the payoff” so that you don’t need to be right most of the time is a much more sustainable path.

Read also: Why Time Is the Most Underrated Competitive Advantage

Optionality in Financial Markets

Financial options provide the most legible conceptual model for this principle. A “call option” gives the holder the right to buy an asset at a specific price, but only if they choose to do so. If the price of the asset crashes, the holder’s loss is limited to the small premium paid for the option. If the price skyrockets, the holder participates in the entire upside.

This structure embodies the separation of knowledge and payoff. The holder of the option does not need to know when or why the market will move; they only need to know that the potential move is large relative to the cost of the option.

In a systemic sense, the “premium” we pay for optionality in life and business—whether it is maintaining a cash reserve, staying in a geographic hub, or acquiring a broad skill set—is the cost of the “insurance” against being wrong about the future. While this premium may look like “waste” or “inefficiency” in a stable environment, it is the only thing that preserves the entity when the environment shifts. Financial markets teach us that the value of an option increases as the time to expiration increases and as the volatility of the underlying environment increases. This is a profound insight: the more chaotic the world becomes, the more valuable flexibility becomes.

Entrepreneurship and Optionality

Entrepreneurship is frequently misinterpreted as the pursuit of a singular, visionary plan. However, a systems analysis of successful startups suggests that they function more like probabilistic exploration engines.

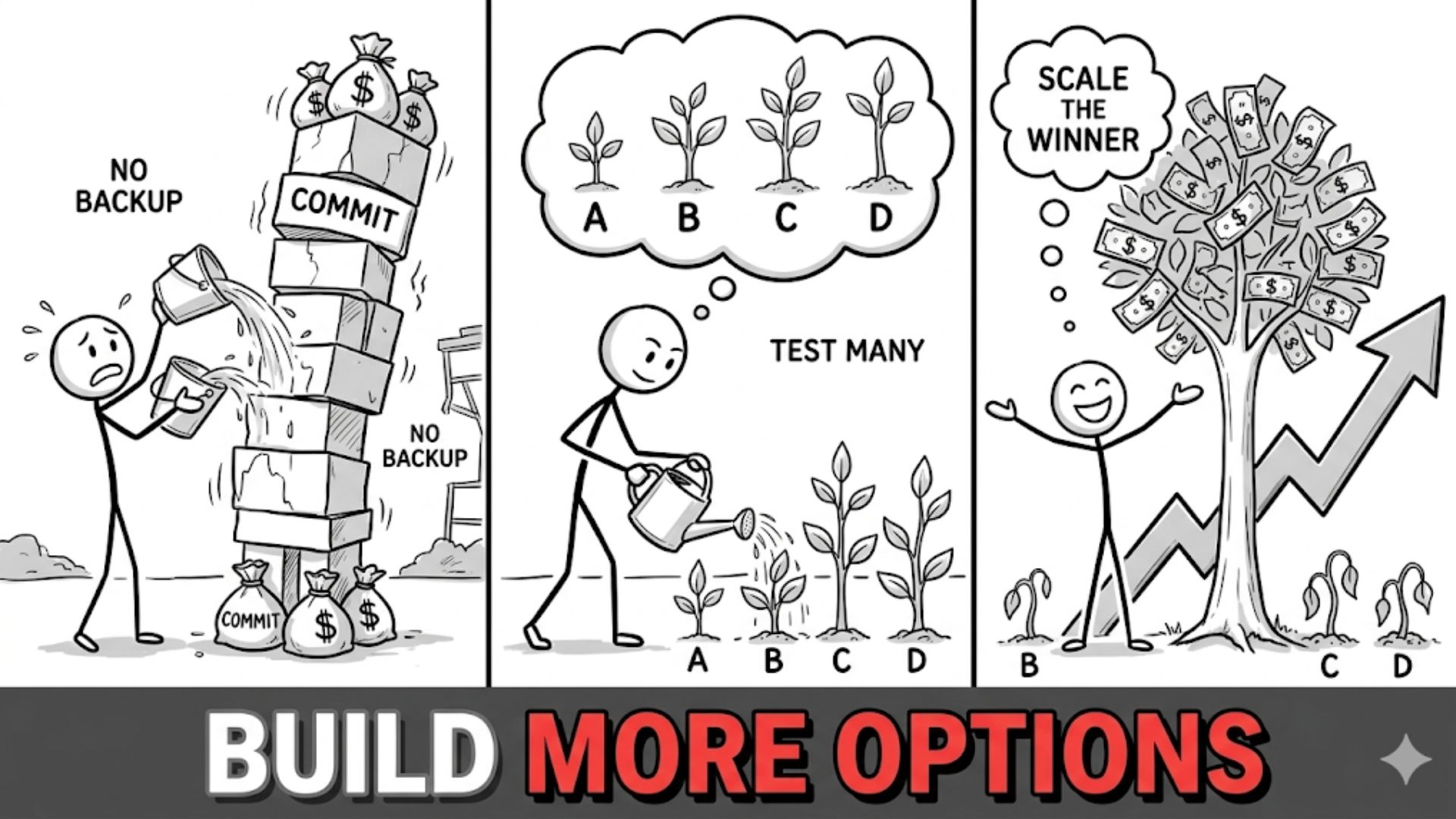

A nascent venture is essentially a bundle of options. Each product feature, marketing channel, or target demographic is a “trial.” Founders who over-optimize for a specific deterministic plan (a “pivot” is a sign of failure in this mindset) often exhaust their capital before finding a viable path. Conversely, the most resilient entrepreneurs treat their initial capital as a way to “buy” as many trials as possible.

This is why the concept of the “Minimum Viable Product” (MVP) is so vital. The MVP is a low-cost option. It allows the entrepreneur to test a hypothesis with limited downside. If the market rejects it, the “premium” lost is small. If the market accepts it, the upside is non-linear. Successful entrepreneurship is the process of harvesting the results of these small experiments and concentrating resources on the ones that show “convex” potential. In this sense, the venture capitalist is not a predictor of winners, but a manager of a portfolio of options, knowing that 90% of the portfolio will expire worthless while 1% will produce 1000x returns.

Read also: The Hidden Geometry of Long-Term Success

Career Optionality

The principle of optionality is perhaps most transformative when applied to human capital. In a linear era, the optimal career strategy was specialization: picking a narrow niche and climbing a predictable ladder. This was a “low-volatility” strategy that worked in a stable economic environment.

In an era of technological disruption and shifting market demands, specialization can become a “short volatility” position. If your value is tied to a specific, non-transferable skill that becomes obsolete, your downside is total. Career optionality, by contrast, is the strategy of building Career Capital that preserves future flexibility.

This is achieved through:

- Transferable Skills: Mastering foundational disciplines like mathematics, persuasive communication, or systems thinking. These are “Lindy” skills that remain valuable regardless of the specific industry.

- Broad Networks: Maintaining connections across disparate industries. A diverse network is a “source of options” for new roles or partnerships.

- Informational Advantages: Staying in high-interaction environments (hubs) where the “collision rate” of new ideas is high.

Career optionality allows an individual to avoid the “Sunk Cost Fallacy.” Because they have preserved their flexibility, they are not forced to go down with a sinking ship. They can “exercise the option” to pivot into a new domain when the environment changes.

Read also: A Structural Analysis of Time-Based Systems

Optionality Through Experimentation

Innovation is rarely a straight line from a problem to a solution. It is a stochastic process. The more “trials” a system can perform, the more likely it is to encounter a positive outlier.

Optionality is the economic justification for high-frequency, low-cost experimentation. In a corporate or scientific setting, a rigid “top-down” plan often kills innovation because it limits the sample space. It only explores the paths that the “planners” can imagine. However, “tinkering”—the act of making small, random adjustments—often leads to discoveries that no one could have predicted.

Consider the history of pharmaceuticals or materials science. Many of the most significant discoveries (e.g., penicillin, Teflon) were accidents. They were “side effects” of other experiments. The organizations that found them were those that had the “optionality” to recognize and capture the accident. If an organization is too focused on a specific predicted outcome, it becomes “blind” to the unexpected upside. Optionality requires the structural openness to let the environment “speak” and the agility to respond when it says something interesting.

Time and Optionality

Time is the “theta” of optionality. In finance, theta is the rate at which an option’s value decays as it approaches its expiration date. In life, time is the medium in which the “randomness” of the world has the chance to manifest.

A long time horizon is a significant “optionality multiplier.” If you are in a high-exposure state—such as living in a dynamic city or being active in a growing industry—the longer you stay there, the more likely you are to encounter a “once-in-a-decade” opportunity. Patience, in this context, is not just a virtue; it is an economic strategy. It is the act of keeping your “options” open long enough for the statistical “tails” to occur.

However, optionality also requires the avoidance of “absorbing barriers.” In systems theory, an absorbing barrier is any event that results in “ruin” (e.g., bankruptcy, total reputational collapse). Once you hit the barrier, your optionality drops to zero because you are no longer in the game. Strategic duration, therefore, requires a combination of aggression in seeking upside and paranoia in avoiding downside.

Optionality and Innovation Systems

Scientific and technological progress is often viewed through the lens of the “Heroic Inventor.” A more accurate view is that progress is the result of an Innovation Ecosystem that maintains high optionality.

In a healthy innovation system, multiple competing paths are explored simultaneously. No one knows which path will yield the “Next Big Thing,” so the system “buys” options on all of them. This is the logic behind decentralized markets. Unlike a centralized “Command Economy,” which bets the entire national capital on a few predicted sectors, a market economy allows thousands of individuals to “buy” small options on their own ideas.

This decentralized exploration is far more robust because it is “antifragile.” The failures of individual experiments provide information to the rest of the system without causing it to collapse. The system “learns” from the “options” that expire worthless, gradually concentrating energy on the “options” that show promise. Innovation is the harvesting of this collective optionality.

Read also: Why Acquisition Entrepreneurship Is the Ultimate Business Mental Model

Why Humans Often Reject Optionality

If optionality is so structurally superior in uncertain worlds, why do most people reject it in favor of “linear” paths? The reasons are rooted in our psychological architecture and the biases identified by behavioral economics.

- The Illusion of Certainty: Humans have a profound psychological need for a sense of control. A “plan” (even a wrong one) provides an emotional comfort that “maintaining flexibility” does not. We prefer the “map” to the “terrain.”

- Loss Aversion: To maintain optionality, one must often pay a small, constant cost—the “premium.” We might have to take a lower-paying job that offers more learning, or keep cash in a low-interest account. Loss aversion makes us focus on the “small loss” of the premium today rather than the “massive gain” of the option tomorrow.

- Discomfort with Ambiguity: Optionality is “messy.” It requires living in a state of “not knowing” which path will work. Most people find this ambiguity cognitively exhausting and will “force” a decision just to end the tension.

Institutional Constraints on Optionality

Institutions are frequently designed to minimize optionality. Bureaucracies thrive on legibility, predictability, and standardization.

- Rigid Career Ladders: Institutions often force employees into “up-or-out” tracks. This reduces the employee’s ability to explore “side paths” that might lead to radical innovation.

- Short Performance Cycles: Quarterly reporting and annual reviews force a focus on “visible results.” Optionality, as we have noted, often involves “invisible progress” (buying the option) for long periods before the payoff.

- Centralized Decision-Making: When decisions are made at the top, the organization is limited by the “optionality” of a few leaders. It loses the “wisdom of the crowd” and the “distributed exploration” of the frontline.

These constraints create Institutional Fragility. By optimizing for the “seen” efficiencies of today, these organizations lose their “unseen” flexibility for tomorrow. When a radical disruption occurs, they have no “alternative paths” ready to exercise.

Read also: A Structural Analysis of Compounding in Life Systems

Optionality and Unequal Outcomes

Systems driven by optionality do not produce “fair” or “even” outcomes. They produce Power Laws.

Because optionality relies on capturing extreme outliers (the 1000x gain), the majority of participants in an optionality-driven system (like Venture Capital, acting, or book publishing) will experience “failure” in the sense that their individual options will expire worthless. The value of the entire system is concentrated in the “top 1%.”

This “Winner-Take-Most” dynamic is an inherent feature of non-linear growth. If you are playing a game of optionality, you must be prepared for the statistical reality that most of your experiments will not work. Success is not a matter of having a high “batting average,” but a high “slugging percentage.” This inequality is the price of the asymmetric upside that the system provides.

Viewing Economic Systems Through Optionality

Reframing economic systems through the lens of optionality allows us to see patterns that are invisible to linear models.

- Venture Capital: It is not about picking winners; it is about paying a small premium (the seed check) for a “call option” on a massive future market.

- Agglomeration Economies (Cities): Cities are “option markets.” They offer a high density of people and ideas, which increases the “collision rate” and provides the resident with more “career options” than a remote location.

- Open Source Software: It is a massive “collective option.” By making the code free, the creators allow thousands of other people to “tinkerer” with it, increasing the probability that someone will find a transformative new use case.

Read also: The Research-Backed Blueprint for Building Truly Great Companies

Conclusion: Optionality as a Strategic Framework

In the final analysis, the pursuit of optionality is an act of intellectual humility. it is an admission that the world is more complex than our models, and that our ability to predict the future is fundamentally limited.

In a stable, linear world, efficiency and specialization are the dominant strategies. But we do not live in that world. We live in a world of non-linear feedback loops, “Black Swan” events, and radical uncertainty. In such a world, the most expensive mistake is not being “wrong”; it is being “fragile”—having no alternatives when your primary plan fails.

Optionality is the structural solution to fragility. By building systems that are “long on volatility” and “asymmetric in payoff,” we can move past the paralyzing need for perfect prediction. We don’t need to know which path the world will take. We only need to ensure that we have “options” on enough of those paths to benefit from the movement of the world, whatever direction it chooses. The future belongs not to those who “see” it most clearly, but to those who have built the most “convex” relationship with it.