In my years of studying economic systems and the mechanics of capital allocation, I have observed a recurring phenomenon that appears with remarkable consistency across cultures, industries, and historical epochs. Whether examining the landholdings of 15th-century Florence, the equity distributions of modern Silicon Valley, or the global concentration of financial assets in the 21st century, the pattern remains largely the same: wealth is rarely distributed according to a normal “bell curve.” Instead, it follows a highly skewed trajectory where a small fraction of the population controls a disproportionately large share of the resources.

This observation invites a rigorous, non-ideological inquiry. Why do economic systems, regardless of their specific political or social underpinnings, repeatedly produce such uneven outcomes? While social and political factors certainly play a role in shaping the environment, they often act as modifiers to a more fundamental set of mathematical and systemic drivers. To understand wealth inequality at its root, one must look toward the mechanics of compounding returns, cumulative advantage, and the non-linear nature of growth in complex systems.

Read also: The Step-by-Step Guide to Discovering Your Purpose

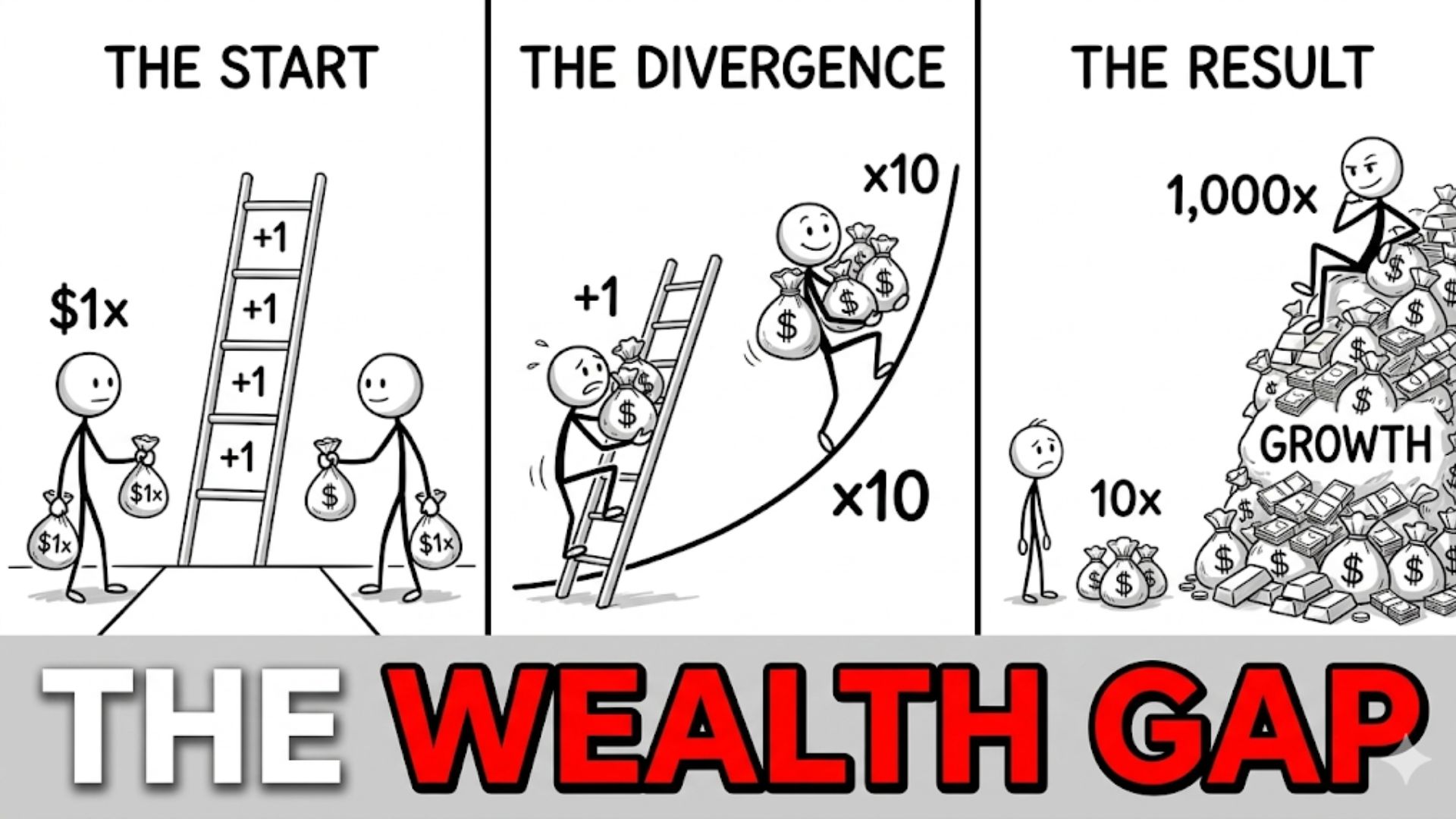

Linear Effort vs. Nonlinear Outcomes

A common cognitive bias in human reasoning is the expectation of linearity. We are biologically and socially conditioned to expect that outcomes should correlate roughly with effort or immediate productivity. In a linear world, if Individual A works twice as hard as Individual B, we expect Individual A to possess twice the resources. This model works well for manual labor or discrete tasks, but it fails to account for the structural reality of wealth accumulation.

Real-world wealth accumulation behaves nonlinearly. It is not merely an additive process of saving wages; it is a multiplicative process governed by reinvestment. When a system allows the “output” of one period to become the “input” for the next, the relationship between effort and outcome decouples. A small initial difference in capital or a slightly higher rate of return does not produce a slightly different outcome over time; it produces a fundamentally different order of magnitude in wealth.

Read also: The Strategic Power of Thinking in Decades

Small Advantages Become Large Outcomes

This divergence is further accelerated by a mechanism known as cumulative advantage, or the “Matthew Effect.” Named after the biblical parable, this principle suggests that “to those who have, more will be given.” In systems theory, this is described as a state where an initial advantage provides the means to acquire further advantages, creating a self-reinforcing cycle.

In the context of wealth, small differences in starting conditions—such as a modest inheritance, access to a high-quality education, or even an early-career informational edge—set a person on a different compounding trajectory. Because the system is path-dependent, an advantage in Year 1 makes it easier to capture an advantage in Year 2. Conversely, those starting with zero or negative capital (debt) must spend the most productive years of their lives simply reaching the “zero-point” where compounding can begin. The “gap” is not just a matter of current bank balances; it is a matter of the “slope” of the growth curve.

Read also: The Deep Psychology of Inspiring Leadership and Brand Loyalty

Positive Feedback Loops in Wealth Systems

The reason cumulative advantage is so potent in economic systems is the presence of positive feedback loops. Wealth is not just a store of value; it is a tool for the acquisition of more wealth.

Consider the following mechanisms:

- Investment Access: Many of the highest-yielding asset classes, such as private equity, venture capital, or large-scale real estate, require significant minimum capital entries. Wealthy individuals can access “r” values that are structurally unavailable to those with less capital.

- Financial Leverage: The ability to borrow capital to invest (leverage) allows those with existing assets to multiply their exposure to growth. If an investor uses 20% of their own money and 80% borrowed money to buy a growing asset, their personal “r” is effectively quintupled.

- Informational Advantages: Wealth buys time and expertise. It allows for the hiring of analysts, tax strategists, and legal counsel who can identify inefficiencies and protect capital from “leaks” like taxes or inflation.

These loops ensure that those who are already positioned on the upper end of the distribution find it structurally easier to stay there and move further ahead. Each successful turn of the feedback loop increases the “principal” for the next turn, making the subsequent growth even more dramatic.

Power-Law Distributions and Economic Systems

When these mechanisms of compounding and feedback loops are allowed to run across a large population over many cycles, the resulting wealth distribution typically follows a “Power Law” (or Pareto Distribution). Unlike the bell curve (Normal Distribution), where most people are near the average, a power-law distribution is characterized by a “long tail” and a heavy concentration at the top.

In such a distribution, the “average” wealth is a meaningless statistic because the mean is heavily skewed by the extreme outliers. This is why we often see the “80/20 rule,” where 20% of the participants own 80% of the assets. In more extreme cases, it may become 99/1. This is not necessarily a sign of a “broken” system, but a predictable mathematical outcome of any system where:

- Growth is proportional to current size (compounding).

- Advantages are reinvested (feedback loops).

- There are no significant “dampening” forces to reset the principal.

Read also: A Visual Guide for First-Time Entrepreneurs

Time Horizons and Wealth Accumulation

One of the most underrated variables in the mathematics of inequality is the time horizon (t). Because compounding is end-loaded—meaning the most significant growth happens in the final stages of the process—wealth systems disproportionately reward those who can remain invested for the longest periods.

An individual who can leave their capital untouched for 50 years will experience a vastly different outcome than one who must liquidate their assets every five years to cover life expenses. Wealthy families and institutions often operate on multi-generational time horizons, allowing t to grow far beyond the span of a single human career. In this sense, time acts as a multiplier of initial capital advantages. Inequality persists because the “holding power” of a large principal allows it to survive market volatility and capture the full verticality of the exponential curve.

Path Dependency in Financial Outcomes

Wealth trajectories are highly path-dependent. This means that early decisions and events have a disproportionate impact on the final destination. A single “Type 1” decision—such as entering a specific high-growth industry, starting to save at age 20 versus age 30, or avoiding a catastrophic debt trap—can alter the “exponent” of a person’s life.

Because the early years of compounding are the foundation for the later years, the “cost” of a mistake at age 25 is much higher than at age 55. This path dependency creates a structural “lock-in.” Once a person falls behind the compounding curve of their peers, the mathematics required to “catch up” become nearly impossible, requiring “r” values (returns) that are statistically improbable without extreme risk.

Read also: Why Time Is the Most Underrated Competitive Advantage

Network Effects and Economic Advantage

While wealth is often viewed as a balance sheet of assets, it is also a function of social and informational networks. Network effects describe a system where the value of a node increases with the number of other nodes it is connected to.

High-wealth individuals often occupy central nodes in professional and informational networks. These networks reinforce existing advantages by:

- Providing early access to “deal flow” (investment opportunities).

- Reducing transaction costs through trust-based relationships.

- Allowing for the rapid synthesis of complex market information.

Networks, like capital, are subject to cumulative advantage. Those who are already connected find it easier to make new connections, leading to a “rich-get-richer” dynamic in social capital that mirrors the dynamic in financial capital.

Read also: The Hidden Geometry of Long-Term Success

Institutional Structures and Wealth Dynamics

While the mathematics of growth are universal, the institutions of a society can either dampen or reinforce these trends. Capital markets, for instance, are the ultimate compounding machines; they allow for the fractional ownership of productive enterprises, meaning capital can grow even when the owner is not working.

Inheritance systems are another critical institutional driver. They allow for the reset of the t variable to zero without resetting the P variable. By allowing wealth to cross generations, the compounding process is never interrupted by the death of the individual. Corporate ownership structures, which allow for the indefinite accumulation of assets within a legal entity, function similarly. These institutions provide the legal framework that allows the underlying mathematical laws of power-law distributions to operate over centuries.

Read also: A Structural Analysis of Nonlinear Progress

The Illusion of Sudden Wealth

To the outside observer, wealth often appears to emerge “suddenly.” We see the IPO of a tech company or the sudden ascent of a billionaire and attribute it to luck or a singular moment of genius. However, from a systems perspective, these “breakthroughs” are usually the result of a long, invisible accumulation phase.

An entrepreneur may spend ten years building a “principal” of skills, code, and relationships with zero visible wealth. When the “inflection point” occurs, the curve goes vertical, and they appear to have become wealthy overnight. In reality, they were merely traversing the “flat” part of the exponential curve. The public only notices the wealth when it reaches the vertical stage, leading to a systematic underestimation of the duration and consistency required for compounding to function.

Read also: A Structural Analysis of Time-Based Systems

Opportunity Asymmetry

A fundamental structural source of inequality is opportunity asymmetry. Capital does not just grow; it provides “optionality.” Someone with $10 million in liquidity has the option to invest $1 million into a high-risk, high-reward venture (like a seed-stage startup) that could return 100x. If the investment fails, their lifestyle is unaffected.

For someone with $10,000, that same opportunity is inaccessible. Not only do they lack the minimum “buy-in,” but they cannot afford the risk of loss. This “asymmetry” means that the wealthy are not just earning more on their money; they are playing an entirely different game with different rules and higher potential “r” values. This structural reality ensures that wealth continues to concentrate at the top, as the most asymmetric growth opportunities are reserved for those who already possess significant capital.

Why Inequality Persists Across Generations

The persistence of wealth inequality across generations is often analyzed through a social lens, but it has a clear mathematical basis. Wealthy families transmit a “bundle” of compounding assets:

- Financial Principal (P): Through inheritance and trust funds.

- Human Capital: Through access to elite education and specialized training.

- Social Capital: Through entry into high-value networks.

When these three factors are combined, the next generation starts their compounding process at a “principal” level that is already higher than the terminal wealth of most other individuals. The ” Matthew Effect” is thus extended beyond the lifespan of a single human, creating a “dynastic” compounding effect where the wealth gaps between families widen over centuries.

Read also: Why Acquisition Entrepreneurship Is the Ultimate Business Mental Model

Viewing Wealth Through Mathematical Systems

When wealth inequality is viewed through the lens of mathematical systems, it becomes easier to understand as a structural outcome rather than a moral failure or a temporary anomaly. If you have a system where:

- Returns are a percentage of existing size ($r \times P$).

- Information and opportunity are unequally distributed.

- Feedback loops are positive and reinforcing.

- Time horizons are long.

Then a power-law distribution is the mathematically inevitable result. Even if every individual started with the exact same amount of money and the same level of intelligence, random “shocks” (luck) would eventually create small differences. Compounding would then take those small differences and amplify them until the distribution looked exactly like the one we see in the real world today.

Read also: A Structural Analysis of Compounding in Life Systems

Conclusion: The Structural Logic of Unequal Outcomes

In the final analysis, wealth inequality is a product of the structural logic of growth systems. It emerges from the intersection of compounding returns, cumulative advantage, and non-linear feedback loops. While societies may choose to implement policies to redistribute wealth or alter the institutional “r” values, the underlying mathematical pressure toward concentration remains constant.

Understanding the mathematics of wealth is not about making a political argument for or against inequality; it is about recognizing the fundamental laws that govern resource distribution in complex, path-dependent systems. In a world where capital can be reinvested and time acts as a multiplier, the “natural” state of wealth is not equality, but a highly skewed distribution. The divergence we observe is the long-term signature of the power of the exponent—a force that, once set in motion, reshapes the economic landscape with a relentless, geometric precision.