Introduction: The Underestimation of Marginal Gains

In the study of capital allocation and economic systems, there exists a pervasive cognitive bias toward the “breakthrough event.” Both individual investors and institutional decision-makers tend to prioritize high-visibility, dramatic actions—such as the identification of a “unicorn” startup, a perfectly timed market exit, or a radical strategic pivot—as the primary drivers of wealth and success. However, a rigorous analysis of long-term outcomes suggests a different reality. The most significant divergences in financial trajectory are rarely the result of singular, high-magnitude events, but are instead the product of small, consistent advantages compounded over extended durations.

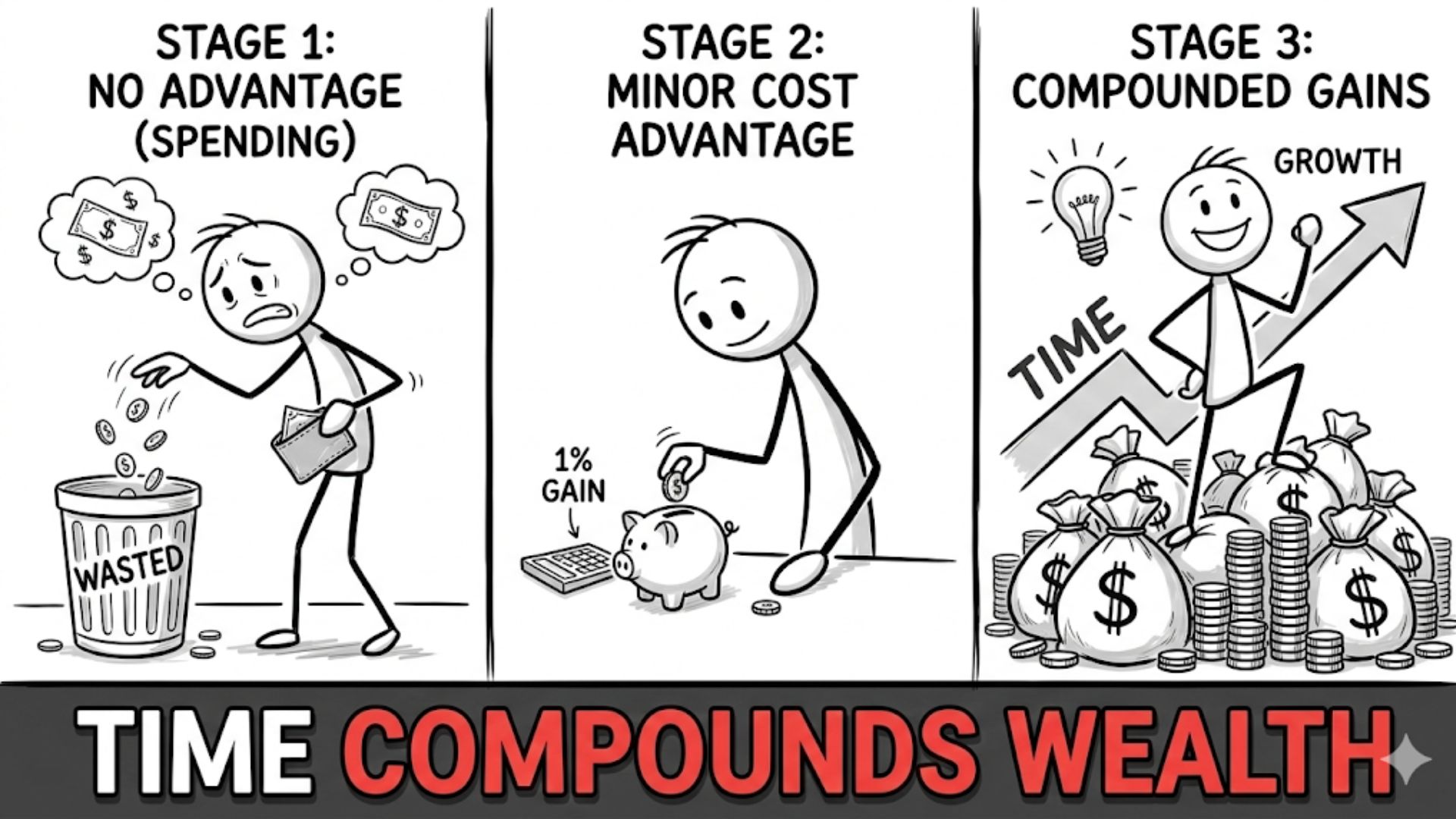

The central paradox of marginal gains is that they appear statistically insignificant within a short-term evaluation window. A 1% improvement in tax efficiency, a 50-basis-point reduction in investment fees, or a marginal increase in a savings rate exerts almost no discernible impact on a portfolio over a twelve-month horizon. Yet, because compounding is a non-linear process, these minor percentage differences act as the primary architecture of long-term asymmetry. The stakes of compounding are structural: over decades, a small edge does not merely result in “more” capital; it results in a fundamentally different order of magnitude in terminal wealth and strategic optionality.

Defining Small Financial Advantages

In economic terms, a “small advantage” is any marginal improvement in the efficiency of capital or labor that is repeatable and sustainable. Unlike “alpha”—the temporary exploitation of market inefficiencies that tends to mean-revert—a structural advantage is embedded in the process of allocation.

Categories of Marginal Edges

These advantages generally fall into three categories:

- Cost Efficiency: The systematic reduction of frictional losses, such as management fees, transaction costs, or administrative overhead.

- Allocative Precision: Marginal improvements in the “spread” between cost of capital and return on capital, often achieved through superior tax planning or better-calibrated risk assessment.

- Human Capital Compounding: The incremental accumulation of skills, reputation, and network density that increases the “yield” on a professional’s time.

The defining characteristic of these edges is that they are structural rather than tactical. A tactical gain is a one-time win; a structural advantage is a permanent shift in the “growth rate” variable of the compounding equation. While the magnitude of the shift is small, its persistence ensures that it eventually dominates the outcome.

Read also: The Psychology of Holding vs Selling Assets

The Core Mechanism: Compounding in Non-Linear Systems

The mathematical foundation of small advantages is the geometric progression. In a linear system, an improvement in input produces a proportional improvement in output. In a compounding system, however, the output of one period becomes the base for the next.

Exponential Growth Dynamics

The formula for future value ($FV = PV(1 + r)^t$) reveals that while the principal ($PV$) is a linear multiplier, the rate of return ($r$) and time ($t$) are exponential components. A small advantage—for example, increasing $r$ from 7% to 8%—does not result in an 11% increase in terminal wealth. Over a 40-year horizon, that 1% difference results in a nearly 50% increase in the final amount.

Consistency Over Magnitude

Compounding magnifies consistency more than magnitude because volatility is an “entropy” that taxes geometric growth. A system that earns a consistent, modest return with low frictional costs will almost always outperform a high-variance system with higher costs, even if the high-variance system achieves higher occasional peaks. Small advantages are effectively “volatility dampeners” and “frictional reducers” that allow the geometric engine to run uninterrupted. The power of the edge lies not in its size, but in its ability to stay “in the game” longer.

Time Horizon Misalignment and the Discounting of Marginal Gains

If the power of marginal gains is mathematically demonstrable, why are they systematically undervalued? The primary cause is the mismatch between the “sampling rate” of human perception and the “maturation rate” of compounding.

Read also: Why Simplicity Wins in Personal Finance

Present Bias and Temporal Discounting

Human biology is optimized for immediate feedback. In an ancestral environment, a 1% improvement in a future resource was abstract and valueless compared to a certain resource today. Behavioral economics identifies this as hyperbolic discounting: we discount the future at an extreme rate in the near term, only to flatten the discount curve in the distant future. Because the benefits of a small advantage are “back-loaded”—occurring mostly in the final 20% of the time horizon—they are perceived as having near-zero present value by the impulsive limbic system.

The Crowding Out of Signal by Noise

In any given year, the “signal” of a 1% advantage is entirely obscured by market “noise” (volatility). If the market moves 15% in a year, an investor finds it psychologically difficult to care about a 0.5% fee reduction. Short-term metrics—quarterly earnings, annual performance reviews, and monthly portfolio statements—crowd out the long-term signal. Consequently, decision-makers often abandon a structurally superior but “quiet” strategy in favor of a “loud” but inferior one that promises immediate, albeit unsustainable, results.

Incentive Structures and Structural Neglect

Institutional environments are frequently architected to reward the “bold stroke” over the “marginal gain.” This is driven by the Principal-Agent problem and the cultural economy of attention.

Quarterly Reporting and Political Horizons

In corporate and political spheres, the evaluation window is significantly shorter than the compounding window. A CEO or a policymaker is often incentivized to produce visible, immediate “wins” to satisfy shareholders or voters. A marginal improvement in operational efficiency that takes a decade to realize its full value is unattractive to an agent who expects to be in their role for only four years. The agent reaps the political or financial cost of the “effort” today, while their successor reaps the “benefit” tomorrow.

Read also: How Loss Aversion Impacts Portfolio Decisions

The “Heroic Narrative” Bias

Media and institutional cultures reinforce this by focusing on “events” rather than “processes.” An acquisition that increases revenue by 20% is a headline; a tax strategy that increases net margin by 1.5% is an asterisk. This narrative bias leads to the misallocation of talent and capital toward high-magnitude, low-probability events, while the “boring” structural edges that provide the highest risk-adjusted returns go ignored.

Feedback Loop Distortion and Perception Bias

Learning and persistence require feedback. However, in compounding systems, the feedback loops are distorted by time and noise.

Delayed Reinforcement

In a skill-based task like tennis or coding, the feedback is immediate. In capital allocation, the feedback for a “small advantage” may be delayed by a decade. Without immediate reinforcement, the commitment to a marginal gain weakens. This is a problem of reinforcement learning: if the “reward signal” is too far removed from the “action,” the brain fails to associate the two, leading to the abandonment of the discipline.

The Illusion of Stagnation

During the early stages of compounding, the growth curve is nearly flat. An individual who increases their savings rate or optimizes their cost structure may see no change in their lifestyle or status for years. This “plateau of latent potential” creates a perception of stagnation. Decision-makers often mistake this lack of visible progress for a failure of strategy, unaware that they are simply in the linear phase of a non-linear process.

Path Dependency and Early Divergence

Small advantages are most powerful when applied early, due to the principle of path dependency. A decision made at the beginning of a trajectory has an outsized influence on the terminal state.

The Fan-Out Effect

Consider two individuals with identical skills and income. One chooses a cost-efficient investment path with a 1% fee; the other chooses a “premium” path with a 2% fee. For the first five years, their lives are indistinguishable. By year thirty, however, the paths have “fanned out” so significantly that the first individual possesses double the capital of the second. This early divergence creates irreversibility: the second individual cannot “work harder” to catch up, as they have lost the most valuable asset in compounding—time.

Read also: The Cost of Overconfidence in Investing

Optionality and Leverage

Small early advantages create “positive path dependency.” As capital or skills accumulate marginally faster, the individual gains optionality—the ability to take advantage of unexpected opportunities. The person with a slightly higher “buffer” can survive a downturn that bankrupts a peer, or they can afford the “entry fee” for a high-leverage investment that their peer cannot. In this way, a first-order marginal gain (cost saving) produces a second-order strategic gain (optionality).

Domains Where Small Advantages Compound

The structural impact of marginal gains can be observed across various economic and professional domains.

- Investment Fees: A 1% management fee “consumes” approximately 25% to 33% of a portfolio’s potential terminal value over a 30-year horizon. The “small” fee is, in reality, a massive transfer of wealth from the principal to the agent.

- Tax Efficiency: Utilizing tax-advantaged accounts or loss-harvesting strategies creates a marginal “return” that is risk-free and government-guaranteed. Over decades, the compounded value of these “unpaid taxes” often exceeds the initial principal.

- Business Margins: In highly competitive industries, the “best” company is often only 2% or 3% more efficient than its peers. However, that 2% difference in margin allows the company to re-invest more in R&D, offer slightly better pricing, and eventually achieve a dominant, “winner-take-all” market share.

- Career Skill Stacking: In professional development, the “top 1%” are rarely the best in the world at one thing. They are often “top 20%” in three or four complementary skills (e.g., engineering + sales + public speaking). The marginal advantage of being “pretty good” at an extra skill creates a unique, non-commodity profile with immense pricing power.

- Network Accumulation: The marginal effort of maintaining a professional network—one additional high-value contact per month—results in a geometric increase in “surface area for luck.” After ten years, the network effect creates a flow of opportunities that no amount of linear “searching” can replicate.

Read also: Why Long-Term Thinking Is a Financial Advantage

Second-Order and Third-Order Effects

The power of small advantages lies not just in the capital they accumulate, but in the “behavioral shifts” they enable.

Risk Tolerance and Resilience

A small advantage in cost structure provides a higher “margin of safety.” This resilience allows the decision-maker to maintain their position during a market crash, whereas a peer with higher costs may be “forced” to sell. The second-order effect of the small advantage is the prevention of a “permanent impairment of capital.”

Reputation and Trust

In professional systems, consistency is a small advantage that compounds into a “reputational moat.” A professional who is 5% more reliable than their peers over a decade becomes the “default choice” for high-stakes projects. This third-order effect is the removal of competition; the individual no longer has to “bid” for work because their reputation acts as an automated “pre-selection” mechanism.

Why Small Advantages Are Rarely Sustained

Maintaining a marginal edge is cognitively and socially taxing. Most individuals and institutions fail to sustain them not because they are difficult to understand, but because they are difficult to endure.

Cognitive Overload and Decision Fatigue

Monitoring marginal gains—checking fees, optimizing taxes, or refining skills—requires constant, “low-intensity” attention. In an environment of information overload, most people default to “good enough.” They pay the “convenience tax” of sub-optimal structures to reduce cognitive load. Over time, these convenience taxes aggregate into a massive loss of terminal value.

Cultural Preference for “The New”

There is a social status associated with “breakthroughs” and “disruption.” There is no social status associated with having a 10% higher savings rate than your neighbor for twenty years. Cultural norms favor the “sprinter” over the “compounder.” Maintaining a marginal advantage often requires a “contrarian” mindset—the willingness to appear boring or overly-detailed to one’s peers.

Read also: How Anchoring Bias Affects Financial Choices

Common Misunderstandings About Compounding

A failure to distinguish between the “math” and the “myth” of compounding leads to strategic errors.

- Risk vs. Return: Many believe that high terminal wealth requires high-risk “bets.” In reality, small advantages often come from reducing risk and reducing friction. Compounding works best when the “ruin probability” is zero.

- The Triviality Fallacy: The assumption that “it’s only 1%, it doesn’t matter” is the most expensive mistake in finance. In compounding systems, 1% is not a measure of size, it is a measure of velocity.

- Linear Expectation: Most people expect linear feedback. When they don’t see results in year two, they assume the strategy is failing. Strategic durability requires “expecting the plateau” as a necessary precursor to the exponential phase.

Structural Principles for Long-Term Advantage

To exploit the power of small advantages, one must move from tactical action to structural discipline.

- Time Horizon Expansion: All small advantages require a “long runway.” If the time horizon is short, the marginal gain is genuinely trivial. Strategic advantage begins when the evaluation window is extended beyond the “noise.”

- Friction Minimization: Before seeking higher returns, one should optimize for lower costs. Taxes, fees, and transaction costs are “guaranteed” negative compounding. Minimizing them is the most reliable “small advantage” available.

- Optionality Preservation: Small advantages should be used to build “buffers” rather than just “consumption.” A buffer provides the optionality to survive “Black Swan” events, which is the ultimate requirement for long-term compounding.

- Incentive Alignment: For institutions, success requires aligning the “agent’s” reward with the “system’s” long-term growth. This often involves deferred compensation or “skin in the game” that matches the duration of the asset.

Broader Conceptual Connections

The study of small advantages connects multiple high-authority frameworks:

- Systems Theory: A system’s long-term behavior is determined by its “feedback loops” and “rates of change.” Small advantages are the “tuning” of these variables.

- Opportunity Cost: The cost of a 1% sub-optimal allocation is not the 1% itself, but the “counter-factual” terminal wealth that was never created.

- Intergenerational Wealth Dynamics: Small advantages are the primary mechanism for the “divergence of dynasties.” Over multiple generations, minor differences in capital allocation discipline result in total economic stratification.

Read also: Why Cash Flow Thinking Beats Net Worth Obsession

Conclusion: Small Edges as Strategic Leverage

Financial dominance is rarely the result of “beating the market” through superior prediction. It is, instead, the result of “beating the process” through superior structure. The power of small advantages—marginal improvements in cost, efficiency, and skill—is the ultimate leverage in a non-linear world. These edges are valuable precisely because they are quiet, boring, and structurally difficult for the impatient majority to sustain.

Reframing financial success as a function of duration and consistency rather than intensity and luck allows the decision-maker to focus on the variables they can control. In the final analysis, the most significant strategic advantage is not a faster reaction time, but a more disciplined time horizon. The small advantage is the “seed” of the exponential curve; its power lies not in its initial size, but in the relentless, uninterrupted logic of the time that follows.