1. The Architecture of Escalation: An Analytical Inquiry into Lifestyle Inflation

The phenomenon of lifestyle inflation—the incremental and often unconscious escalation of consumption in response to rising income—remains one of the most pervasive structural obstacles to long-term capital accumulation. Despite significant advancements in financial literacy and the availability of sophisticated investment tools, the tendency for individuals and organizations to increase their fixed costs in lockstep with their earnings persists across diverse economic environments. This pattern is not merely a failure of individual discipline; it is the result of a complex interplay between neurobiological imperatives, social signaling mechanisms, and systemic feedback loops.

To understand lifestyle inflation is to recognize it as a fundamental problem of intertemporal choice. It represents a recurring decision-making error where immediate utility is prioritized over the expanded optionality provided by deferred consumption. When unchecked, this escalation creates a “lock-in” effect, where the individual remains tethered to a high-earning requirement to sustain a baseline of perceived necessity. The long-term consequences are profound: a reduction in the “margin of safety,” the erosion of career optionality, and the systematic neutralization of the benefits of compounding.

2. The Core Mechanism: Intertemporal Choice and the Baseline Shift

At its foundational level, lifestyle inflation is driven by the dynamic interaction between rising income and the psychological perception of “baseline needs.” In economic terms, this is often analyzed through the lens of income elasticity of demand. For many individuals, goods that were previously categorized as “luxuries” are rapidly reclassified as “necessities” as disposable income increases.

The Elasticity of Necessity

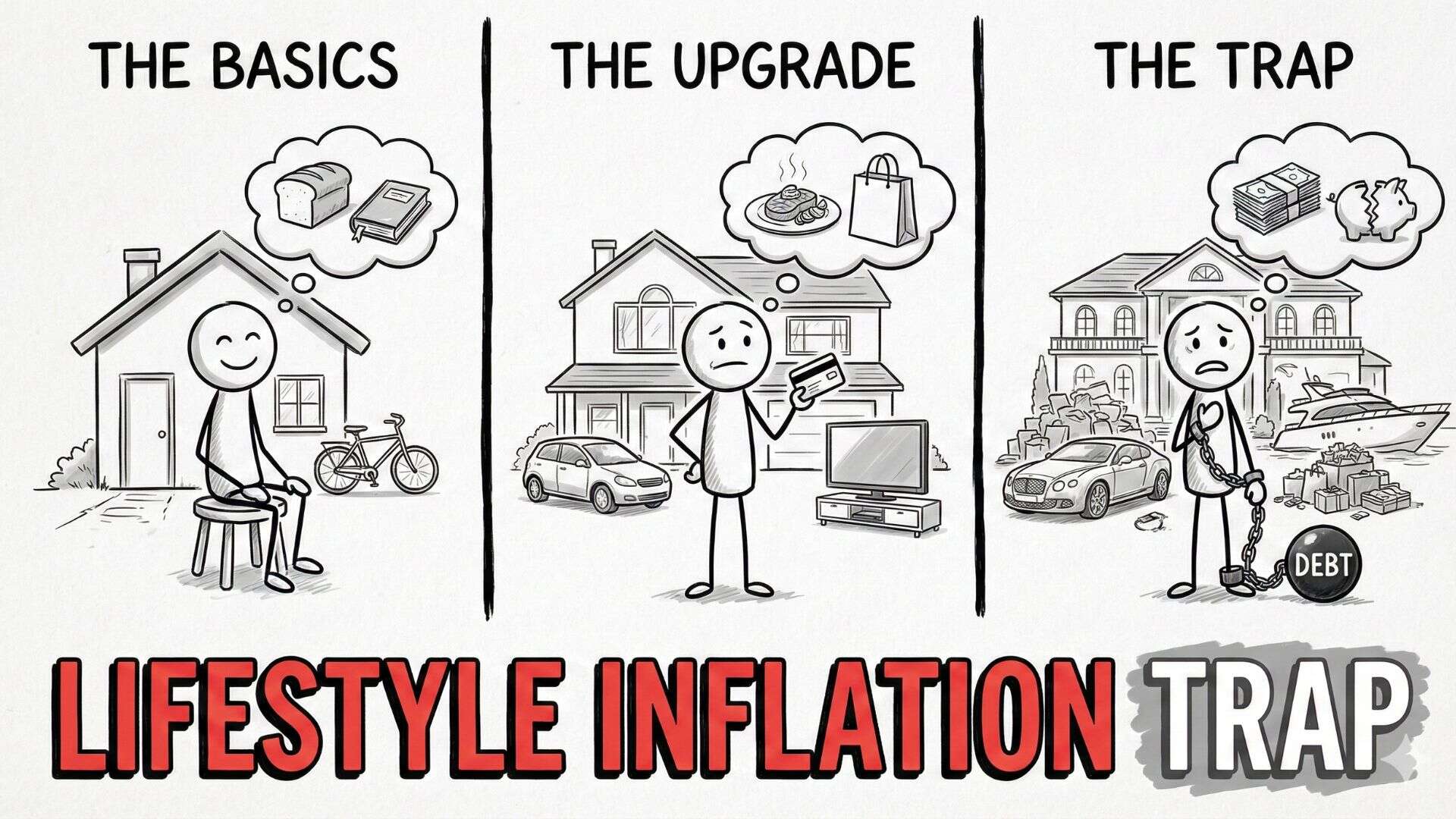

The mechanism begins with a shift in the reference point. When income rises, the decision-maker does not merely experience an increase in purchasing power; they experience a shift in their environment. This environmental change recalibrates the internal set-point for what constitutes a “standard” quality of life. The psychological transition from discretionary to non-discretionary spending is often seamless. For example, a professional who transitions from public transit to a private vehicle, and later to a premium automobile, eventually perceives the premium experience as the baseline. This “necessity creep” ensures that the surplus capital generated by career progression is absorbed into fixed operational costs rather than being diverted to investment.

Intertemporal Choice Dynamics

Lifestyle inflation is a manifestation of hyperbolic discounting—a behavioral bias where individuals choose smaller, immediate rewards over larger, delayed ones. As income grows, the immediate gratification available through upgraded consumption becomes more accessible. The brain’s reward system, calibrated for immediate resource acquisition, struggles to weigh the abstract, future value of a robust investment portfolio against the tangible, immediate utility of a higher-status residence or enhanced leisure experiences.

Read also: Why Income Growth Matters More Than Saving Early

3. Why the Pattern Persists Despite Experience

Lifestyle inflation is rarely a one-time event; it is a structurally recurring pattern. Even individuals who have experienced the “debt traps” of early adulthood often find themselves repeating the cycle as their net worth grows. This persistence is maintained by several reinforcing factors.

Hedonic Adaptation

The primary psychological driver is hedonic adaptation—the observed tendency of humans to return to a relatively stable level of happiness despite major positive or negative life changes. When a higher level of consumption is reached, the initial “utility spike” is temporary. As the new lifestyle becomes the habituated norm, the individual requires a further escalation in consumption to achieve the same level of satisfaction. This creates a treadmill effect where the pursuit of utility necessitates continuous income growth, leaving the net surplus unchanged.

Social Comparison and the “Duesenberry Effect”

The Relative Income Hypothesis, pioneered by James Duesenberry, suggests that an individual’s consumption patterns are more influenced by their relative position in society than by their absolute income. As professionals move into higher-earning circles, their “peer group” shifts. The baseline for social acceptability—the size of the home, the quality of the school, the nature of the vacation—is dictated by the environment. Lifestyle inflation, therefore, is often a defensive mechanism to maintain social cohesion and status within an evolving professional or social hierarchy.

Incentive Asymmetry and Signal Noise

The modern economic environment provides asymmetric feedback. Marketing, credit availability, and social media provide constant, high-fidelity signals encouraging consumption. Conversely, the signals for capital accumulation and the benefits of compounding are quiet, abstract, and often invisible. This “signal noise” makes it far easier for the mind to justify a $2,000 monthly car payment (a visible, social signal) than to internalize the long-term value of $2,000 monthly invested in a diversified fund (an invisible, delayed signal).

Read also: The One Page Financial Plan Summary: STOP OVERTHINKING YOUR MONEY

4. Real-World Consequences: The Erosion of Optionality

The structural impact of lifestyle inflation extends far beyond a simple reduction in savings rates. It fundamentally alters the decision-maker’s relationship with risk and career progression.

Reduced Risk Tolerance and Career Stagnation

A high-fixed-cost lifestyle creates a high “burn rate.” This necessity for high, consistent cash flow effectively reduces an individual’s risk tolerance. When the cost of living consumes 90% of a high salary, the individual cannot afford a period of unemployment or a pay cut to pursue a more lucrative, but riskier, entrepreneurial venture. They become “trapped” in their current income bracket, regardless of their satisfaction with the work. This is the phenomenon of “golden handcuffs,” where lifestyle inflation actively prevents the career pivots that lead to asymmetric long-term gains.

The Systematic Neutralization of Compounding

The mathematical tragedy of lifestyle inflation lies in its impact on the time horizon. Compounding is back-loaded; the most significant gains occur in the final third of the investment period. By inflating the lifestyle in the early and middle years, individuals lose the “base” upon which compounding operates. Even if they begin saving aggressively later in life, they can never recapture the lost time. The cost of a $50,000 lifestyle upgrade at age 30 is not just the $50,000; it is the millions of dollars that capital would have become by age 65.

5. A Core Mental Model: The Ratchet Effect

The Ratchet Effect is a mental model originating from both economics and engineering that describes a process that can easily move in one direction but is difficult or impossible to reverse. In the context of lifestyle inflation, it perfectly illustrates why the problem is so difficult to solve once it has begun.

Just as a physical ratchet allows a gear to turn forward while a pawl prevents it from slipping backward, lifestyle choices frequently have a “one-way” quality. It is psychologically and socially straightforward to move from a modest apartment to a luxury home. However, moving in the opposite direction—downsizing—is met with intense resistance.

Mapping the Ratchet Effect to Behavior

The resistance to “down-ratcheting” is driven by loss aversion. According to prospect theory, the psychological pain of losing a specific level of comfort is significantly greater than the joy experienced when that level was first attained. Once a standard of living is established, any reduction is perceived as a failure or a trauma rather than a strategic reallocation of capital. This creates a structural vulnerability: the individual’s financial plan becomes dependent on their income never decreasing, leaving them exposed to market downturns or industry shifts.

6. Applied Thinking Principles: Decoupling Production from Consumption

Addressing the structural drivers of lifestyle inflation requires a shift from willpower-based discipline to system-level design. The following principles focus on the cognitive frameworks necessary to navigate rising income.

Structural Separation of Cash Flows

One of the most effective methods for mitigating lifestyle inflation is the decoupling of income growth from disposable cash. This involves pre-allocating any increase in earnings to capital formation before it enters the “consumption bucket.” By treating a raise as a non-event for the lifestyle budget, the decision-maker prevents the “baseline shift” from occurring. The goal is to maintain a “standard of living lag,” where the lifestyle remains several years behind the current earning capacity.

Time Horizon Extension

Better thinking requires a deliberate lengthening of the temporal scale used for evaluation. Instead of assessing a purchase based on monthly affordability, it should be assessed based on its “opportunity cost over 20 years.” Shifting the focus from immediate utility to the terminal value of the capital involved helps counteract hyperbolic discounting.

Read also: Unshakeable Summary: How to Thrive When the Market Crashes

The Fixed-Cost Ceiling

A robust strategic principle is the establishment of an absolute ceiling for fixed costs, regardless of income. By defining a maximum “lifestyle footprint,” an individual ensures that as their income grows, their “operating leverage” increases. This growing surplus represents increasing freedom—the ability to walk away from a toxic environment or to invest in high-upside opportunities—rather than increasing maintenance requirements.

7. Common Misunderstandings: Beyond “Discipline”

A common oversimplification is the belief that lifestyle inflation is a simple matter of “spending less” or “having more discipline.” This framing ignores the structural and biological reality of the phenomenon.

The Fallacy of Discipline

Attributing lifestyle inflation purely to a lack of discipline is a fundamental attribution error. In reality, the environment is often the primary driver. An individual working 80 hours a week in a high-stress corporate environment in Manhattan faces different structural pressures to “buy back time” or “signal status” than an individual in a different context. Discipline is a finite resource; expecting it to counteract a 24/7 environment of consumption triggers is often unrealistic.

The “Higher Income” Illusion

Another misunderstanding is the belief that a higher income will eventually outpace the desire for more. Data suggests that without a change in the underlying cognitive framework, consumption simply scales with income. Many high-earning professionals (e.g., surgeons, partners at law firms) report the same level of financial stress as those earning significantly less, precisely because their lifestyle has “ratcheted” to meet their new capacity.

8. Connections to Broader Thinking Frameworks

The psychology of lifestyle inflation is deeply intertwined with several other domains of decision theory and systems thinking.

Systems Thinking: Reinforcing Feedback Loops

In systems thinking, lifestyle inflation can be seen as a reinforcing feedback loop. Higher income leads to higher status requirements, which leads to higher expenses, which requires higher income. Without a “balancing loop”—such as a fixed savings goal or a philosophical commitment to minimalism—the system eventually reaches a point of fragility where any disruption to the input (income) leads to system failure.

Signaling Theory and Evolutionary Psychology

From an evolutionary perspective, humans are wired to signal resource abundance. In the ancestral environment, having excess resources was a signal of fitness and competence. In the modern world, this instinct manifests as conspicuous consumption. Understanding that the urge to “inflate” is an evolutionary vestige can help a decision-maker view the impulse with more objectivity, treating it as a biological signal to be managed rather than an objective necessity.

Opportunity Cost Reasoning

At its core, every dollar spent on a lifestyle upgrade is a dollar that cannot be used to buy “future time.” Individuals who master opportunity cost reasoning understand that they are not just buying a car; they are potentially trading six months of retirement or the ability to leave a job they dislike five years earlier.

9. Conclusion: The Long-Term Perspective

Lifestyle inflation is not an accidental byproduct of success; it is a structural feature of the human experience in a consumption-oriented economy. It is the result of a brain designed for survival in a resource-scarce environment suddenly navigating an environment of relative abundance and intense social signaling.

The persistence of this phenomenon despite experience suggests that the solution is not more information, but a different architecture for decision-making. Success in the long term requires the intellectual humility to admit that one is susceptible to the hedonic treadmill and the ratchet effect. It requires the foresight to build systems that protect capital from the brain’s own desire for immediate utility.

Ultimately, the most valuable asset an individual can possess is not a high-consumption lifestyle, but optionality. By resisting the lock-step escalation of expenses and income, the decision-maker preserves the ability to respond to opportunities and crises with agility. In a world of increasing volatility, the true mark of financial and professional mastery is not how much one spends, but the distance between one’s lifestyle and one’s potential—the margin of freedom that allows for a truly long-term perspective.