In the study of capital allocation and decision theory, time is frequently treated as a secondary coordinate—a mere axis upon which returns are plotted. However, a rigorous analysis of investment behavior suggests that time horizon is the primary architectural variable of the entire system. The duration over which an asset is evaluated and held does not merely influence the magnitude of the outcome; it fundamentally alters the nature of the asset itself, the definition of risk, and the psychological framework of the decision-maker.

The “hidden” nature of the time horizon often leads to profound misalignments between objectives and actions. An identical asset—be it a corporate equity, a real estate parcel, or a debt instrument—can appear as a prudent vehicle for wealth creation to one participant and a hazardous speculative instrument to another, solely based on the window of evaluation. Understanding the causal mechanisms by which time transforms perception and probability is essential for any serious study of long-term reasoning.

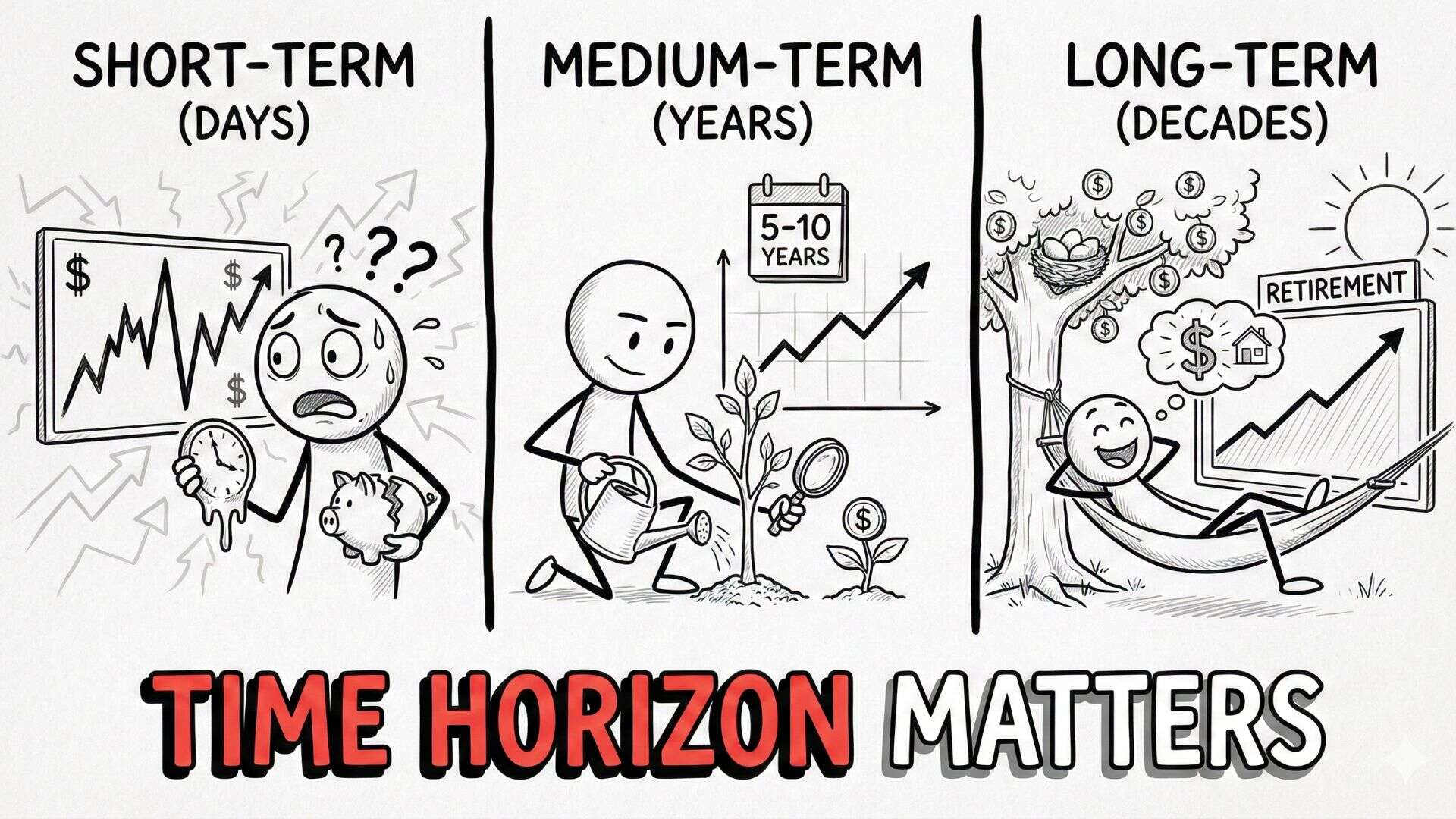

The Psychology of Short-Term vs. Long-Term Thinking

The human cognitive apparatus is evolutionarily optimized for immediate feedback. In a survival context, the ability to react to sudden environmental shifts (noise) was more advantageous than the ability to calculate decade-long trends (signal). When applied to modern financial systems, this biological legacy creates significant distortions.

Immediate Feedback Bias and Emotional Amplification

On short time horizons, the ratio of noise to signal is extremely high. Daily or weekly fluctuations in asset prices are rarely driven by fundamental changes in intrinsic value; rather, they reflect the aggregate emotional state and liquidity needs of market participants. Because the brain processes financial loss in the same neural pathways as physical pain, short-term volatility triggers a state of heightened emotional reactivity.+1

When the evaluation window is narrow, the frequency of feedback increases. Frequent observation of a volatile portfolio subjects the investor to “loss aversion”—the psychological phenomenon where the pain of a loss is felt twice as intensely as the joy of a gain. Consequently, a decision-maker who monitors prices daily is likely to perceive a vastly higher level of risk than one who monitors them annually, even if the underlying asset remains unchanged.

Volatility Misinterpretation

In short time frames, volatility is often conflated with risk. Because price movements are the most visible metric available, they become a proxy for the quality of the investment decision. This leads to a feedback loop where short-term price declines prompt a reassessment of long-term thesis, often resulting in “panic selling” at the exact moment when prospective returns are mathematically highest.

Read also: The Psychology Behind Lifestyle Inflation

Compounding and the Mathematics of Duration

The shift from a short-term to a long-term horizon is not merely a change in perspective; it is a change in the underlying mathematical distribution of outcomes. Time acts as a filter that separates the chaotic influence of randomness from the persistent influence of fundamental growth.

The Dominance of the Mean

Over short durations, investment returns are dominated by the “variance” of the market. The probability of a negative outcome over a single day is nearly 50%, regardless of the asset’s quality. However, as the duration increases, the influence of daily randomness begins to cancel itself out—a phenomenon related to the Law of Large Numbers.

In a long-term horizon, the “mean” or the fundamental earning power of the asset begins to dominate the “noise.” The probability distribution of returns narrows and shifts toward the positive. For example, in many equity markets, the probability of loss decreases significantly as the holding period extends toward ten or twenty years. Time, therefore, acts as a volatility-smoothing mechanism that transforms a high-variance gamble into a lower-variance accumulation of value.+1

Compounding as a Geometric Process

Compounding is fundamentally a geometric progression. In the early stages of an investment, the majority of the total return is driven by the initial principal. As time progresses, however, the returns generated on previous returns begin to eclipse the initial contribution. This non-linear growth requires a specific time threshold to enter the “exponential” phase. A short time horizon truncates this process, effectively ensuring that the decision-maker remains in the linear, low-growth phase of the capital cycle.

Read also: Why Income Growth Matters More Than Saving Early

Risk Perception Changes with Time

The definition of “risk” is not universal; it is duration-dependent. For a market participant with a one-week horizon, risk is price volatility—the possibility that the price will be lower in seven days than it is today. For a participant with a thirty-year horizon, price volatility is irrelevant, and risk is redefined as the permanent impairment of capital or the loss of purchasing power.

Volatility vs. Permanent Impairment

Short-term participants often prioritize “price stability,” yet this stability often masks long-term risks. For instance, holding cash may appear low-risk in a one-year window because the nominal value is stable. However, over a thirty-year window, the certainty of inflation makes cash one of the riskiest assets for preserving purchasing power.

Conversely, productive assets like equities or real estate are highly volatile (risky) in the short term but have historically been more reliable (less risky) at preserving value over decades. When the time horizon is extended, the risk of “missing out” on compounding often becomes greater than the risk of enduring a temporary price decline.

Reframing Uncertainty

Time reframes uncertainty by allowing for the “reversion to the mean.” In the short term, a sector or economy may undergo extreme stress. On a short horizon, the outcome is uncertain and potentially terminal. On a long-term horizon, the decision-maker can account for the cyclical nature of economies, assuming that structural growth will eventually overcome temporary disruptions. This temporal cushion allows for a more analytical, less reactive approach to systemic shocks.

Incentives, Institutions, and Time Horizon Distortion

Despite the mathematical advantages of long-term thinking, institutional and structural forces often coerce market participants into short-term behaviors. These distortions are the result of misaligned incentive structures and the “Principal-Agent” problem.

Quarterly Reporting and Career Risk

Publicly traded corporations and institutional investment funds are often measured on quarterly or annual cycles. For a fund manager, the risk of “underperforming” a benchmark for two consecutive quarters may result in the loss of their job (career risk). Even if the manager believes in the twenty-year prospect of an asset, the institutional incentive to show immediate results forces a shorter-term evaluation. This leads to “window dressing” and herd behavior, where participants buy or sell assets to align with current sentiment rather than long-term value.

Media and Information Velocity

The modern information environment operates on a feedback loop of seconds. Financial media thrives on “breaking news,” which by definition focuses on the immediate and the sensational. This constant stream of data creates an environment of “recency bias,” where the most recent event is given disproportionate weight in the decision-making process. The structural velocity of information makes it difficult for individuals to maintain a ten-year perspective when they are bombarded with ten-second updates.

A Core Mental Model: Compounding as a Time Amplifier

At the heart of duration-based strategy is the mental model of Compounding. While often simplified as “interest on interest,” it is more accurately described as the systematic accumulation of advantages over time.

Exponential vs. Linear Growth

Human intuition is inherently linear. We struggle to visualize a process where $1.00$ becomes $2.00$, $2.00$ becomes $4.00$, and eventually $1,024.00$ becomes $2,048.00$. In a linear system, the change is constant (e.g., adding $10.00$ every year). In a compounding system, the change is proportional to the current state.

This creates a “Time Amplifier” effect. A 1% difference in the rate of return may seem negligible over a one-year period, but over forty years, it can result in a massive divergence in total capital. Because the exponent in the compounding formula is time ($FV = P(1+r)^t$), the duration has a more significant impact on the final outcome than the initial principal or, in many cases, the incremental increase in the rate of return ($r$).

Scaling Decisions

The mental model of compounding suggests that early decisions carry more weight because they have more time to scale. A mistake or a wise allocation made at age 25 has ten times the impact of a similar decision made at age 55. This underscores the causal link between time horizon and the “gravity” of a decision. Long-term reasoning recognizes that the present is the foundation for a vastly scaled future, whereas short-term thinking treats the present as an isolated event.

Read also: How Risk Perception Shapes Financial Outcomes

Applied Thinking Principles (Non-Prescriptive)

Strategic reasoning requires the deliberate alignment of one’s decision-making architecture with their objective time horizon. The following principles serve as a conceptual framework for this alignment:

- Duration Matching: Successful capital allocation requires matching the liquidity of an asset with the time horizon of the need. Using capital required in twelve months to purchase a volatile twenty-year asset is a structural mismatch that exposes the allocator to unnecessary “forced-selling” risk.

- Extension of the Evaluation Window: To counter immediate feedback bias, one might deliberately reduce the frequency of portfolio observation. By moving from daily to annual reviews, the decision-maker naturally filters out noise and focuses on long-term trends.

- Separation of Liquidity and Growth Capital: Maintaining a “liquidity sleeve” (cash or short-term equivalents) allows the remaining “growth capital” to be truly long-term. This structure provides the psychological and financial capacity to endure short-term volatility without jeopardizing the compounding process.

- Reducing Emotional Reactivity through “Pre-Mortems”: Long-term reasoning involves simulating negative short-term scenarios before they occur. By intellectually “accepting” a 30% price decline as a statistical certainty over a twenty-year horizon, the decision-maker reduces the emotional shock and subsequent reactivity when the event eventually manifests.

Common Misunderstandings

The concept of time horizon is often obscured by several common misconceptions that can lead to flawed strategy.

“Long-Term Investing Ignores Risk”

A common critique is that long-term investors are “blind” to current dangers. In reality, a long-term horizon requires a more rigorous assessment of risk, specifically structural and terminal risks. While short-term volatility is ignored, the long-term investor must be hyper-vigilant about anything that could permanently impair the asset’s ability to produce value over decades, such as technological obsolescence or catastrophic governance failure.

“Short-Term Investing is Always Inferior”

Short-term horizons are not inherently “wrong”; they are simply different systems with different rules. High-frequency trading or short-term market making can be highly profitable for those with the technological and informational edge. The error occurs when an individual with a long-term goal uses a short-term methodology, or vice versa.

“Time Horizon Eliminates Uncertainty”

Time does not remove uncertainty; it simply allows it to be managed differently. The “Knightian Uncertainty” (risks that cannot be quantified) still exists. A twenty-year horizon does not guarantee a positive result; it only ensures that the decision-maker is exposed to the fundamental trajectory of the asset rather than its temporary fluctuations.

“Higher Returns Require Constant Action”

There is a pervasive belief that “doing something” is always better than “doing nothing.” However, in a compounding-based system, frequent action often incurs costs—taxes, transaction fees, and the risk of “mistiming” the market—that erode the geometric progression. In many cases, the primary work of the long-term decision-maker is the defense of the original thesis against the impulse to act on short-term noise.

Integration with Broader Decision-Making Frameworks

The study of time horizon intersects with several foundational concepts in systems thinking and behavioral economics:

- Opportunity Cost: Time is the ultimate limited resource. Choosing a short-term horizon for a specific pool of capital has an opportunity cost: the lost compounding that a long-term strategy would have provided.+1

- Systems Thinking (Feedback Loops): Short-term horizons are dominated by “balancing loops” (reversion to the mean), while long-term horizons are dominated by “reinforcing loops” (compounding). Identifying which loop is currently active is a key strategic skill.

- Capital Allocation Theory: Optimal allocation requires viewing capital not as a static pile of money, but as “stored energy” that can be deployed across various durations. The goal is to maximize the “terminal value” of the system by balancing immediate needs with long-term growth.

Conclusion: Duration as Strategic Advantage

In a world increasingly optimized for the immediate, the ability to maintain a long-term time horizon is more than a preference—it is a structural strategic advantage. While most market participants are forced by incentives or psychology to compete in the high-noise environment of the short term, those who can extend their horizon effectively move to a different competitive arena.

Time horizon changes investment decisions by shifting the focus from price to value, from variance to mean, and from reaction to reasoning. It allows for the full realization of the power of compounding and provides the psychological fortitude to withstand the inevitable cycles of the market. Ultimately, capital formation is a function of duration. The most successful participants are not necessarily those who can predict the next move of the market, but those who have the structural patience and intellectual clarity to allow time to do the work for them.

Next Step: Would you like me to draft a comparative table showing how specific “risk factors” (inflation, volatility, liquidity, etc.) change in impact as the time horizon moves from 1 year to 30 years?