The uncomfortable truth: I didn’t lose most of my money from bad investments. I lost it from the decisions I made trying to avoid losses — holding on too long, selling too early, and sitting in cash while the market recovered without me. This is the story of how I discovered loss aversion, what the science says about it, and the exact system I built to stop letting fear run my financial life.

The night I realized fear was making my financial decisions

It was March 2020. The market had just dropped over 30% in a matter of weeks. My portfolio — built carefully over three years — was bleeding red. And I did what any rational, well-read investor would do.

I sold almost everything.

Not because I needed the cash. Not because my thesis had changed. Not because I had analyzed the situation clearly and decided cash was the superior position. I sold because watching the numbers fall was physically painful in a way I had never experienced before — and selling made the pain stop.

For about 48 hours, I felt relief. Then the market began to recover. By August of that same year, the S&P 500 had clawed back nearly all its losses. By the end of 2020, it was up over 16% from where it started the year. The portfolio I had sold in a panic was — had I done absolutely nothing — perfectly fine.

I had bought high, sold low, and missed the recovery. All while reading books about long-term investing and telling myself I was a disciplined, rational investor.

That experience forced me to confront something uncomfortable: I was not making investment decisions based on analysis. I was making them based on fear. And the specific fear driving my behavior had a name — one that psychologists and behavioral economists have studied for decades.

It is called loss aversion. And it is almost certainly affecting your financial decisions too.

Read also: First Principles Thinking: Stop Following Advice, Start Reasoning

What loss aversion actually is — and the science behind it

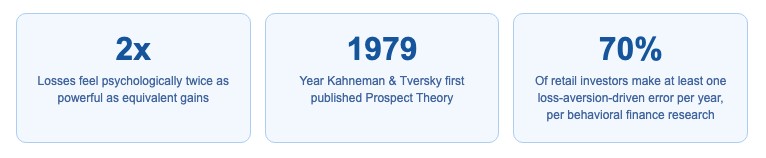

Loss aversion is not a personality flaw. It is a deeply wired feature of human cognition, first formally identified and studied by psychologists Daniel Kahneman and Amos Tversky in the late 1970s as part of their groundbreaking work on Prospect Theory — research that eventually earned Kahneman the Nobel Prize in Economics in 2002.

The core finding is deceptively simple:

“Losses loom larger than gains. The pain of losing something is psychologically about twice as powerful as the pleasure of gaining the same thing.”— Daniel Kahneman, Thinking, Fast and Slow

In concrete terms: losing $1,000 feels roughly as painful as gaining $2,000 feels pleasurable. The emotional weight of a loss is approximately twice the emotional weight of an equivalent gain. The numbers are the same. The psychological experience is not.

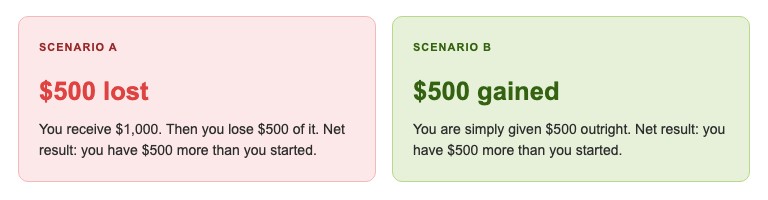

Kahneman and Tversky demonstrated this through a simple thought experiment that I find extraordinarily clarifying. Consider these two scenarios:

The rational outcome is identical. But almost universally, Scenario A feels worse — because the act of losing registers as a distinct, painful event in the brain, even when the final position is the same.

This is not irrationality. It is evolutionary. For most of human history, losses were existential. Losing food, shelter, or a member of the tribe could mean death. Gains, while welcome, rarely offered the same survival urgency. The brain learned to weight losses heavily — and that wiring hasn’t caught up with the reality of modern financial markets.

Read also: The Day I Walked Away from Three Years of Work — And Why It Was the Best Decision I Ever Made

How loss aversion shows up in your portfolio right now

The March 2020 panic sell was my most dramatic moment of loss aversion. But once I understood the bias, I realized it had been quietly shaping my financial behavior for years in subtler ways.

The disposition effect

This is one of the most well-documented manifestations of loss aversion in investing. It describes our tendency to sell winning investments too early — to “lock in” gains — and hold losing investments too long — to avoid realizing a loss.

I did this constantly. I would sell a stock the moment it was up 15–20%, terrified the gains would evaporate. Meanwhile, I would hold positions that were down 30–40% for months, telling myself they would “come back,” when the truth was I simply could not face the emotional weight of booking a loss.

The result: I systematically exited my winners early and rode my losers all the way down.

Cash hoarding during volatility

After bad market periods, I developed a habit of sitting in cash far longer than any rational analysis would support. The logic felt sound: “I’ll wait until things stabilize.” But “stabilized” never felt safe enough, because the fear of losing what little I had left was more powerful than the opportunity cost of missing the recovery.

In behavioral economics, this pattern is sometimes called the break-even effect — after experiencing losses, people become unusually risk-averse, paradoxically at exactly the moment when risk-taking offers the best expected returns.

Refusing to rebalance

Proper portfolio management requires periodically selling outperformers to buy underperformers — rebalancing back to your target allocation. Intellectually, I knew this. But every time I tried to rebalance, I felt the pull of two loss-aversion traps simultaneously: the pain of selling something that was working, and the pain of buying more of something that was down.

So I didn’t rebalance. My portfolio drifted. My risk profile changed without my choosing it. And it happened entirely because of a bias I didn’t consciously register.

The pattern to watch for in yourself

You check your portfolio more often when markets are falling than when they’re rising.

You feel the urge to “do something” when you see red — even when doing nothing is the rational move.

You have held a losing position long past the point where your original thesis was invalidated.

If any of these feel familiar, loss aversion is already in the driver’s seat.

Read also: Cracking the Sales Management Code for Predictable Revenue

The real cost: what loss aversion has actually cost me

For a long time, I thought of my emotional investment mistakes as embarrassing but ultimately minor — the kind of behavioral quirks that smart people laugh about at dinner and then continue repeating.

Then I actually ran the numbers.

Between 2018 and 2023, I tracked every investment decision I could identify as being primarily emotion-driven rather than analysis-driven. The category included: premature sales driven by anxiety, cash-hoarding periods where I stayed out of the market, and positions I held too long out of refusal to accept a loss.

The opportunity cost — the difference between what my portfolio actually returned versus what it would have returned on a basic, emotionless index strategy — was significant enough that I am not going to share the exact number here. What I will say is that it was enough to materially change what I now think about behavioral discipline as a financial skill.

Academic research supports this experience. Studies on retail investor behavior consistently find that individual investors underperform simple index funds by 1.5–3% per year on average — and the primary driver of that gap is not poor stock selection. It is poor behavior. Selling when fear peaks. Buying when enthusiasm peaks. The same cycle, repeated across millions of portfolios.

Loss aversion is not a minor inconvenience. Over a 30-year investing horizon, a consistent 2% behavioral drag compounds into an enormous real-world wealth gap. This is not a theoretical concern. It is a calculable, quantifiable cost of letting an ancient survival instinct run a modern financial life.

Why this bias is so hard to overcome

If you’ve read this far, you might be thinking: “Okay, I understand the bias now. I’ll just ignore my emotional reactions when I’m investing.” I thought the same thing. It doesn’t work — and understanding why it doesn’t work is essential to building a system that actually does.

Knowledge does not override the wiring

Kahneman himself — the man who spent his career studying cognitive biases — has said that knowing about a bias does not make you immune to it. The emotional reaction is generated by the older, faster parts of the brain (what Kahneman calls System 1 thinking) before the analytical, slower parts (System 2) even have a chance to weigh in.

By the time you’re telling yourself “I shouldn’t panic sell,” the emotional signal has already been firing for several seconds. In a volatile market, that is more than enough time to click “sell” before logic catches up.

Loss aversion is amplified by information density

The more frequently you check your portfolio, the more loss aversion episodes you experience — and the more frequently they drive bad decisions. Research by Richard Thaler (another Nobel laureate in behavioral economics) found that investors who checked their portfolios daily made significantly worse decisions than those who checked quarterly, even when holding identical assets.

This is why the solution is not willpower. The solution is architecture.

The key insight

You cannot willpower your way out of loss aversion any more than you can willpower your way out of hunger. The emotion is real, valid, and not a character flaw.

What you can do is design your environment and decision-making process so that the emotion cannot act unilaterally. The goal is not to feel less — it is to create enough friction between the feeling and the action that reason has time to participate.

Read also: What “Mastering Private Equity” Taught Me About How Capital Really Moves

The 5-step framework I use to make fear-free investment decisions

After the 2020 experience, I spent several months rebuilding my investment process from the ground up — specifically designed to neutralize loss aversion at the structural level. Here is exactly what I did.

- Write an investment thesis before buying anythingBefore purchasing any position, I write a one-paragraph document stating: what I believe, why I believe it, what conditions would prove me wrong, and what conditions would confirm I’m right. When the market moves against me, I return to this document. The question is not “does this feel bad?” — it is “has my thesis changed?” If not, the feeling is noise.

- Set a pre-committed decision rule for exitsI decide in advance — before the emotional state occurs — under what conditions I will sell. A specific price level. A fundamental change in the business. A time horizon expiry. This converts exit decisions from emotional reactions into mechanical executions of a pre-set plan, made when I was calm and rational.

- Limit portfolio check frequency by designI removed all investment apps from my phone’s home screen. I set a calendar reminder to review my portfolio on the first Sunday of each month — and I do not open brokerage accounts outside of that scheduled review. This is not discipline. It is architecture. Fewer exposure events means fewer opportunities for loss aversion to trigger a decision.

- Implement a 72-hour rule for any unplanned tradeIf I feel a strong urge to buy or sell something outside of my scheduled review — which is almost always driven by fear or excitement — I write down the action I want to take and wait 72 hours. In my experience, roughly 80% of those impulses disappear entirely within three days. The 20% that survive are worth examining.

- Reframe “loss” as “cost of participation”Volatility is not a malfunction of markets. It is the price of long-term returns. I now think of portfolio drawdowns the way I think of turbulence on a flight — uncomfortable, expected, and not a signal that the plane is going down. Reframing the experience does not eliminate the discomfort, but it changes the action I associate with it.

My personal investment rules that neutralize the bias

Beyond the framework, I’ve developed a set of rules I follow consistently. These aren’t theoretical — they are the direct result of painful, expensive experiments in what happens when I don’t follow them.

Rules I now follow without exception

- Never make an investment decision during a market decline. Decisions made in red-screen environments are almost always loss-aversion driven. I wait for green days or for scheduled review periods before making structural changes.

- Never check my portfolio more than once per week. The more I look, the more the volatility feels like a crisis. At a monthly check frequency, the same volatility feels unremarkable.

- Never calculate unrealized losses in dollar terms. I track my portfolio in percentage terms only. “$47,000 down” triggers a visceral response that “14% below peak” does not — even though they represent the same reality.

- Always have a written thesis before a position. If I can’t articulate why I own something in one paragraph, I don’t buy it. If my thesis changes, I exit — regardless of current price.

- Automate the rational decisions. Dollar-cost averaging into index funds is now automatic. The money moves on the first of each month whether I feel good about markets or not. Automation removes the decision point — and therefore removes the opportunity for loss aversion to intervene.

Read also: How I Upgraded My Thinking with Adler’s 4 Levels of Reading

Conclusion: the goal isn’t to eliminate fear — it’s to stop obeying it

I want to be clear about something: I still feel fear when markets drop. I still feel the pull to check my portfolio obsessively during volatile periods. I still notice the discomfort of watching a position move against me.

The difference is that I have stopped treating those feelings as signals to act.

Loss aversion is not a bug you can patch out of the human operating system. It is a feature — one that served our ancestors well and continues to serve us in domains where physical and social losses carry immediate consequences. The problem is that financial markets are a domain where our instincts are almost perfectly calibrated to produce the wrong behavior at the wrong time.

The market falls. Fear spikes. The instinct says sell and preserve what remains. The rational response is frequently the opposite — hold, or even buy more.

Every time I have followed the instinct, I have regretted it. Every time I have followed the system, I have not.

The goal of behavioral finance literacy — understanding biases like loss aversion — is not to become emotionless. It is to understand your emotional wiring well enough to build systems that protect you from it when it matters most.

Start with one thing. Pick one rule from the framework above and implement it this week. Not when you feel ready. Not after the next market correction. Now — while you’re calm and rational and the stakes feel low.

Because the time to build a firebreak is never when the forest is already burning.