The embarrassing gap I didn’t know I had: For years I invested in individual companies while being unable to properly read their financial statements. I understood the concepts in general terms — revenue, profit, debt — but I had never sat down with an actual annual report and worked through it systematically. The day I finally did, I found accounting realities in companies I owned that I had completely missed. This article is the guide I wish I had before I started investing in individual stocks.

Disclaimer: This article is educational only and does not constitute financial or investment advice. Always consult a qualified financial professional before making investment decisions. See our full disclaimer.

Why financial literacy matters even if you don’t pick stocks

Before I explain the mechanics, I want to address the most common objection: “I invest in index funds — why do I need to read financial statements?”

The answer is that financial statement literacy matters beyond stock picking. If you are self-employed or run a business, understanding income statements and cash flow is essential for making operational decisions. If you are evaluating a partnership, a client’s creditworthiness, or a vendor’s stability, financial statement literacy tells you things that no presentation or sales conversation does. If you ever negotiate compensation with equity components, you need to understand the financial health of the company offering you equity.

And if you do invest in individual companies — as I did, without this literacy — you are essentially navigating without a map. The numbers are available to everyone. Not being able to read them is a choice that puts you at a consistent disadvantage relative to people who can.

Read also: How I Finally Overcame Procrastination — After Years of Failing To

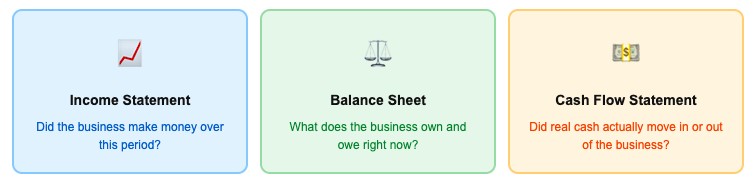

The three financial statements and what each answers

These three documents together form the complete financial picture of any business. Each answers a different question, operates on different time horizons, and uses different accounting conventions. Understanding what each one does — and what it doesn’t — is the foundation of financial literacy.

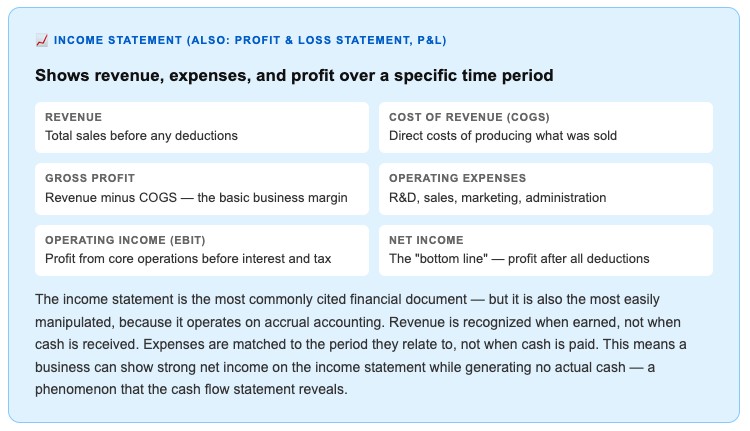

The Income Statement — what the business earned

What I look for first: Revenue growth trend (is the business growing?), gross margin trend (is the core business model becoming more or less efficient?), and the gap between operating income and net income (large discrepancies often indicate unusual items worth understanding).

Read also: Why Incompetence Feels Like Confidence — and What to Do About It

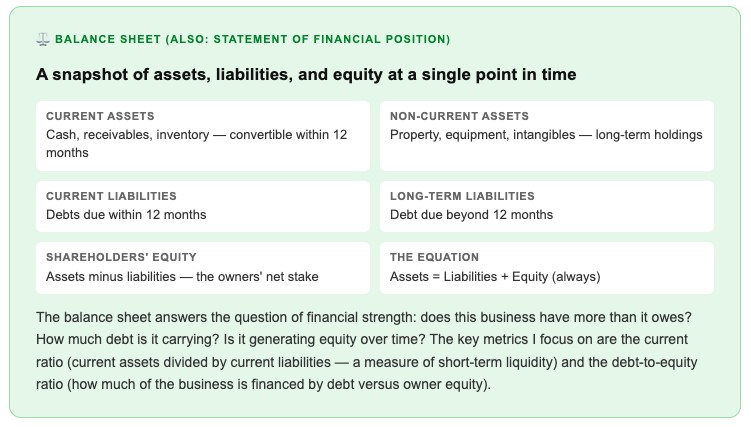

The Balance Sheet — what the business owns and owes

What I look for: Growing goodwill and intangible assets that can indicate acquisition-driven growth that hasn’t been tested, rising short-term debt that could signal liquidity pressure, and the trend in shareholders’ equity over multiple years as a measure of value accumulation.

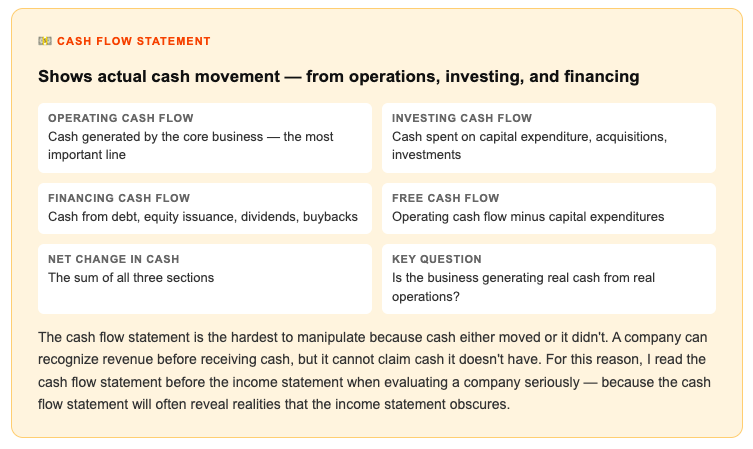

The Cash Flow Statement — the most honest of the three

“Revenue is vanity, profit is sanity, but cash flow is reality.”— Common accounting maxim

What I look for first: The relationship between operating cash flow and net income. If net income is consistently much higher than operating cash flow, the company is recognizing revenue faster than it’s collecting cash — which is worth understanding and potentially concerning. Free cash flow (operating cash flow minus capital expenditures) is the number I consider most important for understanding genuine business quality.

Read also: The Hidden Price Tag on Every Decision You Make

How the three statements connect

The three statements are not independent documents — they form a coherent system where each connects to the others through specific line items.

Net income from the income statement flows into the equity section of the balance sheet (increasing retained earnings) and is also the starting point for the cash flow statement (which then adjusts net income for non-cash items to arrive at operating cash flow). Changes in the balance sheet’s working capital accounts — receivables, inventory, payables — appear as adjustments in the operating section of the cash flow statement.

Practically: a company that is growing revenue and net income but whose receivables are growing faster than revenue may be recognizing revenue that customers haven’t paid yet. This shows as strong income statement performance and concerning cash flow performance simultaneously. Seeing both statements together reveals what either one alone would obscure.

Red flags I now look for in every financial statement

My practical reading order and process

- Start with the MD&A (Management Discussion and Analysis) In an annual report, the MD&A section precedes the financial statements and contains management’s own explanation of the results. Read this first to understand the narrative before the numbers. Then read the numbers critically against that narrative — looking for discrepancies between what management emphasizes and what the statements show.

- Read the cash flow statement first among the three Start with the cash flow statement’s operating section. Is the business generating real cash from operations? How does operating cash flow compare to net income? This establishes the baseline reality before the income statement’s accrual-based picture.

- Read the income statement with the cash flow statement in mind Now look at the income statement. How does the revenue trajectory compare to operating cash flow? Are there large non-cash charges or credits affecting net income? Is operating income a reliable representation of business performance?

- Check the balance sheet for financial strength and trend Assess liquidity (current ratio), debt load (debt-to-equity), and the trend in equity over multiple years. Is the business generating value for shareholders over time? Is the debt load sustainable given the cash flow generation?

- Always read at least three to five years of data — never just one A single year’s financial statements can tell you what happened. Multiple years tell you the trend — whether margins are expanding or compressing, whether cash generation is improving or deteriorating, whether management’s promises in previous MD&As turned into results. One year is a snapshot; multiple years are the story.

Conclusion: the numbers tell a story — you need to read the whole book

Financial statement literacy is not reserved for accountants and professional analysts. It is a practical skill that anyone who invests, runs a business, or makes significant financial decisions with or about organizations should develop.

The mechanics are learnable in a few hours of focused study. The judgment — knowing which numbers to focus on for a given type of business, understanding the difference between genuine financial strength and accounting creativity, recognizing the patterns that indicate opportunity or risk — takes longer to develop and requires reading many statements across many companies over time.

Where to start — this week

Pick a publicly traded company whose products or services you use regularly and understand well. Download their most recent annual report from their investor relations page. Find the three financial statements. Read the cash flow statement first.

Ask one question: is this business generating more real cash from operations than it did three years ago? Follow that question into the income statement and balance sheet. You’ll learn more from one focused reading of a real company than from any number of explanatory articles — including this one.