Risk is not a single thing: For most of my adult life, I thought about risk as a dial — more risk, more potential reward, less risk, less. That model is both common and wrong. Risk is actually a relationship between probability, magnitude, reversibility, and asymmetry. Once I understood those four dimensions, my entire approach to decisions changed — in investing, in career, and in how I think about what is actually dangerous.

The risk mental model most people use — and why it fails

The most common mental model of risk treats it as a single-dimensional spectrum: from safe to risky. More risk means more potential reward and more potential loss. Less risk means less of both. This model is intuitive, simple, and significantly wrong.

The problems with the dial model are multiple. It conflates very different kinds of risk — a small probability of enormous loss and a high probability of small loss look the same on the dial, even though they require completely different responses. It ignores reversibility — whether a bad outcome is recoverable or permanent. And it treats “less risk” as always better when the real goal is not risk minimization but intelligent risk selection.

The result of operating from the dial model: people avoid low-stakes, highly reversible risks that offer genuine upside, while accepting high-stakes, irreversible risks without fully recognizing them as such. The person who won’t try a new career path because it “feels risky” may simultaneously have their retirement savings in a single asset class — a much more dangerous risk configuration that feels safe because it’s familiar.

Read also: The Exact Formula for Wealth Creation

The four dimensions of risk that actually matter

1. Probability

How likely is the bad outcome? This is the dimension most people consider — but it is only one of four, and on its own, it is insufficient. A 90% probability of a small loss is a very different situation from a 90% probability of a catastrophic one. Probability must be combined with magnitude to mean anything.

2. Magnitude

How bad is the bad outcome if it occurs? A 50% chance of losing $100 and a 50% chance of losing your entire financial net worth are not equivalent risks even though the probability is identical. Magnitude is what determines whether a bad outcome is a setback or a catastrophe — and catastrophe is categorically different in ways that probability alone doesn’t capture.

3. Reversibility

Can you recover? This is perhaps the most underweighted dimension of risk. A bad outcome that is reversible — a failed project, a poor investment in a small position, a career move that doesn’t work out — is fundamentally different from one that is permanent. Reversible bad outcomes are learning opportunities. Irreversible bad outcomes are terminal in a way that closes off the future entirely.

This is why Nassim Taleb’s primary rule of risk management is essentially: never risk ruin. Not because you should avoid large bets, but because a zero — bankruptcy, catastrophic health failure, permanent reputational damage — eliminates all future optionality in a way that no expected value calculation fully captures.

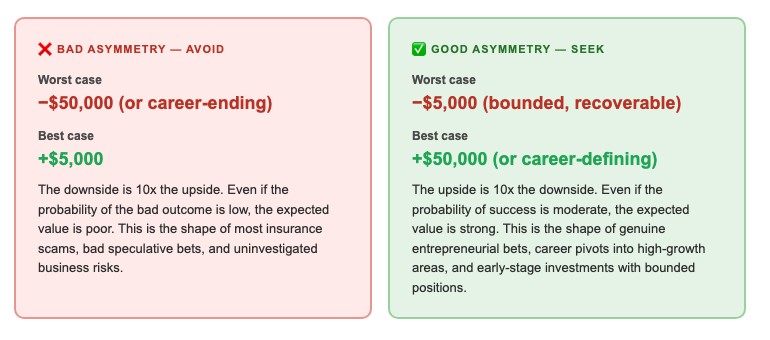

4. Asymmetry

What is the ratio of best-case outcome to worst-case outcome? This is the dimension that separates intelligent risk-taking from gambling. The goal is not to take risks where the downside and upside are equivalent — it is to find situations where the upside is significantly larger than the downside. That asymmetry — not a vague tolerance for risk — is the foundation of intelligent risk-taking.

“If you’re going to be wrong, make sure you’re wrong in a way that doesn’t kill you. Protect the downside and let the upside take care of itself.”— Nassim Nicholas Taleb, Antifragile

Asymmetric risk: the concept that changed how I invest and decide

The most valuable single concept in risk thinking — the one that has changed my behavior more than any other — is asymmetric risk: situations where the potential upside dramatically exceeds the potential downside.

Once you start looking for asymmetry explicitly, you find it everywhere — and you find its inverse everywhere too. Most people accept bad asymmetry without recognizing it, and avoid good asymmetry because the downside feels uncomfortable even when it’s bounded and recoverable.

Read also: How Better Thinking Leads to Better Outcomes

Tail risk: the danger of ignoring low-probability catastrophe

Tail risks are low-probability, high-magnitude events — things that are unlikely to happen but, when they do, produce catastrophic outcomes. They live in the tails of the probability distribution, which is why they’re called tail risks. And they are systematically underweighted in most people’s risk thinking.

The reason for this underweighting is partly psychological — we weight recent and vivid experiences more heavily than statistical probabilities — and partly structural: financial models that assume normal distributions radically underestimate the probability of extreme events. The 2008 financial crisis, the COVID-19 pandemic, and multiple other “once in a generation” events happened within a single generation.

The practical implication for risk management is that you should treat tail risks categorically differently from regular risks. Regular risks can be evaluated by expected value — probability times magnitude. Tail risks require a separate framework: the question is not “what is the expected value?” but “can I survive the worst-case outcome?” If the answer is no, the position is too large regardless of the expected value calculation.

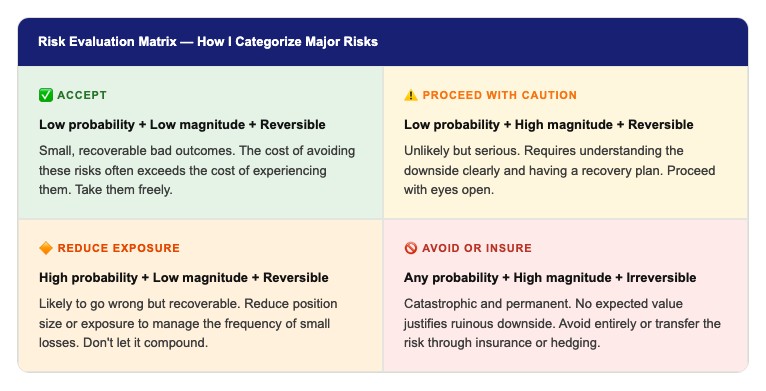

A practical risk matrix I use for major decisions

How I apply this to my own financial and career decisions

The framework above is not abstract for me. Here is how I use it in practice across the two domains where I find it most valuable.

In investing

My primary rule is position sizing: no single position large enough to be catastrophic if it goes to zero. This isn’t about being conservative — I hold concentrated positions and take genuine risks. But I size them so that the worst-case outcome on any individual position is recoverable. I accept the asymmetry that this produces: I cap my upside on any single bet in exchange for capping my downside at something survivable.

I also think about tail risk explicitly. My portfolio maintains enough liquidity and diversification that a single catastrophic event in one area doesn’t eliminate the whole. I pay for this margin of safety through somewhat lower expected returns in normal times. I consider that a reasonable price for the option value of surviving a tail event.

In career decisions

Career risks tend to be more reversible than people treat them. A failed startup that costs two years of salary is not a catastrophe for most people — it is a recoverable setback with significant learning embedded in it. Yet many people treat the risk of career change as if it were in the “avoid” category of my matrix, when it is often closer to “proceed with caution.”

I evaluate career risks on reversibility more than on probability. Can I return to something like my current position if the new path doesn’t work? If yes, the downside is bounded and the risk profile is much more favorable than the emotional experience of considering the change suggests.

Read also: A Deep Anthropological Review of Simon Sinek’s Leaders Eat Last

My personal risk rules — built from expensive mistakes

- Never risk ruin — no bet is worth zero Whatever position I take — financial, career, or otherwise — I size it so that the complete failure of that position doesn’t eliminate my ability to participate in the next opportunity. Ruin is the one outcome from which there is no recovery and no learning.

- Evaluate reversibility before probability Before asking “how likely is this to go wrong?” I ask “how bad is it if it does go wrong, and can I recover?” Reversible risks with uncertain probabilities are almost always worth taking. Irreversible risks require near-certainty of outcome before accepting them.

- Look for asymmetry — and avoid its inverse Before any significant commitment, I map the best-case and worst-case outcomes explicitly. If the ratio is unfavorable — if I can lose significantly more than I can gain — I don’t proceed regardless of how compelling the opportunity seems. Emotion makes bad asymmetry feel acceptable. The explicit mapping counteracts that.

- Pay for protection against tail risks — it is always worth it Insurance, diversification, liquidity reserves, and other forms of tail-risk protection cost money in expected-value terms. They are still worth having because the tail events they protect against, when they occur, are catastrophic in ways that expected value calculations don’t capture.

- Distinguish between risk and uncertainty — and act differently in each Risk is measurable — you can estimate probabilities. Uncertainty is not — you cannot. Many of the most important decisions involve uncertainty, not risk. In uncertainty, reduce position size, increase optionality, and avoid irreversibility. In risk, calculate expected value and act on it. The mistake is treating uncertainty as if it were risk — applying quantitative tools to situations where the inputs are fundamentally unknowable.

Conclusion: the goal isn’t to avoid risk — it’s to take the right kind

The best risk-takers I have studied are not people who tolerate more risk on the dial model. They are people who think more precisely about what kind of risk they are taking — its probability, magnitude, reversibility, and asymmetry — and who take risks that score well on those four dimensions while avoiding risks that score poorly.

The person who takes a large, bounded, reversible career risk with significant upside is not being reckless. They are being intelligent. The person who keeps 90% of their net worth in a single asset class because it’s “safe and familiar” is not being conservative. They are accepting significant tail risk without recognizing it as such.

The framework does not make risk disappear. It makes it more visible — and once you can see the four dimensions clearly, you can make better choices about which risks are worth taking and which are not. That clarity is the beginning of intelligent risk management.

Start here — one question per dimension

For any significant risk you’re currently carrying or considering, ask four questions: How probable is the bad outcome? How large is the bad outcome? Can I recover from it? And is the upside meaningfully larger than the downside?

Most risks that feel uncomfortable become clear through that four-question frame. And several risks that feel comfortable reveal themselves to be the kind worth addressing.