Debt Snowball vs Avalanche: The Best Method Is the One You’ll Actually Finish

One saves you the most money. The other keeps you going. Here’s the honest debt snowball vs avalanche comparison — and why finishing matters more than being mathematically perfect.

If you’ve started reading about paying off debt, you’ve hit the two big names: the snowball and the avalanche. And you’ve probably also hit the slightly heated debates about which is “correct,” usually with someone insisting the maths proves their side. I want to give you a calmer, more honest take, because the truth is gentler than the debates suggest. Both debt snowball vs avalanche methods work. They just optimize for different things — and the right one for you depends on you, not on a formula. Here’s the plain version.

First, something more important than the method

Before any strategy talk, one thing needs saying, because if you’re carrying debt you may need to hear it: debt is a situation, not a character flaw. People end up in debt for a thousand reasons — medical bills, job loss, a hard season, a genuine mistake, or just life being expensive. Carrying debt says nothing about your worth as a person. The heaviness of debt is often as much about the shame and the not-knowing as the money itself.

So approach this without self-punishment. You’re not fixing a personal failing; you’re solving a situation, one payment at a time. That mindset matters, because shame makes people avoid looking at their debt, and avoidance is the real enemy. Facing it, gently and practically, is the whole game.

The avalanche: mathematically cheapest

The avalanche method says: pay minimums on everything, then throw every extra dollar at the debt with the highest interest rate first. Once that’s gone, roll everything onto the next-highest rate, and so on.

The logic is airtight. Your highest-interest debt is the one costing you the most money every month, so killing it first saves you the most in interest and gets you debt-free fastest (and cheapest) in pure numbers. If you’re driven by efficiency and you’ll stick to a plan based on maths alone, the avalanche is the mathematically optimal choice. Every dollar goes where it does the most damage to your total cost.

The snowball: built for momentum

The snowball method says: pay minimums on everything, then throw every extra dollar at the debt with the smallest balance first — regardless of interest rate. Once that’s paid off, roll its payment onto the next-smallest, and so on. The payments “snowball” as each debt falls.

The logic here is psychological, not mathematical. By targeting the smallest balance, you get your first debt paid off quickly — an early, motivating win. That win produces momentum, a sense of progress, and the emotional fuel to keep going. You feel the plan working, fast, which makes you more likely to stick with it. The snowball costs a little more in interest than the avalanche, but it’s engineered to keep you in the game.

Why “just do the maths” misses the point

Here’s where the debates go wrong. The avalanche is mathematically superior — this is simply true. But personal finance isn’t a maths problem; it’s a human problem. And the best debt payoff method isn’t the one that’s optimal on a spreadsheet. It’s the one you’ll actually stick with to the end.

A snowball you complete beats an avalanche you abandon three months in. If quick wins keep you motivated and the avalanche’s slow start would make you give up, then the snowball — despite costing marginally more in interest — is genuinely the better choice for you, because finishing is what matters. The small extra interest is a tiny price for dramatically higher odds of actually becoming debt-free.

This is why the honest answer to “which method?” is: the one you’ll finish. For some people that’s the avalanche (they’re motivated by knowing they’re being optimal). For others it’s the snowball (they need the wins). Both are right, for different people. Neither is a moral choice.

How to pick yours

A simple way to decide: be honest about what keeps you going. Do you find it satisfying to know you’re saving the maximum, even if the first payoff takes a while? Avalanche. Do you need to see a debt fully gone, soon, to believe the plan is working? Snowball. There’s no wrong answer, and you can even switch if one isn’t working — the point is momentum toward zero, however you get it.

It helps enormously to see both orders laid out side by side with your actual debts, so you can make an informed choice rather than an abstract one. Seeing “here’s the snowball order, here’s the avalanche order, here’s roughly what each costs” turns a heated internet debate into a simple personal decision.

The thing that beats both methods

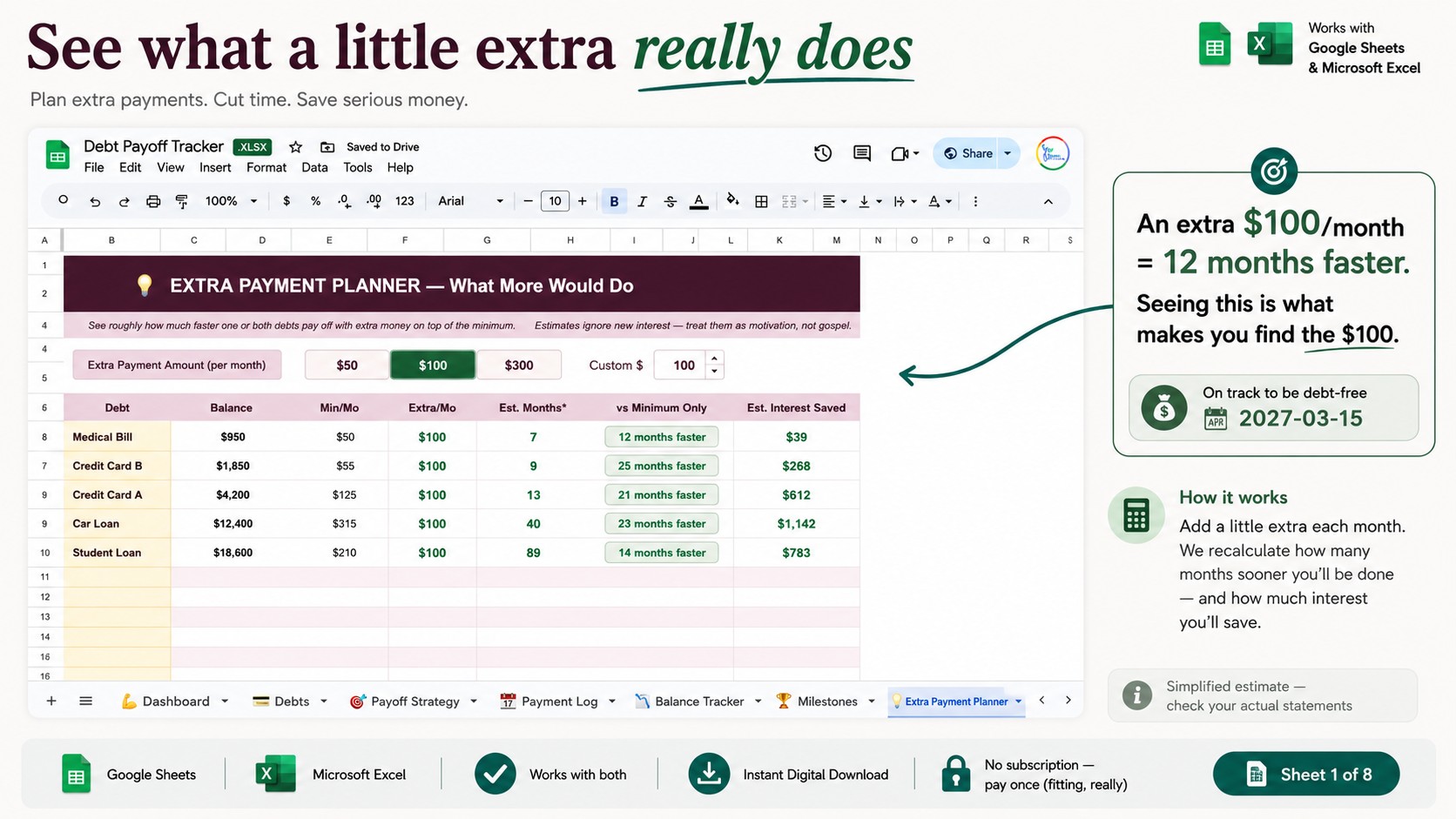

Whichever you pick, one factor dwarfs the snowball-vs-avalanche difference: paying extra. Any additional amount you can put toward your debt, beyond the minimums, accelerates your payoff far more dramatically than the choice of method does. The methods decide the order; the extra payments decide the speed. Don’t let the method debate distract you from the thing that matters most — consistently putting whatever extra you can toward getting free.

An important, caring note

Please hear this clearly: this is a general explanation of two common approaches — not financial, debt, or credit advice, and payoff estimates are simplified (they don’t fully account for compounding, fees, or rate changes, so always check your actual statements). Most importantly: if you are struggling with debt, you don’t have to face it alone. A non-profit credit counselling service can help, often for free, and reaching out to one is a sign of strength, not failure. There is real, judgment-free help available.

If you want both methods calculated for you

I built a debt payoff tracker in Google Sheets that calculates both the snowball and avalanche orders automatically from your actual debts, so you can see them side by side, watch your total fall month by month, and see how much faster extra payments get you there:

👉 Debt Payoff Tracker for Google Sheets & Excel

Whether you use a tool or a notebook, pick the method you’ll actually stick with, and start. The snowball-vs-avalanche debate matters far less than showing up, month after month, and chipping away. Debt is a situation, not a character flaw — and every payment is a brick out of the wall. You can do this.

This is a general explanation and organizing tool — not financial, debt or credit advice; estimates are simplified, so check your actual statements. If you’re struggling, a non-profit credit counselling service can help, often for free. Which method are you using, and how’s it going? Share it in the comments — this community roots for each other.