The Extra $100 That Saves You a Year

A modest extra payment does something surprisingly powerful — because every extra dollar goes straight at the principal. Here’s why extra debt payments are the real accelerator.

When you’re paying off debt, the minimum payment feels like the deal you’re stuck with — the amount you owe each month, the pace you’re locked into. But the minimum payment is quietly working against you, and the single most powerful thing you can do to get free faster is deceptively small: pay a little extra. Not a lot. Even a modest amount, consistently, changes the picture dramatically. Understanding why extra debt payments are so powerful is one of the most motivating things you can learn when you’re trying to become debt-free. Here’s the mechanism, in plain terms.

Why the minimum payment keeps you stuck

Here’s what’s happening with a minimum payment that most people don’t see. A big chunk of it goes to interest, not to your actual balance. Especially early on, especially with high-interest debt like credit cards, your minimum payment barely touches the principal — you pay, and yet the balance seems to crawl down at a heartbreaking pace, because interest is eating most of your payment.

This is by design. Minimum payments are calculated to keep you paying for a very long time, maximizing the interest collected. It’s not your imagination that the balance moves slowly on minimums — it genuinely does, because you’re mostly paying rent on the money rather than giving it back. That’s the trap: minimums keep you technically “paying it off” while barely making progress.

Why extra payments hit so much harder

Here’s the beautiful part. When you pay extra — beyond the minimum — that entire extra amount typically goes straight at the principal. It skips the interest portion (which the minimum already covered) and directly reduces what you owe.

That has a compounding effect in your favour. A lower principal means less interest charged next month. Less interest means more of your next payment goes to principal too. Which lowers the balance further, which lowers interest again. The extra payment doesn’t just reduce your debt by that amount — it accelerates the entire payoff, because it breaks the interest cycle that was holding you back. A dollar of extra payment does far more work than a dollar of minimum payment, because it’s attacking the root instead of the symptom.

This is why a surprisingly small extra amount can take months, sometimes a year or more, off your payoff timeline, and save a real chunk of interest. The effect is much bigger than the modest size of the payment would suggest — and it grows the earlier in the debt you start doing it.

Seeing “12 months faster” is what makes it real

Numbers on a page don’t motivate people. Concrete, personal projections do. There’s a huge difference between the vague idea “extra payments help” and the specific, personal fact “an extra $100 a month gets me debt-free 14 months sooner and saves me a significant amount in interest.”

That second version is motivating in a way the first isn’t, because it makes the trade-off real. Suddenly the question isn’t abstract willpower — it’s “is finding an extra $100 a month worth being free more than a year sooner?” For most people, seeing that specific payoff is exactly what makes them go find the extra money: cut a subscription, pick up a little extra work, trim somewhere. The concrete result justifies the sacrifice in a way that “you should pay extra” never could.

Where the extra money comes from

You don’t need to find hundreds out of nowhere. The extra can come from small, findable places: a couple of cancelled subscriptions you barely used, a temporary trim to some spending category, a bit of side income, a windfall like a tax refund or bonus put straight onto the debt instead of spent. Even a small consistent extra amount compounds into a meaningfully faster payoff.

And there’s a powerful accelerator built into the payoff journey itself: every time you finish paying off one debt, you free up that entire payment. Rolling that freed-up amount onto your next debt — rather than absorbing it back into spending — means your extra-payment power grows as you go. Each debt you kill makes the next one fall faster. The snowball (or avalanche) gathers speed precisely because of this.

A gentle dose of realism

I want to be honest and kind here at once. Extra payments are powerful, but only what you can genuinely afford. Don’t skip necessities, don’t neglect a small emergency buffer that keeps you from going further into debt when something breaks, and don’t set an extra-payment target so aggressive that you burn out and quit. Sustainable beats heroic. A modest extra amount you keep up for years beats a huge one you abandon in a month. Be kind to yourself; this is a marathon, and consistency wins it.

An important, caring note

Please note: this is a general explanation of how extra payments work — not financial, debt, or credit advice, and any timeline projections are simplified estimates that don’t fully account for compounding, fees, or rate changes, so always check your actual statements. And if debt feels overwhelming, please reach out — a non-profit credit counselling service can help, often for free. Asking for help is a strength, and no one should carry this alone.

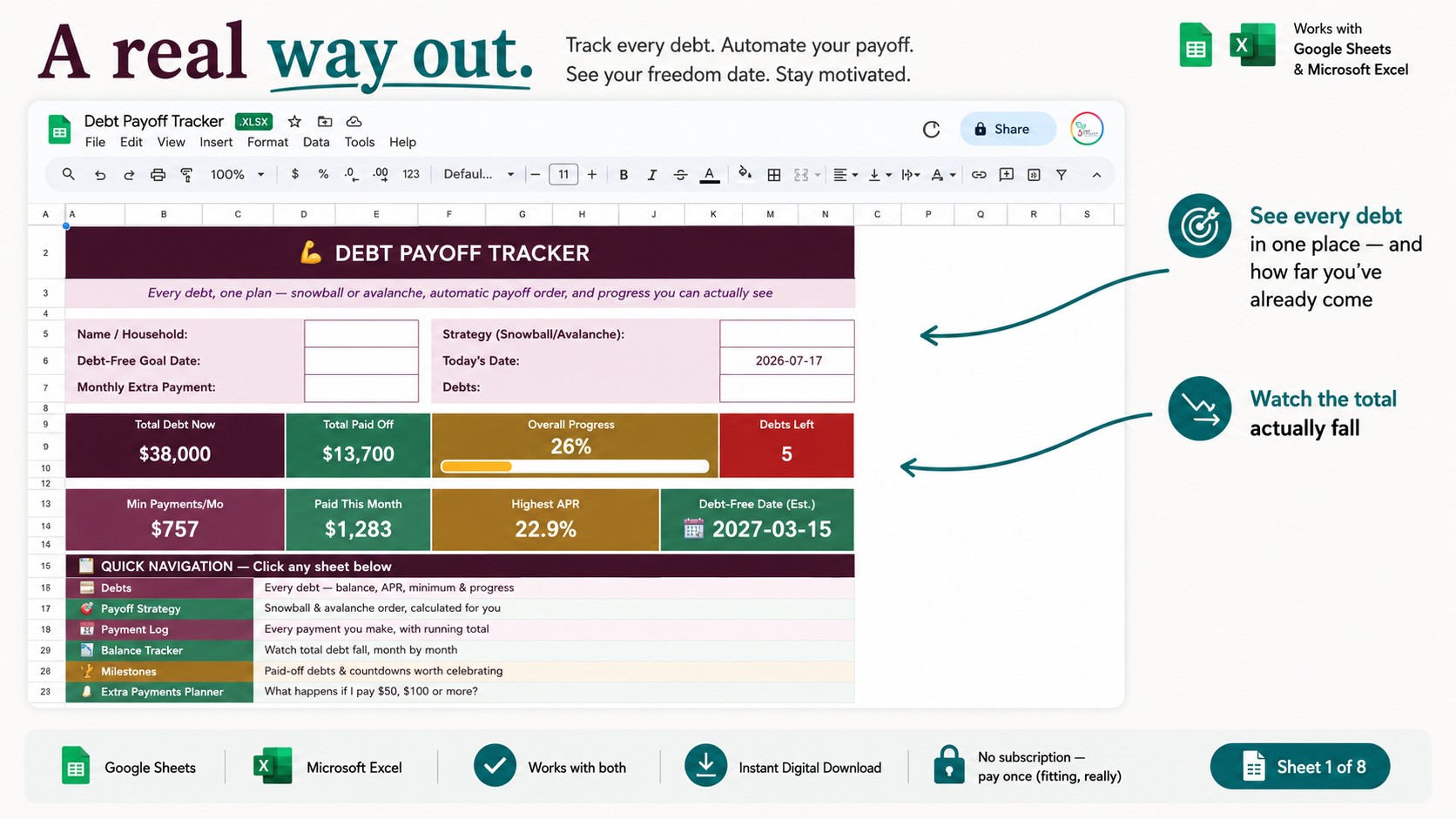

If you want to see your own numbers

I built an extra-payment planner into my debt payoff tracker in Google Sheets — enter an extra amount and it estimates how many months sooner you’d be free, so you can see your own personal “12 months faster,” alongside both payoff strategies and a month-by-month balance tracker:

👉 Debt Payoff Tracker for Google Sheets & Excel

Whether you use a tool or work it out yourself, look at what even a small extra payment would do to your timeline. That number — your personal “free this much sooner” — is one of the most motivating things you’ll see on your debt-free journey. Debt is a situation, not a character flaw, and every extra dollar is a brick out of the wall. You’ve got this.

This is a general explanation and organizing tool — not financial, debt or credit advice; projections are simplified estimates, so check your actual statements. If you’re struggling, a non-profit credit counselling service can help, often for free. What’s the extra amount you’re aiming for — and where’s it coming from? Share it in the comments; someone might need the idea.