$12 a Month Is $144 a Year: The Reframe That Makes You Act

Small monthly charges feel harmless precisely because they’re monthly. Look at the annual cost of your subscriptions instead, and everything changes.

There’s a reason subscriptions are priced by the month, and it’s not for your convenience. “$12 a month” sounds like nothing — the price of a couple of coffees, easily ignored. But that same subscription is $144 a year, and $144 is a number that makes you sit up. Same subscription, same money, wildly different emotional weight — purely because of the timeframe you view it through. Learning to look at the annual cost of subscriptions rather than the monthly price is one of the simplest and most powerful reframes in personal finance. Here’s why it works, and why the monthly framing is quietly costing you.

Why “per month” disarms your judgment

Subscription pricing is monthly because monthly numbers slip under your radar. Our brains treat small, recurring amounts very differently from large, one-off ones. A single $144 charge would make you pause and think. Twelve charges of $12, spread across a year, barely register — each one is small enough to wave through without a second thought.

This is the entire psychology that makes the subscription model so profitable. Break a meaningful annual cost into small monthly pieces, and each piece feels trivial. You’d never pay $600 upfront for something you use occasionally, but $50 a month? Sure, seems fine — and that’s $600 a year you’ve just agreed to without the flinch you’d have felt paying it all at once. The monthly framing is a feature for the seller and a trap for you.

The annual number cuts through it

The fix is almost embarrassingly simple: multiply by twelve (or convert whatever the billing cycle is into a yearly figure) and look at the annual cost. That’s it. But the effect is dramatic, because the annual number carries the emotional weight the monthly number hides.

“$15 a month for streaming” becomes “$180 a year for streaming.” “$50 a month across a few apps” becomes “$600 a year.” Seeing the annual figure triggers the judgment the monthly figure suppressed: Is this worth $180 a year to me? Is this really worth $600? Those are questions you can actually answer — and often the answer, once you’re looking at the real yearly number, is no.

Nothing about the money changed. You were always paying that annual amount; you just never looked at it that way. The annual view doesn’t cost you anything — it just stops the monthly framing from hiding what you’re really spending.

The total is the real gut-punch

Individual annual costs are eye-opening. The combined annual total is the thing that genuinely changes behavior. Because subscriptions don’t come alone — they come in a pile. Streaming, music, cloud storage, apps, memberships, tools. Each one small monthly, each one a moderate annual figure, and together?

When you add up the annual cost of all your subscriptions, the total is very often shockingly high — hundreds or even thousands of dollars a year that you never consciously decided to spend, because you only ever saw it $12 at a time. That total is the number that makes people finally act. It reframes “a few harmless subscriptions” as “a serious chunk of my annual budget,” which is what it actually is. Seeing the yearly total in one place is frequently the moment the cancelling begins.

What that annual money could be instead

There’s a final, motivating reframe: opportunity cost. Once you see the real annual total, you can ask what else that money could do. Your subscription total for a year might be a meaningful contribution to savings, a debt paid down faster, a proper holiday, or an emergency fund started. Framed as “$12 a month,” a subscription competes with nothing. Framed as “$144 a year, or a chunk of a holiday,” it suddenly has to justify itself against things you might want more.

This isn’t about depriving yourself — the subscriptions you genuinely value are worth every dollar. It’s about making the trade-off visible, so you’re consciously choosing your subscriptions over the other things that money could become, rather than defaulting into them one small charge at a time.

A quick caveat

One honest note: converting to annual figures is a way of seeing your spending clearly — it’s not financial advice, and the numbers are your own. Before cancelling anything based on its annual cost, check the actual terms and your real statements (some annual plans are cheaper than monthly, some have commitments). Use the annual view to understand what you’re really spending; make changes with the actual details in front of you.

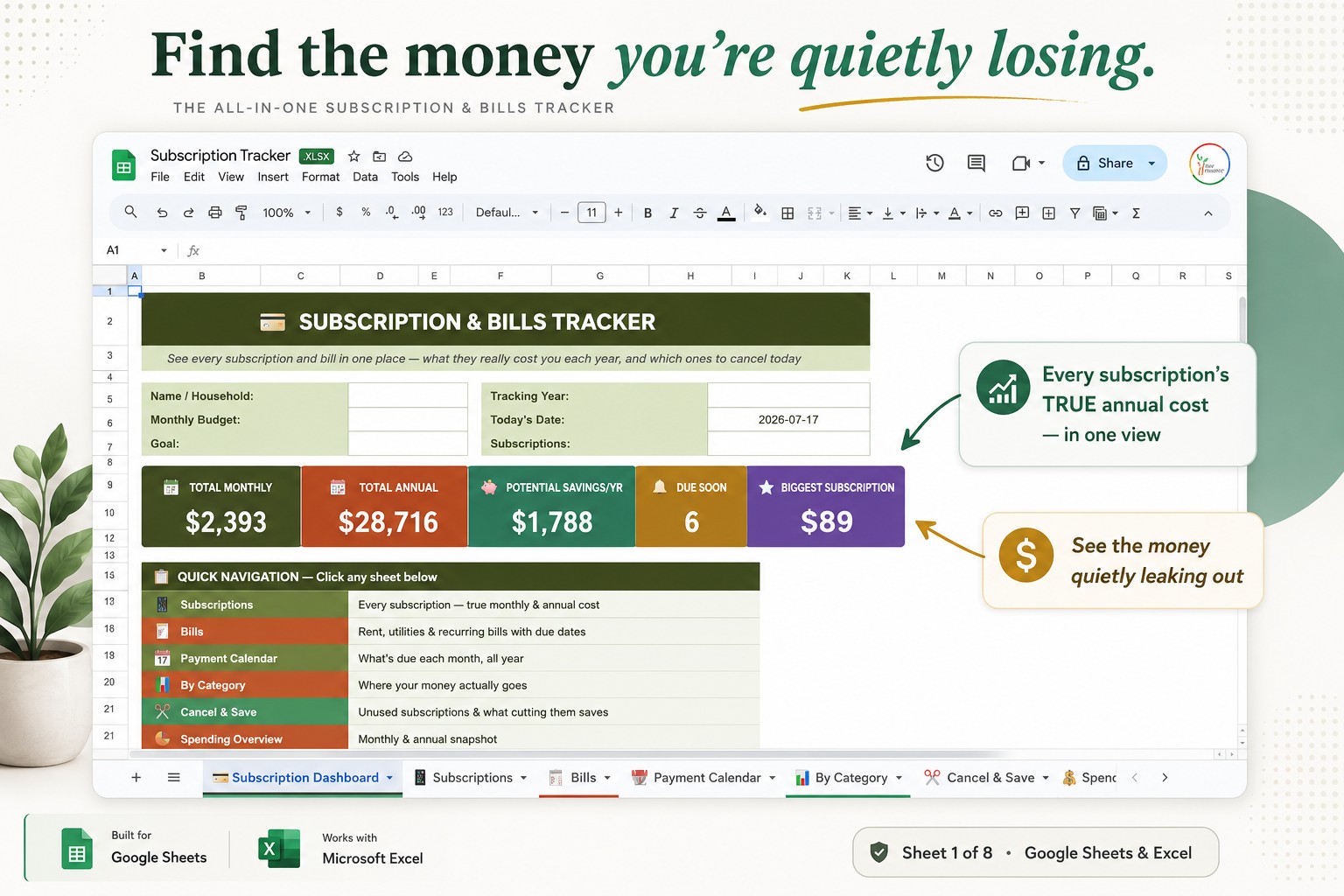

If you want the annual numbers done for you

I built automatic annual-cost conversion into my subscription tracker in Google Sheets — enter any billing cycle and it shows the true monthly and annual cost of each subscription, plus your combined annual total and where it all goes:

👉 Subscription Tracker for Google Sheets & Excel

Whether you use a tool or a calculator, stop looking at your subscriptions by the month. Multiply everything out to the year, add up the total, and look at the real number. It’s the same money you were always spending — but seen annually, it finally gets the attention it deserves. And attention, it turns out, is all it takes to stop losing money $12 at a time.

This is a personal-finance perspective and organizing tool — not financial advice. Check each subscription’s terms and your actual statements before making changes. What was your combined annual subscription total when you finally added it up? Share it in the comments — the number surprises everyone.