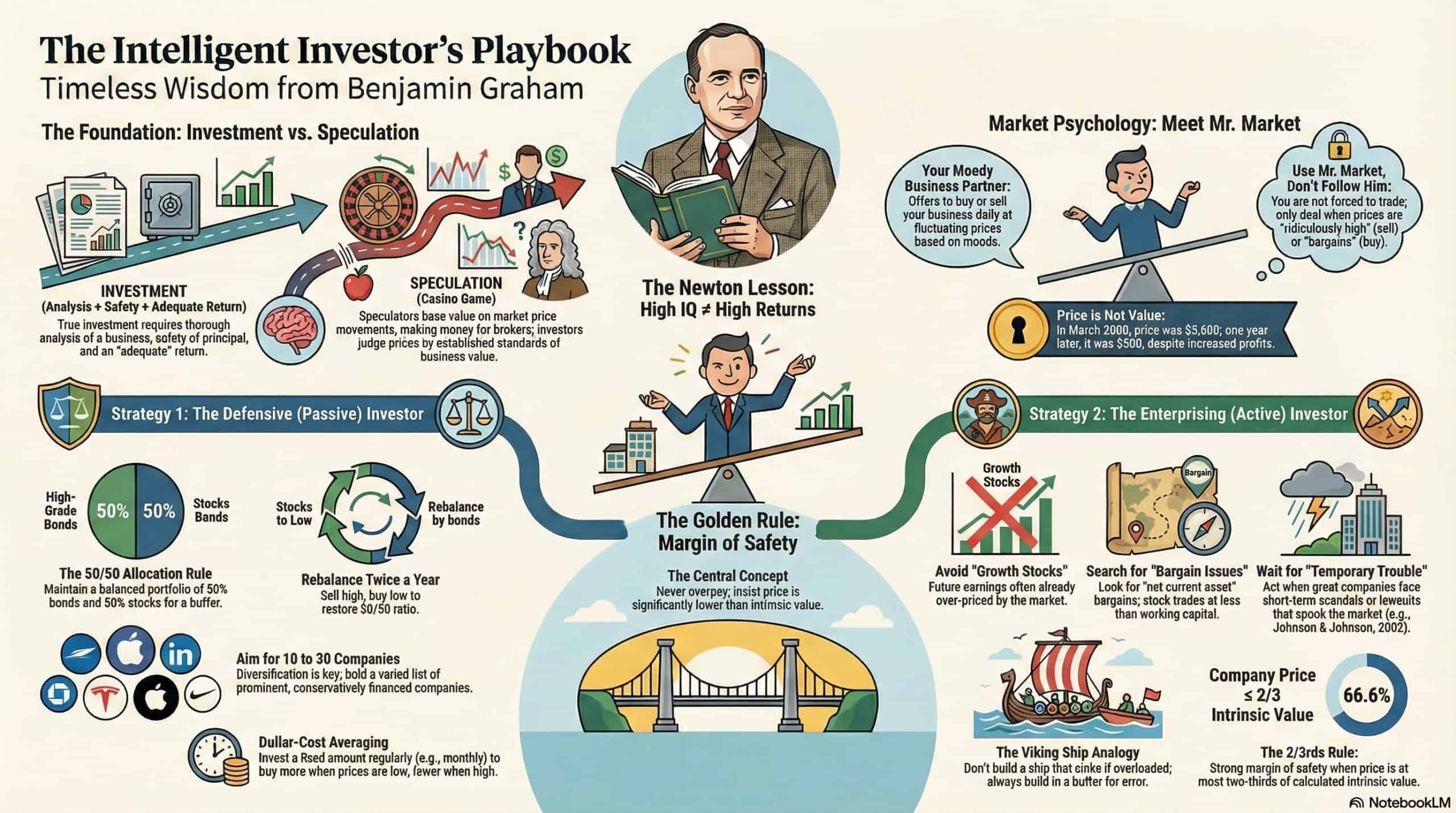

We have been conditioned to believe that the market is a playground for the elite—a complex machine that requires a stratospheric IQ, a PhD in mathematics, or a list of insider secrets to navigate. This is a lie that Benjamin Graham dismantled decades ago.

In his seminal work, The Intelligent Investor—the book Warren Buffett calls “by far the best book on investing ever written”—Graham reveals a transformative truth: successful investing is not about being the smartest person in the room; it is about being the most disciplined. Graham defines “intelligence” not as academic brilliance, but as emotional control and patience. As he famously put it, intelligence is a trait more of the character than of the brain.

If you are ready to stop gambling and start building, here are the five timeless pillars of the “Intelligent Investor” framework.

1. Your Temperament Outperforms Your Brain (The Newton Lesson)

To understand that raw brainpower is no shield against market folly, one need only look at Sir Isaac Newton. The man who discovered gravity and reshaped human understanding of the universe was, in Graham’s eyes, a “fool” when it came to the market.

In the early 1700s, Newton invested in the South Sea Company. Sensing a bubble, he initially sold his shares for a 100% profit. But as the market continued to surge, the “sting of embarrassment” from seeing his friends get richer drove him back in. He reinvested at the peak, losing £20,000—over $3 million in today’s value. Newton spent the rest of his life forbidding anyone to even mention the words “South Sea” in his presence.

“I can calculate the motions of heavenly bodies, but not the madness of men.”

Newton’s failure underscores the core principle of value investing: Intelligence is a trait of character, not the brain. The “Intelligent Investor” is not a person with the highest IQ, but the person with the courage to think independently and the discipline to keep their emotions from corroding their intellectual framework.

2. Meet Mr. Market—Your Bipolar Business Partner

Graham used a brilliant metaphor to explain market volatility: Imagine you own an interest in a business, and every day a bipolar partner named Mr. Market offers to either buy your share or sell you his. His moods range from “pure gibberish” and extreme pessimism to “ridiculously high” optimism.

The market is frequently irrational. For instance, in March 2000, Mr. Market estimated a share’s value at $2,600. Just one year later, in March 2001, he valued that same share at $500—even though the company’s profits had actually increased by 20% during that period.

In the 1970s, Mr. Market arrived once a day with the morning newspaper. In our digital era, he is an addictive video game on your smartphone, knocking on your door with notifications 100 times a day. He is more persistent now, but he is no more informed.

Mr. Market is your servant, not your master. His daily prices are not instructions on what your business is worth; they are merely opportunities. You should be happy to sell to him when he offers a price that is nonsense-high, and happy to buy from him when he presents you with a bargain.

3. The “Margin of Safety” as an Insurance Policy

The risk that no amount of analysis can eliminate is the risk of being wrong. To protect against this, Graham insisted on a “Margin of Safety.”

Think of it like building a ship. You wouldn’t construct a vessel that sinks if 31 Vikings board it when you know you will regularly transport 30. You build it with the capacity to handle 50. In the market, this means never paying the full “calculated value” for a stock. If you think a company is worth $31, but it is currently priced at $30, you have no room for error. If your calculation is off by just a few percent, you have overpaid. Graham’s rule was to buy only when the price is significantly lower than the value—ideally at two-thirds of its intrinsic worth.

“The really dreadful losses of the past few years… were realized in those common-stock issues where the buyer forgot to ask ‘How much?'”

Without a margin of safety, you aren’t investing; you are walking a tightrope without a net.

4. The Invisible Wall Between Investing and Speculating

A primary goal for any wealth builder is to distinguish between an “investment operation” and speculation. Speculators are gamblers chasing “hot” stocks and reacting to headlines; they make money for their brokers, not themselves.

The danger of speculation comes from both “laziness” and “euphoria.” In the 1990s tech bubble, we saw the “Tempco vs. Ticketmaster” confusion, where traders tripled the price of an obscure company (TMCO) simply because they mistook its ticker for Ticketmaster (TMCS). We also saw “Inktomy,” a company with a $25 billion valuation that had never made a single dollar in profit. By the time the bubble popped, the stock plummeted from $231 to just 25 cents.

To stay on the right side of the wall, an operation must meet The Investor’s Checklist:

• Thorough Analysis: Study the business model, leadership, and financials.

• Safety of Principal: Ensure the investment protects against total loss.

• Adequate Return: Aim for reasonable, consistent gains, not overnight miracles.

5. Why High Reward Doesn’t Always Mean High Risk

Academic theory often claims that risk and reward are always correlated—that to get higher returns, you must accept more danger. Graham fundamentally disagreed.

Consider the “Russian Roulette” story from the obscure bars of Moscow at 4:00 am. An academic would say that if you demand $100,000 to take two shots (33% risk) vs. $10,000 for one shot (16% risk), you are being rational. But Graham shows that value investing flips this logic.

If you find a way to buy a dollar for 60 cents, you have a potential reward. If you find a way to buy that same dollar for 40 cents, your potential reward is much higher, yet your risk is mathematically lower because you have a larger margin of safety. In this framework, the maximum return goes to the investor who exercises the most discipline and “intelligent effort” to find bargains, not the one who stomachs the most danger.

Conclusion: Putting the Foundations Under Your Castles

The core of Benjamin Graham’s philosophy is that you do not need to beat the market through luck; you simply need to discipline yourself. As Henry David Thoreau once wrote:

“If you have built castles in the air, your work need not be lost; that is where they should be. Now put the foundations under them.”

Graham’s principles—temperament, the Margin of Safety, and the strict wall between investment and speculation—are the foundations that keep your financial castles from crumbling.

Ask yourself: Are you thinking like a casino player, or are you thinking like a business owner? Next time Mr. Market knocks on your phone with a “can’t-miss” tip, will you be his master, or his servant?