Invoiced vs Collected: Why Your Revenue Isn’t What You Think

The amount you’ve billed and the amount you’ve actually been paid are two very different numbers. Confusing invoiced vs collected is how freelancers get blindsided by cash flow.

Here’s a mistake I made early in freelancing that quietly caused me real stress. I’d look at what I’d invoiced in a month, feel good about the number, and mentally treat it as my income. Then I’d wonder why my bank account didn’t match my sense of how well business was going. The answer was a distinction I hadn’t internalized: the money I’d invoiced was not the money I’d collected. They’re different numbers, sometimes very different, and conflating them is one of the most common ways small businesses and freelancers get blindsided by cash flow. Understanding invoiced vs collected changed how I read my own business. Here’s why it matters.

Two numbers that feel like one

When you send an invoice, it’s easy to feel like you’ve earned that money. You did the work, you billed for it — done, right? But invoicing and getting paid are two separate events, often separated by weeks or months. The invoiced amount is what you’ve billed; the collected amount is what’s actually landed in your account. Until a client pays, invoiced money is a promise, not cash.

The trap is treating invoiced money as if it’s already yours to spend or count. Your invoiced total might look healthy while your collected total — the money you can actually use — lags well behind, tied up in unpaid invoices. If you plan your spending, your sense of success, or your business decisions around the invoiced number, you’re building on money you don’t yet have. That’s how a business that looks profitable on paper runs short of actual cash.

Why the gap causes real problems

The gap between invoiced and collected is where cash flow problems live. You can have a great month on paper — lots invoiced — and still not be able to pay your own bills, because that money is sitting in accounts receivable, unpaid. Cash flow, not paper revenue, is what actually keeps a business alive. Plenty of profitable-on-paper businesses have run into serious trouble simply because their collected cash didn’t arrive in time to cover their real outgoings.

For freelancers especially, this matters enormously. Your invoiced income might be steady, but if clients pay slowly, your actual incoming cash is lumpy and delayed. Understanding that distinction is the difference between managing your money based on reality (what you’ve collected) versus fantasy (what you’ve invoiced but might not see for months).

Tracking both changes how you see your business

The fix is simple: track both numbers, separately and clearly. See what you’ve invoiced and what you’ve actually collected, and the gap between them. That gap — your outstanding accounts receivable — is one of the most important numbers in your business, and most freelancers never look at it directly.

When you track both, several things become clear:

- Your real income is what you’ve collected, not what you’ve invoiced. Planning around collected cash keeps you grounded in reality.

- Your outstanding receivables (the gap) show how much of your billed work is still tied up unpaid — money to chase, and a risk to manage.

- Your collection patterns become visible: how long, on average, between invoicing and getting paid, which helps you plan cash flow and spot clients who consistently pay slowly.

That clarity transforms how you make decisions. You stop being surprised by the mismatch between your “revenue” and your bank balance, because you understand exactly where the difference is and why.

The insight: manage cash flow, not just revenue

The deeper lesson is that for a small business or freelancer, cash flow is the number that matters day to day, not headline revenue. Revenue (invoiced) tells you how much business you’re doing; cash flow (collected) tells you whether you can pay your bills this month. Both matter, but confusing them is dangerous. The businesses that stay healthy are the ones that watch what’s actually coming in, manage the gap between billed and collected, and never spend money they’ve only invoiced.

Tracking invoiced versus collected is how you keep that distinction front and centre. It’s a small shift in what you measure, but it’s the difference between managing your business on reality and being repeatedly surprised by it.

A quick note

As always: tracking your invoiced and collected amounts is an organizing tool for understanding your own cash flow — not accounting, tax, or financial advice. Keep your official records, and consult a qualified professional for bookkeeping, tax, and financial decisions. Use tracking to see your cash flow clearly; rely on a professional for the accounting.

If you want to see both numbers clearly

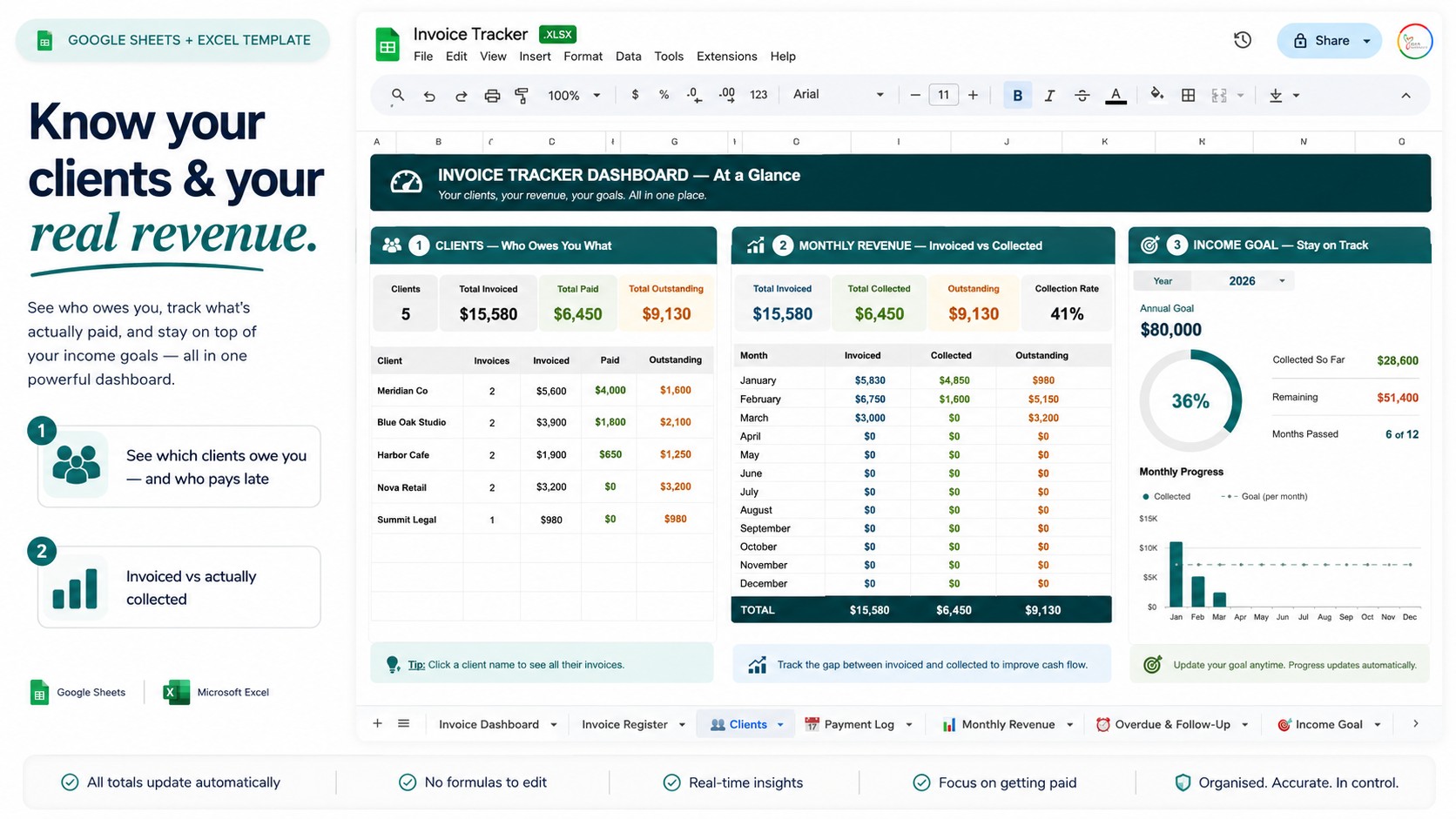

I built invoiced-versus-collected tracking into my invoice tracker in Google Sheets — see what you’ve billed, what you’ve actually collected, and your outstanding receivables at a glance, alongside per-client totals and overdue tracking:

👉 Invoice Tracker for Google Sheets & Excel

Whether you use mine or build your own, stop treating invoiced money as collected money. Track both, watch the gap, and manage your business on the cash you actually have — not the cash you’ve only billed. It’s a simple distinction that will keep you from ever being blindsided by the difference between looking profitable and actually having money in the bank.

This reflects my own experience and is a tracking tool — not accounting, tax or financial advice; keep official records and consult a professional. Have you ever been caught out by the gap between invoiced and collected? Tell me in the comments.