Don’t Lose Your FSA Money: How Tracking Your HSA and FSA Keeps It Yours

FSA funds are often use-it-or-lose-it, and people forfeit real money every year by forgetting. Here’s how simple HSA FSA tracking makes sure that money stays yours.

If you have a Flexible Spending Account (FSA), there’s a quietly painful fact you may have run into: FSA money is often “use it or lose it.” Contribute to it, don’t spend it by the deadline, and you can forfeit it — money you earned, set aside, and then simply lost back. Every year, people give up real money this way, usually just because they lost track. And Health Savings Accounts (HSAs), while more forgiving, come with their own things worth tracking. Getting deliberate about HSA FSA tracking is one of those small financial habits that quietly saves you real money. Here’s how it works and why it matters.

The use-it-or-lose-it trap

Let’s start with the FSA, because that’s where money actually gets lost. An FSA lets you set aside pre-tax money for healthcare expenses — which is a genuine benefit, since it lowers your taxable income. The catch is the deadline: FSA funds typically must be used within the plan year (sometimes with a small grace period or limited carryover, depending on your plan). Whatever’s left when the deadline passes can be forfeited.

So the very thing that makes an FSA valuable — pre-committing money for healthcare — becomes a trap if you don’t spend it in time. People contribute a sensible amount, then get busy, forget how much is left, and realize too late that they’ve left money on the table. It’s a completely avoidable loss, and it happens constantly, purely because the balance and the deadline weren’t being watched.

The fix: always know your balance and your deadline

The solution is simple: track your FSA balance and know your deadline. When you can see, at any point in the year, how much FSA money you have left and when it needs to be spent, the whole trap disappears. If you’re approaching the deadline with a balance remaining, you know to use it — on eligible expenses you may have been putting off, or planned purchases you can bring forward.

That advance awareness is everything. FSA money is only lost when the deadline surprises you. Track the balance and the date, and it never surprises you. You either spend it deliberately on things you need, or you at least make a conscious choice — instead of discovering the loss after it’s gone. A little visibility turns a common, painful forfeit into a non-event.

HSAs are different — but still worth tracking

Health Savings Accounts work differently and are more forgiving: HSA money is generally yours to keep, rolls over year to year, and can even be invested and grow over time. There’s no use-it-or-lose-it deadline in the same way. So why track it?

Because an HSA is a genuinely valuable account worth managing well. Tracking your contributions helps you stay aware of annual limits and make the most of the tax advantages. Tracking your spending versus your balance helps you decide whether to spend from it now or let it grow for the future (many people treat a well-funded HSA as a long-term health-cost or even retirement asset). And keeping records of what you spend it on matters for staying organized and compliant. An HSA isn’t a use-it-or-lose-it risk, but it is a valuable tool that rewards attention.

Keep the records for reimbursement, too

There’s a related benefit to tracking here: reimbursement. Sometimes you pay for an eligible expense out of pocket and can be reimbursed from your FSA or HSA — but only if you keep the record and actually submit it. It’s easy to pay for something, mean to get reimbursed, and forget. Tracking your eligible expenses and which ones you’ve been reimbursed for makes sure you claim the money you’re entitled to, rather than leaving it sitting in an account you forget to draw from.

Small habit, real money

I want to be honest that, like a lot of good financial admin, this isn’t thrilling — it’s the quiet, practical kind of money management. But it’s genuinely worthwhile. Forfeited FSA money is pure loss, and it’s entirely avoidable. Unclaimed reimbursements are money you already earned, left behind. A little tracking turns these avoidable losses into money that stays where it belongs — with you. For the small effort of watching a couple of balances and dates, the payoff is real.

An important note

As always with anything involving health accounts, taxes, and money: this is a personal-organization perspective, not tax, financial, or benefits advice. HSA and FSA rules — contribution limits, eligible expenses, deadlines, carryover provisions — are specific, vary by plan, and change over time. Always confirm the details of your own accounts with your plan administrator and official plan documents, and consult a qualified professional for tax and financial decisions. Use tracking to stay aware and organized; rely on official sources for the rules.

If you want a way to track them

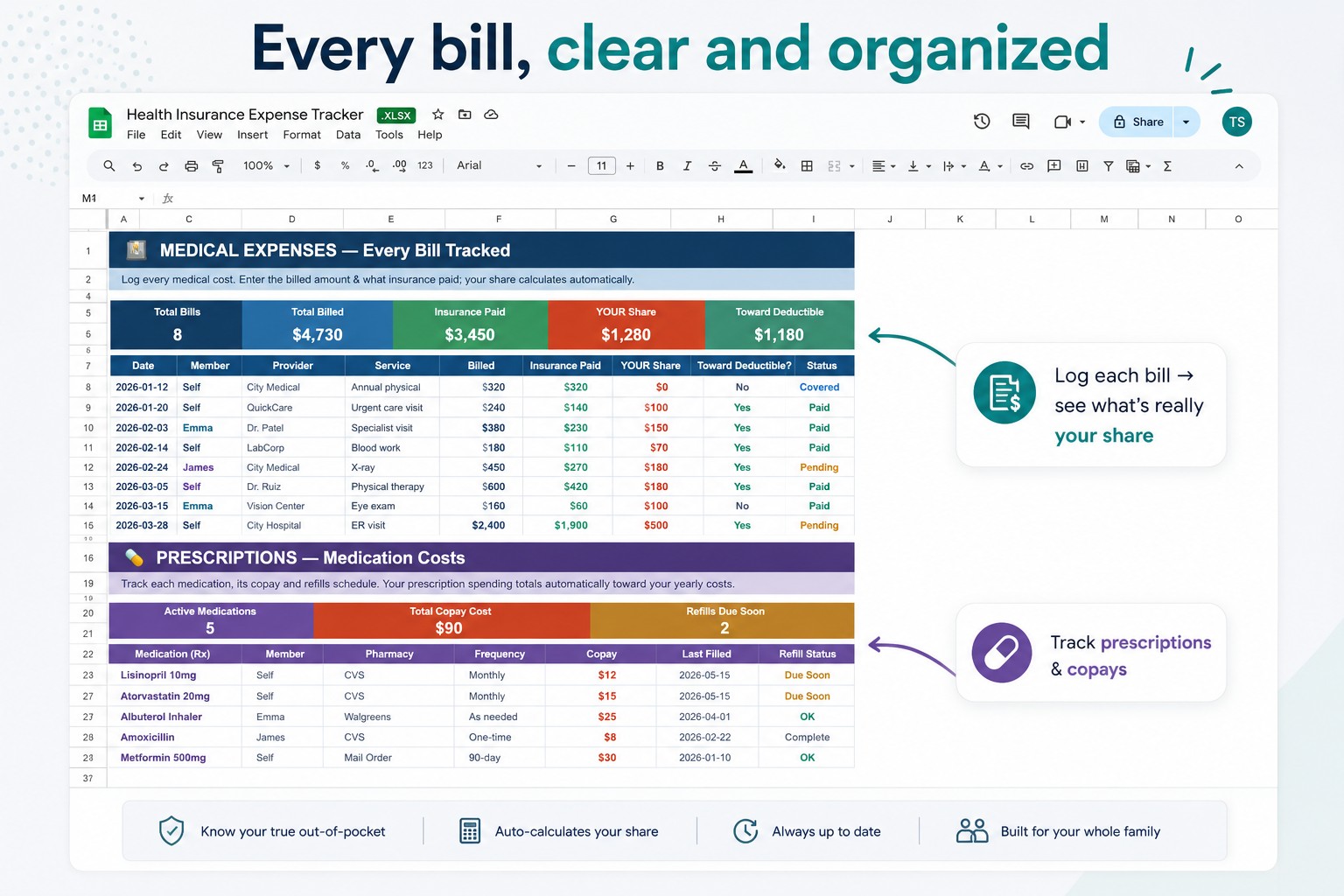

I built HSA and FSA tracking into my health expense tracker in Google Sheets — see your contributions, spending, and running balance, with awareness of your FSA deadline, alongside your medical expenses, deductible progress, and reimbursements owed:

👉 Health Insurance Expense Tracker for Google Sheets & Excel

Whether you use mine or a simple note, start watching your HSA and FSA balances. Don’t let use-it-or-lose-it money slip away, and don’t leave reimbursements unclaimed. It’s some of the easiest money you’ll ever “make” — by simply not losing money that was already yours.

This is a personal-organization perspective — not tax, financial or benefits advice. HSA/FSA rules vary by plan and change; confirm details with your plan administrator and official documents, and consult a qualified professional. Have you ever lost FSA money to the deadline? Let this be your reminder to check your balance — and tell me in the comments.