In the modern economic landscape, “short-termism” is frequently discussed as a moral or cultural failing. However, from the perspective of decision science and behavioral economics, it is more accurately described as a structural misalignment between human biology, institutional incentives, and the mathematical reality of compounding. The tendency to prioritize immediate gains at the expense of long-term stability is not merely a lapse in judgment; it is a default setting of the human cognitive architecture that has been exacerbated by modern information systems.

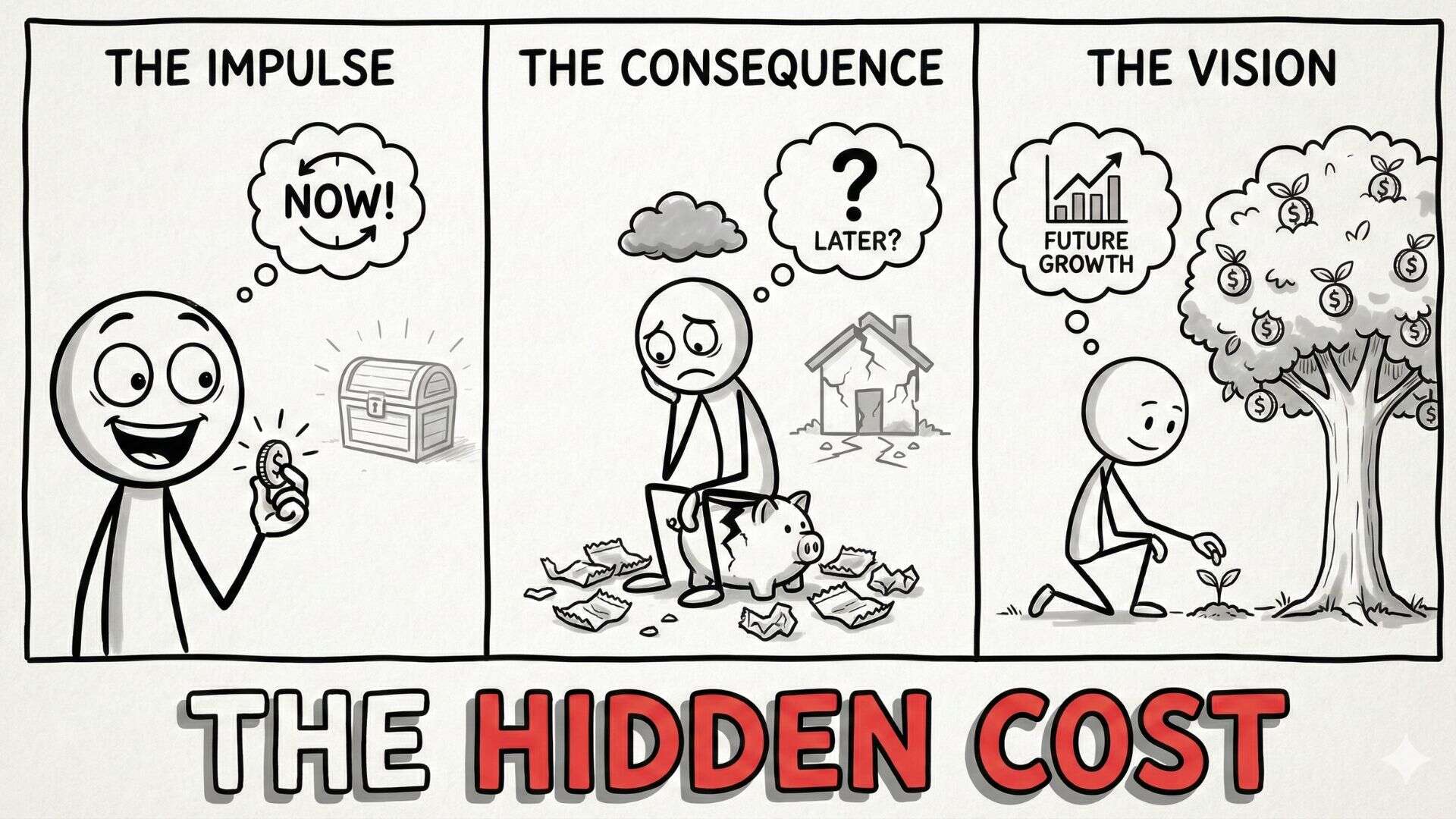

The hidden cost of short-term financial thinking is rarely visible in a single transaction. Instead, it manifests as a cumulative erosion of optionality, an increase in system fragility, and the catastrophic loss of the most powerful force in economics: time. For individuals and organizations in the United States and Europe, understanding the causal mechanisms behind this behavior is essential for navigating environments that increasingly reward high-velocity, low-depth decision-making.

1. The Causal Mechanism of Short-Termism: Temporal Discontinuity

The core problem of short-term financial thinking is rooted in what psychologists call temporal discounting. This is the phenomenon where the perceived value of a reward decreases as the delay to receive that reward increases. While a rational model would suggest a consistent, exponential decline in value over time, human behavior follows a more erratic path.

The Biological Imperative

From an evolutionary standpoint, short-termism was a survival heuristic. In environments characterized by high caloric scarcity and physical danger, an immediate resource (food, shelter, or security) held infinitely more value than a theoretical resource in the future. The “future” was not guaranteed; therefore, discounting it heavily was a logical strategy for survival.

In a modern financial context, this biological bias creates a “temporal discontinuity.” The brain’s limbic system, which processes immediate rewards and emotions, often overrides the prefrontal cortex, which is responsible for long-term planning and abstract reasoning. When an individual chooses a minor immediate gain over a significant future benefit, they are not necessarily “failing” to think; they are responding to a deeply ingrained biological drive that treats the future as a high-risk uncertainty.

The Shift from Stewardship to Velocity

Historically, wealth was often tied to physical assets—land, infrastructure, or family enterprises—that required multi-generational stewardship. The inherent illiquidity of these assets forced a long-term horizon. In contrast, the modern digital economy is characterized by extreme liquidity and high-frequency feedback. When capital can be moved across the globe in milliseconds, the incentive structure shifts from “building” to “extracting.” This velocity creates a feedback loop where the speed of the transaction is mistaken for the quality of the decision.

2. Why the Problem Persists: The Feedback Gap and Path Dependency

If short-term thinking is so destructive, why does experience not naturally correct it? The persistence of this problem is driven by two primary factors: the Feedback Gap and Path Dependency.

The Feedback Gap

In most learning environments, the interval between an action and its consequence is short. If a person touches a hot stove, the feedback is instantaneous, and the lesson is learned. In finance and career planning, however, the feedback for short-termism is often delayed by years or decades.

A company may cut its Research and Development (R&D) budget to meet a quarterly earnings target. In the short term, the stock price rises, and executives receive bonuses—a positive feedback loop. The negative feedback (the loss of competitive edge and product obsolescence) may not appear for five to ten years. By the time the consequence arrives, the original decision-makers are often gone, and the system has already been compromised. This “asymmetric feedback” rewards short-term behavior while masking long-term decay.

Read also: How Emotional Investing Destroys Long-Term Wealth: a Cognitive Analysis

Path Dependency

Decisions made with a short-term horizon often create “Path Dependency,” where the options available in the future are constrained by the choices made today.

- The Debt Trap: Taking on high-interest debt for immediate consumption is a classic short-term decision. The immediate gain is the utility of the purchase. The path-dependent consequence is that a portion of all future income is now “locked” into debt service, reducing the individual’s ability to take risks or invest in the future.

- Specialization Over-Optimization: In a career context, an individual might focus exclusively on a narrow, high-paying skill that is currently in demand. While this maximizes short-term income, it creates a fragile path. If that industry shifts or the skill becomes automated, the individual lacks the broad-based “meta-skills” required to pivot.

3. Real-World Outcomes: The Triple Cost of Myopia

Short-term thinking imposes a “triple cost” on real-world outcomes: the Opportunity Cost of Compounding, the Cost of Fragility, and the Complexity Tax.

The Opportunity Cost of Compounding

Compounding is mathematically back-loaded. The vast majority of gains in any long-term endeavor—whether it is an investment portfolio, a professional reputation, or a technical skill—occur in the final 20% of the time horizon.

Short-term thinking leads to “frequent restarts.” Every time an investor exits a position because of a temporary dip, or a professional switches industries to chase a 5% salary increase, they reset their compounding clock. The hidden cost is not the loss of the immediate gain, but the “unearned” wealth that would have accrued twenty years later.

The Cost of Fragility

Short-term systems are optimized for efficiency rather than resilience. A business that operates with “just-in-time” inventory and zero cash reserves is highly efficient and profitable during stable times. However, it is also extremely fragile. When a “Black Swan” event—such as a pandemic or a geopolitical crisis—occurs, the short-term optimized system collapses. The hidden cost here is the total loss of the enterprise, which far outweighs the marginal gains achieved through extreme efficiency.

The Complexity Tax

Short-term fixes often involve layering new solutions on top of broken foundations. In software engineering, this is known as “technical debt.” In finance, it might involve complex hedging or refinancing to cover up a lack of underlying profitability. Eventually, the system becomes so complex that the energy required to maintain it exceeds the energy produced by it.

4. The Mental Model: Hyperbolic Discounting

To navigate the problem of short-termism, one must master the mental model of Hyperbolic Discounting.

Defining the Model

Hyperbolic discounting is a mathematical model that describes how humans value rewards. In a standard “rational” model (Exponential Discounting), the value of a reward drops by a fixed percentage for every unit of time delayed. If you prefer $100 today over $110 in a month, you should also prefer $100 in a year over $110 in thirteen months.

Human beings do not function this way. We are “hyperbolic.” We will choose $100 today over $110 tomorrow (extreme short-term preference), but we will easily choose $110 in thirty-one days over $100 in thirty days. When the rewards are in the “far future,” we are rational. When one reward is in the “immediate present,” we become impulsive.

Why the Model Matters

Understanding hyperbolic discounting allows an individual to recognize that their “future self” and “present self” have different incentive structures. The present self wants the dopamine hit of the spend or the quick win. The future self wants the security of the saved capital. The hidden cost of short-term thinking is effectively a “transfer of wealth” from your future self to your present self, usually at a highly disadvantageous exchange rate.

Read also: The One Page Financial Plan Summary: STOP OVERTHINKING YOUR MONEY (CARL RICHARDS REVIEW)

5. Applying Better Thinking: Principles of Long-Term Reasoning

Improving decision-making requires moving away from “willpower” and toward Architectural Constraints. One cannot simply “decide” to be a long-term thinker while living in a short-term environment.

1. Lengthen the Feedback Loop

If the problem is a feedback gap, the solution is to create artificial feedback loops for long-term goals. This involves shifting focus from Outcomes (which take a long time) to Systems (which can be measured daily). Instead of measuring the growth of a fund, one measures the consistency of the contribution. This provides the “present self” with a sense of progress while allowing the “future self” to benefit from the outcome.

2. The Margin of Safety

A core principle of long-term reasoning is the Margin of Safety. This is the practice of building “slack” into a system.

- In finance: Maintaining cash reserves that the “math” says are unnecessary.

- In career: Developing “redundant” skills that are not currently required for your job.

- In business: Choosing a slower growth rate that ensures the company can survive a 30% drop in revenue.The Margin of Safety is an insurance policy against the fragility created by short-term optimization.

3. Incentives Audit

One must ruthlessly analyze the incentives of the environment. If a professional is in a role where bonuses are tied exclusively to quarterly targets, they will inevitably become a short-term thinker. Long-term reasoning often requires “exiting” environments where the incentives are misaligned with long-term capital preservation.

6. Common Misunderstandings: Survival vs. Short-Termism

It is a common oversimplification to equate all immediate action with “short-termism.” There is a critical distinction between Tactical Agility and Strategic Myopia.

- Tactical Agility: Making quick adjustments to respond to new data while maintaining the same long-term objective. This is necessary and beneficial.

- Strategic Myopia: Changing the long-term objective because of a short-term emotional or financial impulse. This is destructive.

Furthermore, short-termism is not always a choice; for those in genuine survival situations (the “bottom” of Maslow’s hierarchy), hyperbolic discounting is a rational survival mechanism. The “Hidden Cost” discussed in this article applies primarily to those who have the capacity to choose a longer horizon but are prevented from doing so by cognitive biases or institutional structures.

7. Connection to Related Thinking Frameworks

Short-term thinking does not exist in a vacuum; it is influenced by and influences several other mental models:

- The Principal-Agent Problem: This occurs when the interests of the person making the decision (the agent, e.g., a CEO) are different from the interests of the person affected by the decision (the principal, e.g., the long-term shareholder). The agent is often incentivized to maximize short-term metrics to increase their own compensation.

- Second-Order Thinking: Short-term thinkers stop at “First-Order Thinking” (What is the immediate result of this action?). Long-term thinkers use “Second-Order Thinking” (What are the consequences of that result in five years?).

- First Principles Thinking: Instead of following the “short-term” trends of the market (reasoning by analogy), long-term thinkers break a problem down to its fundamental truths. If the fundamental value of an asset hasn’t changed, a short-term price drop is irrelevant noise.

8. Conclusion: The Power of the Long Horizon

The hidden cost of short-term financial thinking is the sacrifice of the future on the altar of the immediate. In a world that is increasingly optimized for the “now,” the ability to maintain a ten, twenty, or thirty-year time horizon is perhaps the most significant competitive advantage an individual or organization can possess.

Wealth, reputation, and mastery are not events; they are the “residual” of thousands of decisions where the individual chose to delay gratification, build resilience, and respect the laws of compounding. By understanding the biological roots of temporal myopia and implementing structural systems to counteract them, we can stop paying the “tax” of short-termism and begin capturing the exponential rewards of the long horizon.

Would you like me to develop a “Long-Term Strategy Audit” for a business or career context based on these principles, or perhaps explore the “Principal-Agent Problem” in more detail as it relates to corporate decision-making?