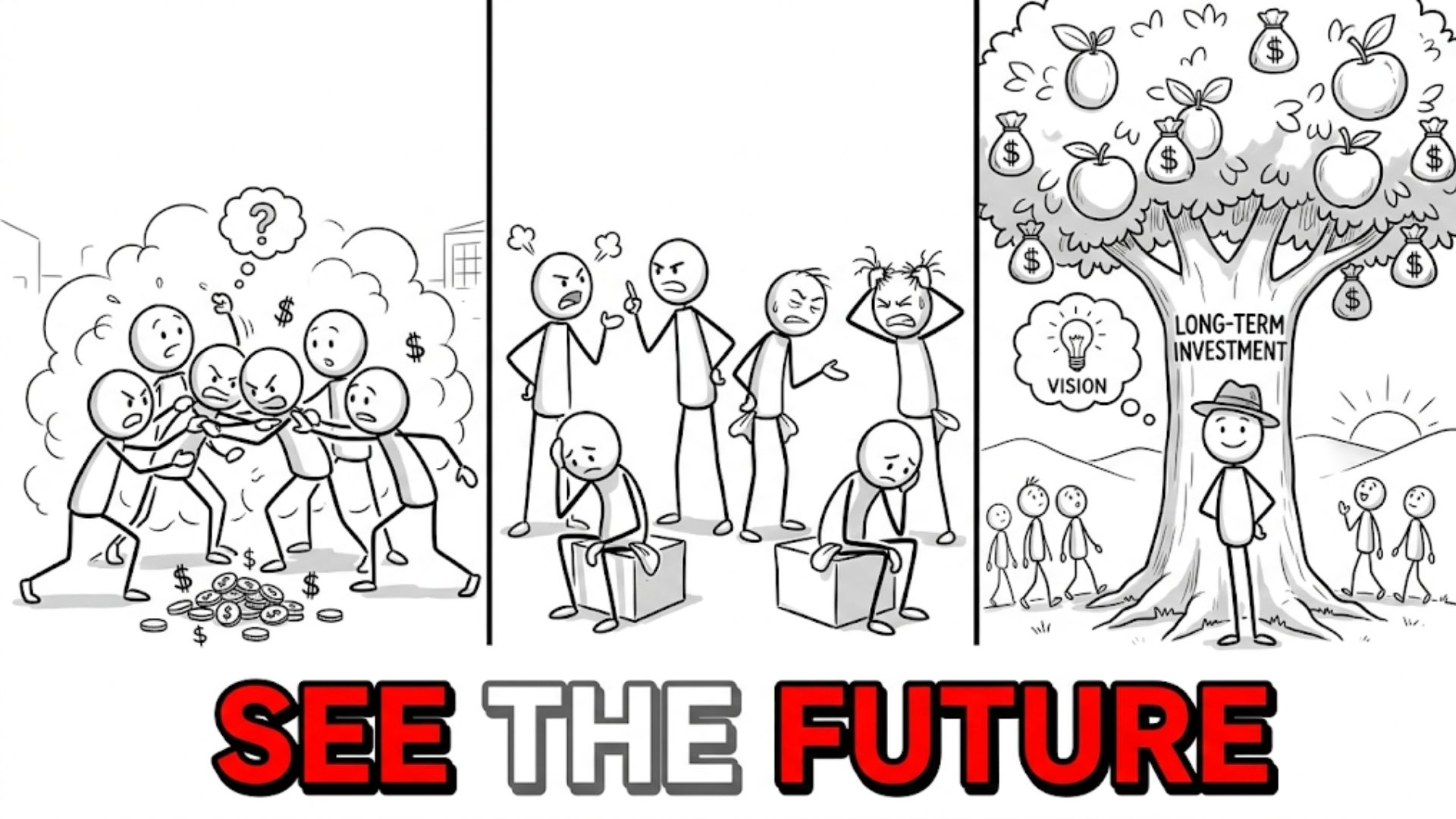

The concept of “long-term thinking” occupies a unique position in modern strategic discourse. It is simultaneously the most universally endorsed principle of success and the most consistently ignored practice in institutional and individual decision-making. In corporate boardrooms, political arenas, and personal career planning, the rhetorical commitment to “investing for the future” is nearly ubiquitous. Yet, the empirical reality reveals a systematic bias toward immediacy, characterized by quarterly earnings obsessions, short-term political cycles, and the rapid “churn” of human and financial capital.

This discrepancy is not a product of widespread intellectual failure or a lack of moral fortitude. Rather, the rarity of long-term thinking is a structural outcome of how human biology, institutional incentives, and information environments are architected. To understand why long-term thinking is rare—and why its rarity creates a massive strategic advantage for those who can maintain it—requires a deconstruction of the causal mechanisms that enforce short-termism. By examining the misalignment between time, incentives, and feedback, we can identify the “time arbitrage” available to the disciplined actor.

Read also: The Cost of Overconfidence in Investing

The Structural Constraint: Human Temporal Bias

The most foundational barrier to long-term thinking is biological. Human cognition evolved in an environment where immediate survival was the primary metric of success. For the vast majority of evolutionary history, the certainty of a resource today outweighed the probabilistic promise of a larger resource in the future.

Temporal Discounting and Hyperbolic Models

In behavioral economics, this is analyzed through the lens of temporal discounting. Most standard economic models assume exponential discounting, where a reward loses value at a constant rate over time. However, human behavior more closely follows a hyperbolic discounting model. In this framework, individuals demonstrate an extreme preference for immediate rewards over delayed ones, but this preference flattens out as the time horizon extends.

For example, given a choice between receiving $100 today or $110 in a month, many choose the immediate $100. However, when choosing between $100 in a year or $110 in thirteen months, the same individuals often choose the larger, delayed reward. This “present bias” suggests that the human brain is structurally poorly equipped to weigh immediate utility against distant outcomes. The “now” is processed by the limbic system—the emotional, reactive part of the brain—while the “future” is the domain of the prefrontal cortex—the analytical, calculating part. In moments of stress or high information velocity, the limbic system typically dominates, causing a collapse in the time horizon.

Evolutionary Mismatch and Probabilistic Risk

From an evolutionary perspective, long-term thinking was often a high-risk strategy. In a world of predators, disease, and environmental instability, the “long term” was not guaranteed. Investing energy into a ten-year outcome was irrational if the probability of surviving to year ten was low. Modern financial and professional systems, however, are characterized by relatively high stability and the non-linear rewards of compounding. We are, essentially, using Paleolithic hardware to navigate a geometric environment. This mismatch ensures that short-termism remains the default biological setting.

Read also: Why Long-Term Thinking Is a Financial Advantage

Incentive Structures That Reward Short-Term Outcomes

While biology provides the baseline bias, institutional design reinforces it. In modern markets and organizations, rational actors are frequently incentivized to prioritize short-term metrics at the expense of long-term health. This is primarily a result of the “Principal-Agent” problem.

The Principal-Agent Problem in Time Horizons

In most institutional settings, the person making the decision (the Agent) is not the same person who reaps the long-term rewards or suffers the long-term consequences (the Principal). A CEO on a four-year contract, for instance, is incentivized to maximize the stock price or earnings per share during their tenure to maximize their own compensation and reputation. If a strategic investment takes seven years to yield a return, the current CEO bears 100% of the cost (lower current earnings) while their successor reaps 100% of the benefit.

Quarterly Reporting and the Institutional Imperative

Public equity markets have institutionalized short-termism through the mechanism of quarterly reporting. The pressure to meet analyst expectations creates a “balancing loop” that discourages long-term capital allocation. If an organization misses a quarterly target, its cost of capital may rise, or its leadership may face termination. Consequently, managers frequently delay R&D, maintenance, or brand-building—all of which have long-term payoffs—to “smooth” short-term earnings.

This is further amplified by the “Institutional Imperative,” a term coined by Warren Buffett to describe the tendency of corporate managers to mimic the behavior of their peers. If most competitors are optimizing for the quarter, the manager who optimizes for the decade appears to be an underperformer in the short term, regardless of the eventual terminal value of their strategy.

Media and Information Velocity

The modern information environment operates on a feedback loop of seconds and minutes. Social media and 24-hour financial news cycles create a “recency bias” that treats every minor fluctuation as a structural shift. For a decision-maker, this high-velocity environment creates a constant pressure to react. In this context, “doing nothing”—often the most effective long-term move—is perceived as a failure of agency or a lack of vigilance.

Read also: Mastering The 5 AM Club for Elite Performance and Cognitive Sovereignty

Feedback Loop Distortion and Delayed Consequences

Learning and strategy depend on feedback loops. In a simple system, the relationship between an action and its consequence is immediate and clear. In a complex, long-term system, this relationship is distorted by “delay” and “noise.”

The Noise-to-Signal Ratio

On a short time horizon, the vast majority of data is “noise”—random variance that does not reflect the underlying structural trend. On a long time horizon, the “signal”—the fundamental growth or decay of the system—becomes visible.

The structural difficulty of long-term thinking is that the human brain is highly sensitive to noise. When a decision-maker observes a system frequently (e.g., checking a stock portfolio daily), they are exposed to an overwhelming amount of noise, which triggers emotional reactivity and short-term “course corrections.” These corrections often disrupt the underlying signal, preventing the long-term strategy from maturing.

Delayed Feedback and Reinforcement Learning

Reinforcement learning principles show that behaviors followed by immediate rewards are more likely to be repeated. Short-term strategies (like cutting costs to hit a target) often provide immediate positive reinforcement: a higher stock price, a bonus, or professional praise. Long-term strategies (seeding a new market or developing a rare skill) often involve an initial “trough” of negative feedback: higher costs, increased stress, and lower visible output.

This creates a “feedback loop distortion.” The decision-maker is effectively punished in the short term for making the “correct” long-term decision. Without a robust mental model to withstand this period of negative reinforcement, most actors revert to the short-term path.

Read also: How Anchoring Bias Affects Financial Choices

Compounding as a Structural Advantage

The primary mathematical reason long-term thinking is valuable is the nature of compounding. Compounding—the process by which the output of one period becomes the input of the next—is a geometric progression that is inherently back-loaded.

The Mechanics of Geometric Growth

In any compounding system, whether financial capital, reputation, or skill acquisition, the relationship between time and value is non-linear. In the early stages of the process, the growth is almost imperceptible. This is the “linear phase” where effort appears to outweigh results. However, once the system reaches a critical threshold—the “knee of the curve”—the growth becomes vertical.

The rarity of long-term thinking creates a strategic “moat” because most participants exit the system during the linear phase. When an individual or institution abandons a strategy at year three of a ten-year compounding cycle, they effectively forfeit the 80% of the total value that would have been generated in years eight through ten. Those who can maintain their position through the linear phase capture an asymmetric portion of the total system value.

Multi-Domain Compounding

Compounding is not limited to interest rates. It applies to:

- Skill Acquisition: The more you know about a complex field, the faster you can acquire new, related information. Expertise is a compounding asset.

- Reputation and Trust: Trust is built through consistent behavior over multiple cycles. A long-term reputation reduces transaction costs and attracts higher-quality opportunities.

- Network Effects: The value of a network increases exponentially with each new participant. Maintaining a presence in a specific network over decades creates “Lindy Effect” advantages that cannot be replicated by short-term entrants.

Read also: Why Cash Flow Thinking Beats Net Worth Obsession

Path Dependency and Irreversibility

A critical, often overlooked aspect of time horizons is path dependency—the idea that current decisions limit or expand the set of future options. Short-term thinking often involves “optimizing for the local maximum” at the expense of long-term optionality.

Local vs. Global Optima

In systems dynamics, a “local optimum” is the best solution within a narrow set of parameters. A “global optimum” is the best solution across the entire system over time. Frequently, the path to the global optimum requires moving away from a local optimum. This is cognitively difficult because it requires accepting a temporary decrease in performance.

Short-term optimization (e.g., maximizing this year’s bonus by ignoring a new technological threat) “locks” the actor into a specific path. As they continue to optimize for the short term, they become more fragile. Decisions become path-dependent: once a certain amount of capital or reputation has been committed to a sub-optimal short-term path, the cost of “reverting” to the long-term path becomes prohibitively high.

Second-Order Effects

Long-term thinking is synonymous with second-order thinking. A first-order effect is “What happens if I do this now?” A second-order effect is “What happens as a result of what happened if I do this now?” Short-termism usually stops at the first order. By ignoring second-order consequences (e.g., the long-term brand damage of a short-term marketing hack), the decision-maker creates a “debt” that must eventually be paid with interest.

Read also: The Difference Between Volatility and Risk

Why Long-Term Thinkers Create Disproportionate Value

The value of long-term thinking is an arbitrage of human psychology and institutional failure. Because the environment is structurally biased toward the short term, the “long-term arena” is remarkably uncrowded.

Time Arbitrage

In finance, arbitrage is the simultaneous purchase and sale of an asset to profit from a difference in price. “Time arbitrage” is the strategic practice of exploiting the different time horizons of market participants. If the majority of participants are forced to sell an asset or abandon a project due to a short-term liquidity crisis or a quarterly reporting miss, the long-term thinker—who is not subject to those same pressures—can acquire that asset at a significant discount.

Market Inefficiency and Impatience

Impatience is a form of market inefficiency. When a market is dominated by short-term actors, prices and opportunities are dictated by immediate news and sentiment. The long-term thinker can “arbitrage” this impatience by remaining steady when others are reactive. By playing a different game (e.g., a ten-year game in a one-year market), the long-term thinker is effectively competing against fewer people. The “rarity” of the behavior is what creates the “alpha” (excess return).

Duration as a Competitive Moat

The ability to wait is a structural advantage that cannot be easily copied. A competitor can copy your product, your technology, or your marketing. However, they cannot easily copy your time horizon if they are beholden to quarterly earnings or a two-year political cycle. Therefore, duration itself becomes a competitive moat. An organization with the “permission” (from shareholders or leadership) to think in ten-year blocks can pursue R&D and market-building strategies that are physically impossible for their short-term competitors to execute.

Read also: How Fear and Greed Drive Market Cycles

Common Misconceptions About Long-Term Thinking

To apply long-term thinking with rigor, one must distinguish it from several common oversimplifications.

Equating Patience with Passivity

Long-term thinking is not “wait and see.” It is an active, aggressive pursuit of a long-term goal. It often involves making more difficult decisions in the short term—such as cutting a profitable but declining business unit to invest in an unproven but growing one. Passivity is avoiding decisions; long-term thinking is making decisions based on a different set of terminal values.

The Fallacy that Long-Term Equals Low Risk

A common misunderstanding is that long-term thinking is “safe.” In reality, a ten-year horizon is subject to “Black Swan” events and structural shifts that a one-year horizon may ignore. Long-term thinking does not eliminate risk; it shifts the type of risk one is willing to accept. The long-term thinker accepts “volatility risk” (short-term price movement) in exchange for reducing “terminal risk” (the risk of being structurally obsolete in ten years).

Assuming Patience Guarantees Outcomes

Patience is a multiplier of quality, not a substitute for it. Being “patient” with a bad business model or a useless skill will only result in a larger loss over time. Long-term thinking must be coupled with continuous “stress-testing” of the underlying assumptions. If the fundamental thesis changes, the long-term thinker must be willing to pivot. The difference is that they pivot based on structural changes, not price noise.

Read also: Financial Freedom From $2.26 to $1.25 Million in 5 Years

Broader Framework Connections

Long-term thinking is the thread that connects several diverse fields of decision theory:

- Systems Thinking: Understanding that a system’s behavior over time is more important than its state at any single moment. Long-term thinking is the practice of managing the “stocks” and “flows” of a system for terminal health.

- Incentive Design: The recognition that if you want long-term outcomes, you must align the “reward timing” with the “time horizon.” If an employee is measured on a month-to-month basis, it is irrational to expect them to act for the benefit of the company in year five.

- Opportunity Cost: The realization that time is the ultimate scarce resource. The opportunity cost of a short-term “win” is often the long-term “dominance” that was sacrificed to achieve it.

- Capital Allocation Theory: Treating time as a form of capital. Just as one allocates financial capital to the highest-yielding investments, one should allocate their “time horizon” to the systems with the highest potential for compounding.

Conclusion: Time Horizon as a Strategic Variable

The rarity of long-term thinking is not an accident of culture or a lack of individual character; it is a structural feature of human and institutional systems. We are biologically predisposed to the “now,” and our most powerful institutions—markets and governments—have doubled down on this bias through their incentive and reporting structures.

However, it is precisely this structural rarity that creates the immense value of a long-term horizon. In a world of increasing information velocity and immediate feedback, the capacity to extend one’s time horizon is perhaps the most significant “arbitrage” available to the modern decision-maker.

By understanding that the short-term bias of others is a result of their structural constraints, the long-term thinker can position themselves to benefit from the “noise” and “volatility” that others fear. Rarity increases strategic advantage. In a market of one-year thinkers, the ten-year thinker is a monopoly. Ultimately, long-term thinking is not about predicting the future, but about aligning one’s behavior with the non-linear mechanics of compounding and survival. The most valuable strategic variable is not speed, but duration.