Rent Is Not Cash Flow: The Landlord Math That Fools Almost Everyone

“Rent minus mortgage” is the most seductive wrong number in real estate. Here’s what actually determines your rental property cash flow — and why so many landlords overestimate it.

The first time I looked at a rental property, I did the math every beginner does. Rent is $1,600 a month. Mortgage is $1,200. So I make $400 a month — nice! That simple subtraction is the most common calculation in amateur real estate, and it’s also badly, expensively wrong. Real rental property cash flow is what’s left after everything, and the gap between “rent minus mortgage” and reality is where a lot of landlords quietly lose money while believing they’re profitable. Here’s what that seductive math leaves out.

The costs hiding between rent and profit

Rent minus mortgage ignores an entire category of costs that every rental incurs. Some are obvious once you list them; others are the sneaky ones that get forgotten precisely because they don’t show up every month:

- Property taxes and insurance — often significant, and sometimes bundled into the mortgage payment (or not), which is exactly how they get double-counted or missed.

- Repairs and maintenance — things break. Constantly. A rental generates a steady stream of small repairs plus the occasional large one.

- Property management — whether you pay a manager a percentage of rent, or you do it yourself (in which case you’re paying with your time, which isn’t free).

- Utilities and other operating costs — depending on the property and lease, some of these are yours.

Subtract just these, and that comfortable $400 shrinks considerably. But two more costs — the ones almost nobody budgets for — often do the most damage.

Vacancy: the cost of the rent you don’t collect

Here’s a number beginners essentially never include: vacancy. Your rental will not be occupied 100% of the time, forever. Tenants leave. Units sit empty between tenants while you clean, repair, market, and screen. During those weeks, you collect nothing — but the mortgage, taxes, and insurance keep coming.

Vacancy is a real, recurring cost, and it must be budgeted for. Assuming full occupancy in your math is assuming a fantasy. Experienced investors always haircut their expected rent to account for vacancy, because a single month empty can wipe out several months of “profit” from the rent-minus-mortgage calculation. It’s not a matter of if you have vacancy; it’s how much you planned for it.

CapEx: the big costs that arrive eventually

The other silent killer is capital expenditures — the big, occasional replacements. Roofs. Water heaters. HVAC systems. Flooring. These don’t happen monthly, which is exactly why people forget them. But they will happen, they’re expensive, and they’re a genuine cost of owning the property.

The right way to handle capex is to set aside a portion of rent every month as a reserve, so that when the roof needs replacing, the money is there and it doesn’t blow up your returns. Landlords who don’t reserve for capex aren’t avoiding the cost — they’re just being surprised by it, often in a way that wipes out years of small monthly “profit” in one hit. Ignoring capex doesn’t make it disappear; it just makes it ambush you.

True cash flow: what’s left after everything

Real cash flow is rent, minus all operating expenses (taxes, insurance, maintenance, management, utilities), minus reserves for vacancy and capex, minus the mortgage. What remains is what the property actually puts in your pocket — and it’s usually a lot less than “rent minus mortgage.”

That’s a sobering number, but it’s the only honest one. Plenty of properties that look like they make $400 a month actually make far less, break even, or lose money once everything’s counted. And the difference matters enormously: a landlord who thinks they’re making $400 might buy more properties on that assumption and build a portfolio on sand. Knowing your true cash flow is what separates investors who actually profit from ones who are slowly losing money while feeling successful.

Log the real numbers, not the estimates

The other half of this is tracking actual income and expenses over time, not just estimating them once at purchase. Your real repair costs, real vacancy, real everything — logged as they happen — tell you what the property genuinely earns, versus what you hoped it would. Estimates are for deciding whether to buy; actuals are for knowing what you own. Investors who log their real numbers know exactly which properties perform and which quietly underperform. Those who never look just assume the original estimate held (it rarely did).

An honest note

As always with property: this is my own experience and a way of thinking about rental numbers — not financial, investment, tax, or real-estate advice, and no calculation guarantees a result. Property investments carry real risk, figures are estimates, and costs vary hugely by market and property. Do your own due diligence and consult qualified professionals before making investment decisions.

If you want the math done for you

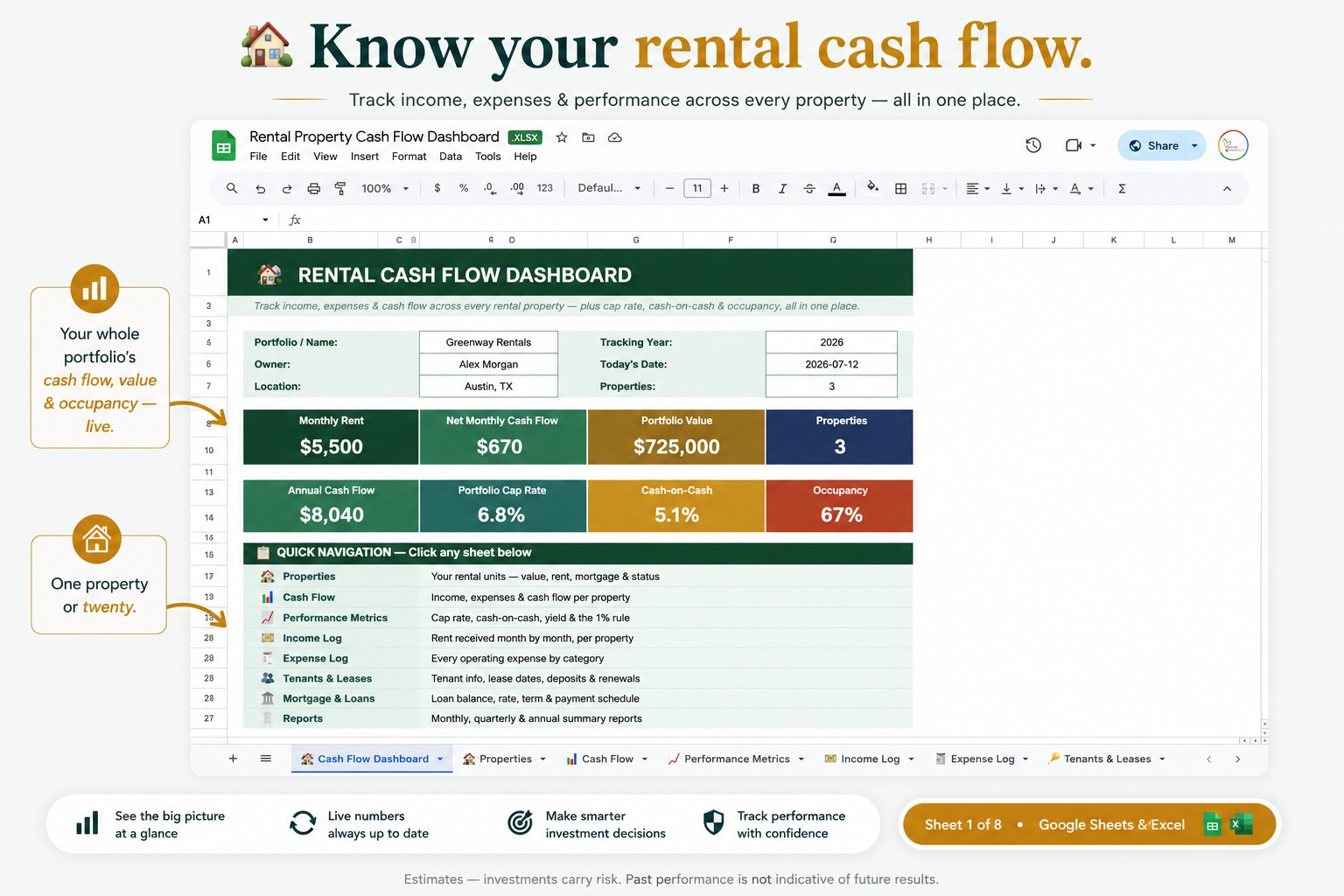

I built a rental cash flow dashboard in Google Sheets that calculates true cash flow for every property — rent, all expenses and the mortgage, with income and expense logs for your real numbers, plus cap rate, cash-on-cash return and occupancy across your whole portfolio:

👉 Rental Property Cash Flow Dashboard for Google Sheets & Excel

Whether you use mine or run the numbers yourself, stop calculating rent minus mortgage and calling it profit. Count every cost — including the vacancy and capex nobody budgets for — and find out what your rentals really earn. The honest number is less exciting than the fantasy, but it’s the only one you can actually build a portfolio on.

This reflects my own experience and is a tracking tool — not financial, investment, tax or real-estate advice; figures are estimates and property investments carry risk. Do your own due diligence and consult a professional. What cost surprised you most as a landlord? Tell me in the comments.