Cap Rate vs Cash-on-Cash: Which Number Actually Matters?

Two metrics every real estate investor quotes, and many confuse. Here’s what cap rate vs cash-on-cash each really tells you — and when to use which.

Spend five minutes in any real estate investing conversation and you’ll hear two numbers thrown around: cap rate and cash-on-cash return. They both sound like “the return on the property,” they’re often quoted interchangeably, and plenty of investors — I was one — nod along without really knowing the difference. But they measure genuinely different things, and confusing them leads to bad comparisons and worse decisions. Understanding cap rate vs cash-on-cash properly is one of the highest-value bits of real estate literacy you can pick up. Here’s the plain-English version.

Cap rate: the property’s return, ignoring your financing

Cap rate (capitalization rate) measures the property’s return based on its net operating income relative to its value:

Cap rate = Net Operating Income ÷ Property Value

Net operating income (NOI) is your rental income minus all operating expenses — but not including the mortgage. That exclusion is the whole point. Cap rate deliberately ignores how you financed the property, which means it measures the property itself, independent of your particular loan.

This makes cap rate excellent for one specific job: comparing properties objectively. Because financing is stripped out, two properties can be compared apples-to-apples on the strength of their income relative to their price, regardless of how each buyer happens to be financing. When you want to ask “is this a good property, at this price, in this market?” — cap rate is your tool.

Cash-on-cash: what YOUR money earns

Cash-on-cash return asks a completely different question:

Cash-on-cash = Annual pre-tax cash flow ÷ Total cash you actually invested

This one does account for your financing. It measures the cash the property puts in your pocket each year (after the mortgage), divided by the actual cash you put in (down payment, closing costs, rehab). In other words: what return is your invested money actually earning?

This is the number that answers “was this a good use of my money?” If you put down a certain amount of cash and the property returns a certain cash flow, cash-on-cash tells you the rate that cash is earning — which you can compare against other things you could have done with that money.

Why the difference matters so much: leverage

Here’s where it gets interesting, and where confusing the two becomes dangerous. Because cash-on-cash accounts for financing, leverage changes it dramatically while leaving cap rate untouched.

Buy a property in cash, and your cash-on-cash return will be relatively close to the cap rate (you’ve invested a lot of cash, and there’s no mortgage eating cash flow). Buy the same property with a mortgage, and you’ve invested far less of your own cash — so even though the mortgage reduces your cash flow, the return on your smaller invested amount can be significantly higher. Same property, same cap rate, very different cash-on-cash.

That’s the power (and the risk) of leverage, and it’s exactly why you need both numbers. Cap rate tells you if the property is good. Cash-on-cash tells you if your deal structure is good. A great property with terrible financing can be a bad investment; a decent property with smart financing can be a good one.

Which one should you use?

Both — for different jobs:

- Comparing properties or markets? Use cap rate. It strips out financing so you’re comparing the assets themselves.

- Deciding whether this deal is a good use of your money? Use cash-on-cash. It tells you what your actual invested cash earns.

- Evaluating a whole portfolio? Look at both, plus your absolute cash flow — because ultimately, cash flow is what pays your bills, no matter how good the ratios look.

The mistake is treating them as interchangeable, or quoting whichever flatters the deal. Sophisticated investors know what each number means, and they use the right one for the question they’re actually asking.

Don’t let ratios distract from cash flow

One grounding note: ratios are tools for comparison, but actual cash flow is what keeps a portfolio alive. A property with an impressive cap rate that produces negative cash flow after your mortgage still drains your bank account every month. Never let a good-looking ratio talk you into a property that doesn’t actually pay. Use cap rate and cash-on-cash to evaluate and compare — and then check that the real, all-costs-included cash flow works.

An honest note

This is educational and my own understanding — not financial, investment, tax, or real-estate advice, and no metric guarantees a result. Property investments carry real risk; figures are estimates, and how these metrics apply depends on your situation and market. Do your own due diligence and consult qualified professionals before investing.

If you want them calculated for you

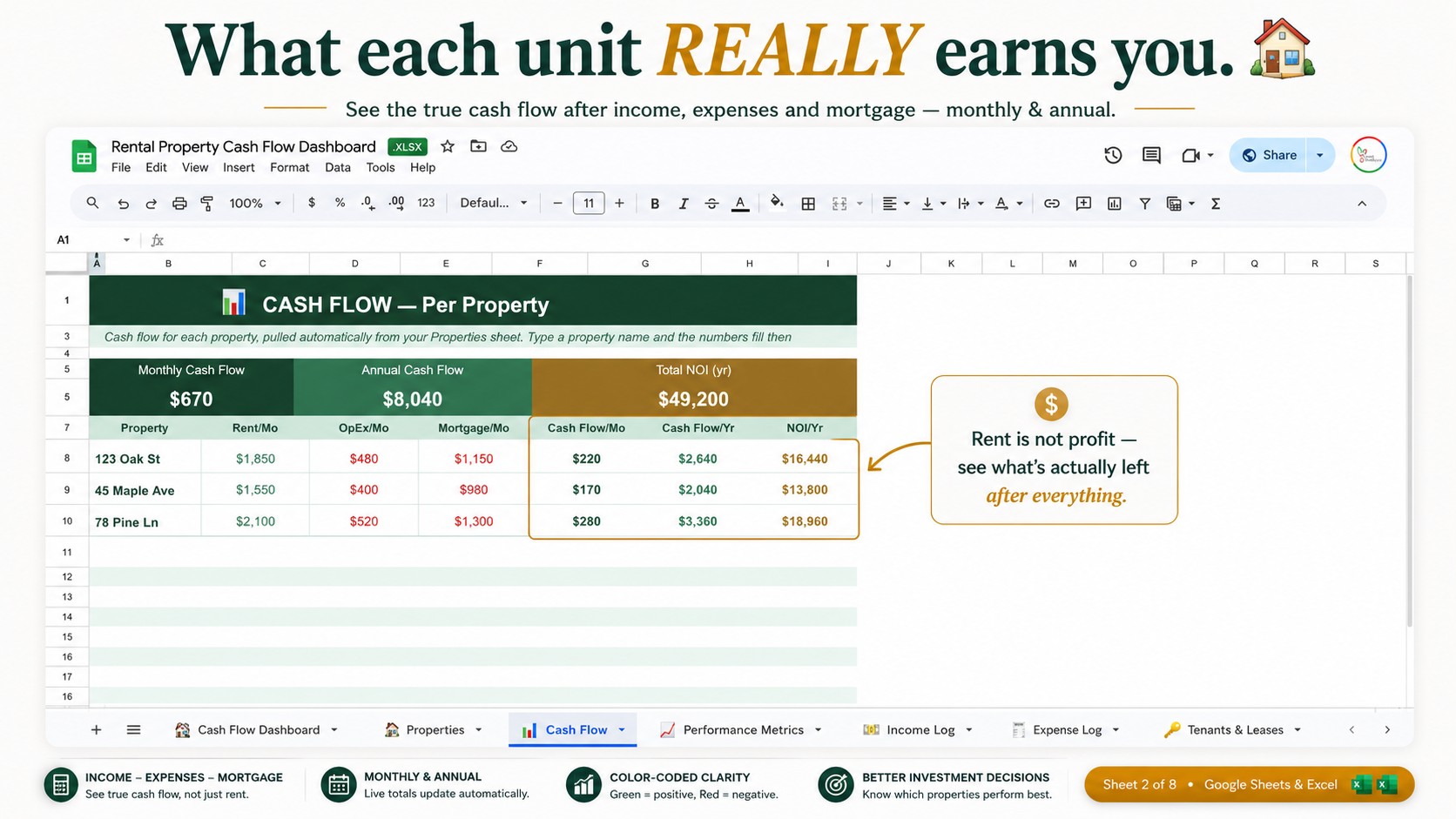

I built cap rate, cash-on-cash return, gross yield and the 1% rule into my rental cash flow dashboard in Google Sheets — enter each property’s value, rent, expenses, mortgage and cash invested, and every metric calculates automatically, with each property rated so you can compare at a glance:

👉 Rental Property Cash Flow Dashboard for Google Sheets & Excel

Whether you use a tool or a calculator, learn the difference between these two numbers. Cap rate judges the property; cash-on-cash judges your deal. Knowing which question you’re asking — and which number answers it — is what turns you from someone who nods along in investing conversations into someone who actually evaluates deals well.

This is educational and my own understanding — not financial, investment, tax or real-estate advice. Figures are estimates; property investments carry risk. Do your own due diligence and consult a professional. Which metric do you lean on most? Tell me in the comments.